Answered step by step

Verified Expert Solution

Question

1 Approved Answer

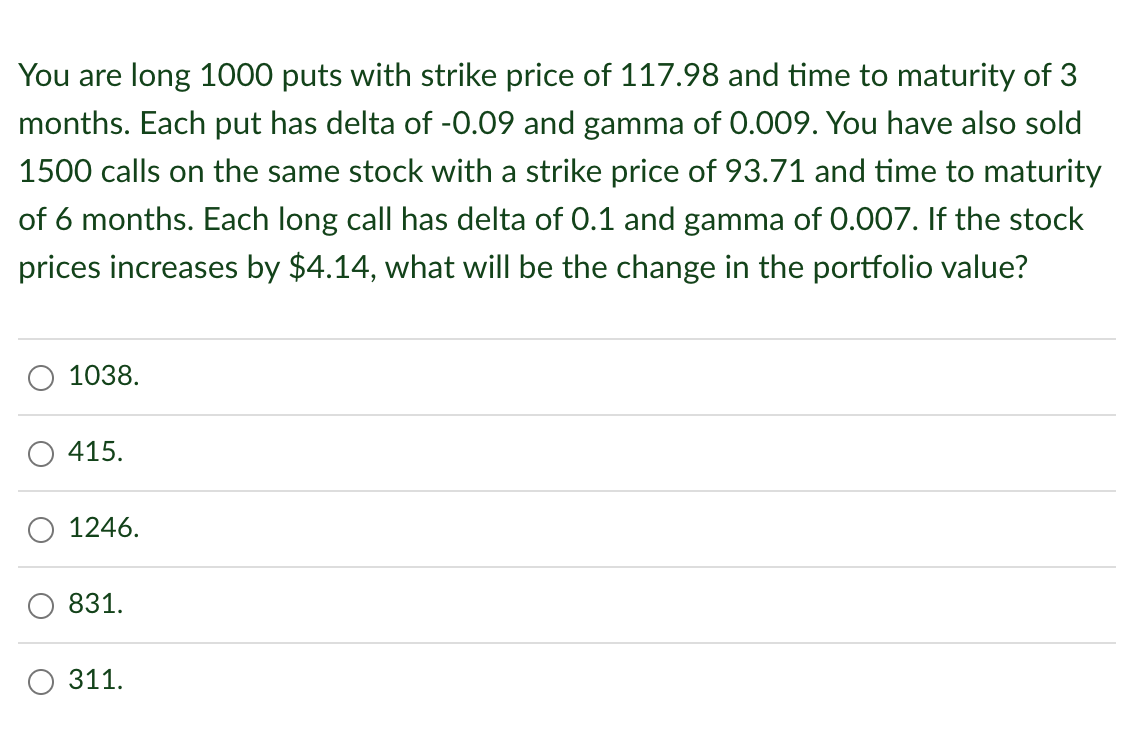

Please answer the following question in Excel. Please provide your cell references You are long 1000 puts with strike price of 117.98 and time to

Please answer the following question in Excel. Please provide your cell references

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Conflict Resolution

Authors: Oliver Ramsbotham, Tom Woodhouse, Hugh Miall

3rd Edition

0745649742,1509509542