please answer the following questions as asked in detail.

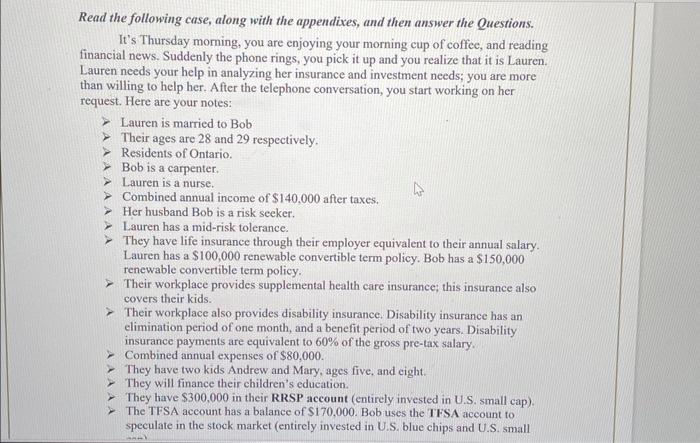

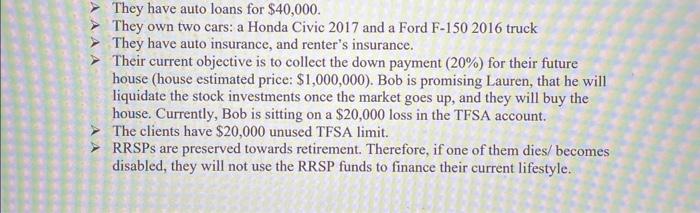

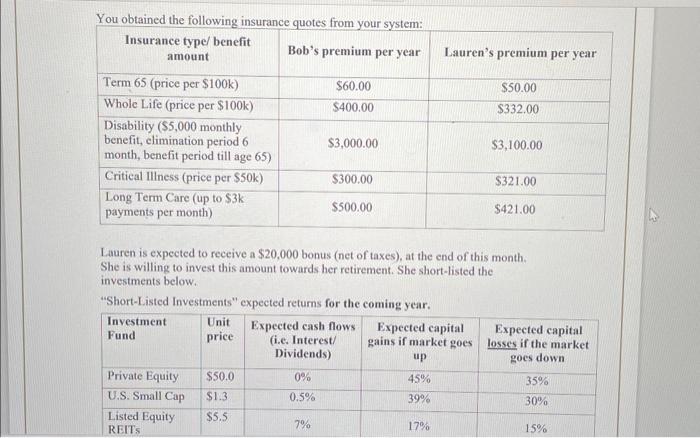

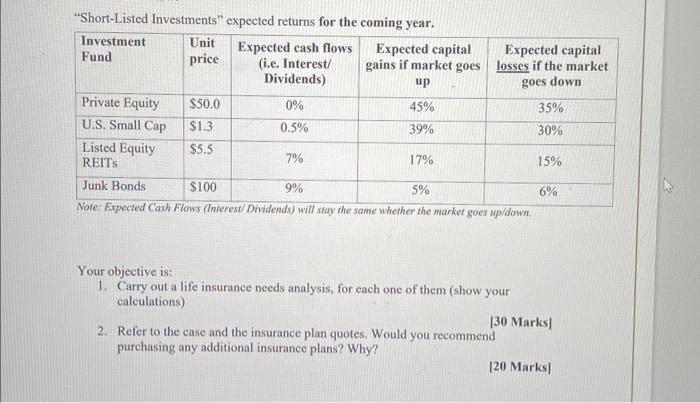

Read the following case, along with the appendixes, and then answer the Questions. It's Thursday morning, you are enjoying your morning cup of coffee, and reading financial news. Suddenly the phone rings, you pick it up and you realize that it is Lauren. Lauren needs your help in analyzing her insurance and investment needs; you are more than willing to help her. After the telephone conversation, you start working on her request. Here are your notes: > Lauren is married to Bob > Their ages are 28 and 29 respectively. > Residents of Ontario. > Bob is a carpenter. > Lauren is a nurse. > Combined annual income of $140,000 after taxes. > Her husband Bob is a risk seeker. > Lauren has a mid-risk tolerance. They have life insurance through their employer equivalent to their annual salary. Lauren has a $100,000 renewable convertible term policy. Bob has a $150,000 renewable convertible term policy. > Their workplace provides supplemental health care insurance; this insurance also covers their kids. > Their workplace also provides disability insurance. Disability insurance has an elimination period of one month, and a benefit period of two years. Disability insurance payments are equivalent to 60% of the gross pre-tax salary. - Combined annual expenses of $80,000. - They have two kids Andrew and Mary, ages five, and eight. They will finance their children's education. They have $300.000 in their RRSP account (entirely invested in U.S. small cap). - The TFSA account has a balance of $170,000. Bob uses the TFSA account to speculate in the stock market (entirely invested in U.S. blue chips and U.S. small They have auto loans for $40,000. They own two cars: a Honda Civic 2017 and a Ford F-150 2016 truck They have auto insurance, and renter's insurance. Their current objective is to collect the down payment (20%) for their future house (house estimated price: $1,000,000 ). Bob is promising Lauren, that he will liquidate the stock investments once the market goes up, and they will buy the house. Currently, Bob is sitting on a $20,000 loss in the TFSA account. The clients have $20,000 unused TFSA limit. RRSPs are preserved towards retirement. Therefore, if one of them dies/ becomes disabled, they will not use the RRSP funds to finance their current lifestyle. Lauren is expected to receive a $20,000 bonus (net of taxes), at the end of this month. She is willing to invest this amount towards her retirement. She short-listed the investments below. "Short-Listed Investments" expected returns for the coming year. "Short-Listed Investments" expected returns for the coming year. vore: axpectea Cash Flows (Interesu Dividends) will stay the same whether the market goes up/down. Your objective is: 1. Carry out a life insurance needs analysis, for each one of them (show your calculations) [30 Marks] 2. Refer to the case and the insurance plan quotes. Would you recommend purchasing any additional insurance plans? Why? [20 Marks] 3. If Bob becomes disabled, how could the family meet the living costs? Are there any governmental plans to support the family in this case? [20 Marks] 4. Refer to the case and appendices and answer the following questions: a. Comment on the client's current asset mix. b. Do you think their portfolio should be redesigned? Why? c. Assuming their portfolio remains unchanged (i.e., they'll keep their investments in small caps and blue chips. Which investment fund/ or asset class will you recommend to Lauren? i.e., where should she invest her $20,000 bonus? (Note: factor in correlations, Sharpe ratios, historical refurns, and volarility) d. Would you use any of Lauren's short-listed funds? Why? e. Assuming an inflation rate of 2% p.a. and a retirement age 65 . Calculate whether they'll have enough money to fully fund their retirement spending of $100,000 in current (real) dollars. Show your work