Please answer the yellow cells for 10.1-10.10 (first photo). The other photos are for reference.

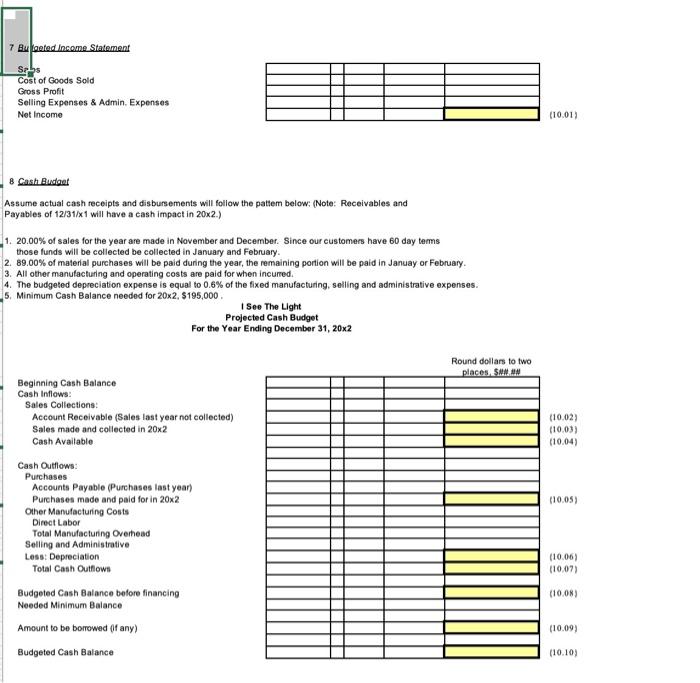

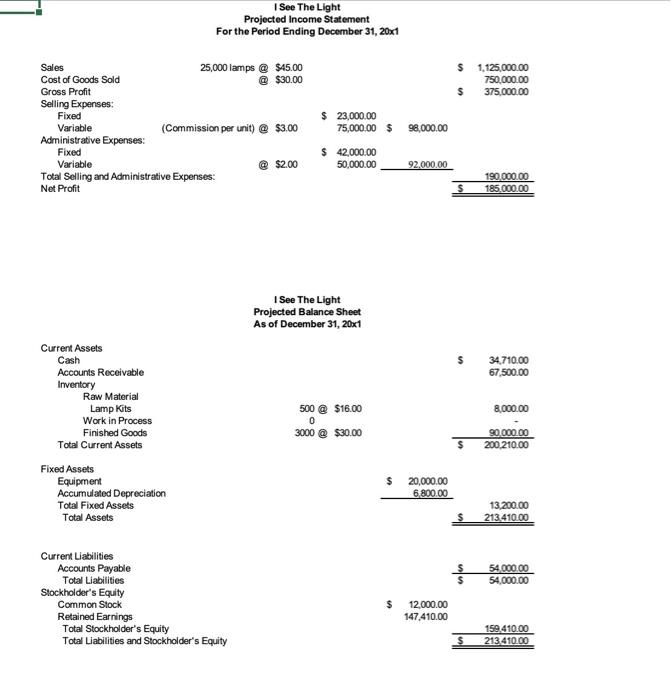

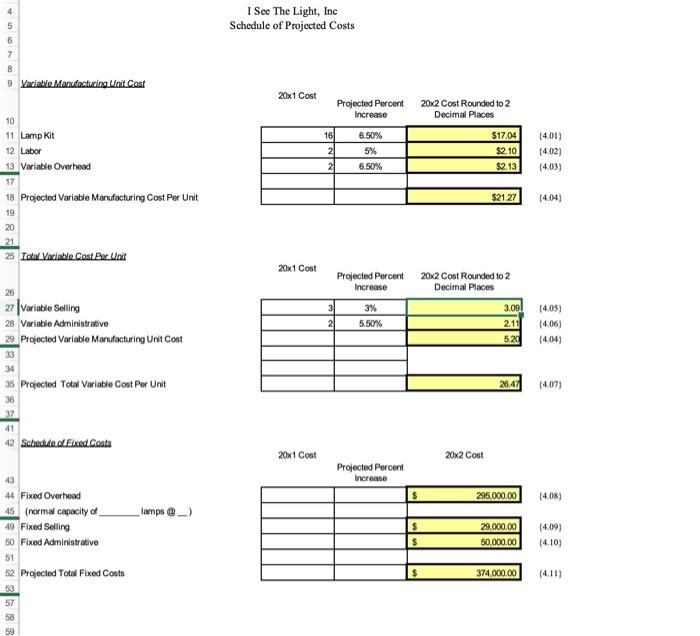

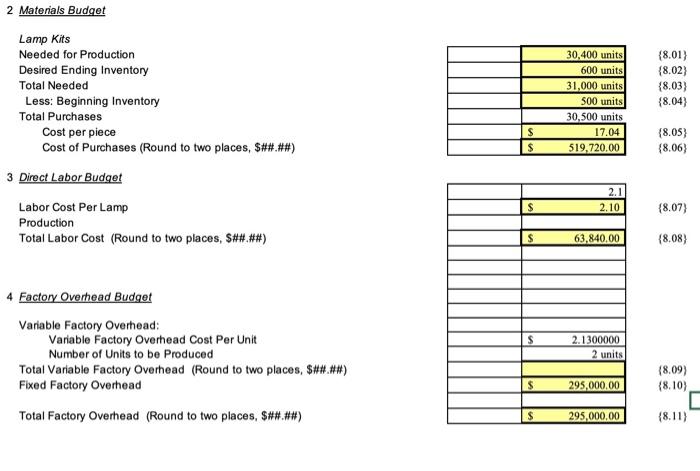

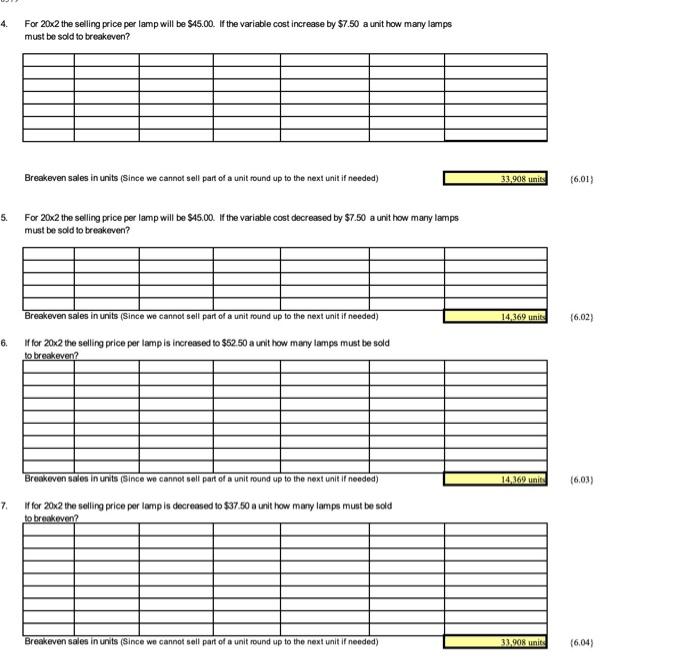

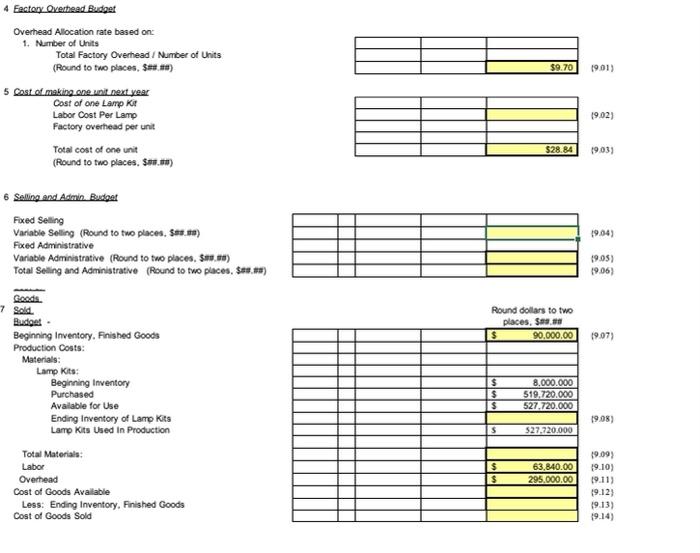

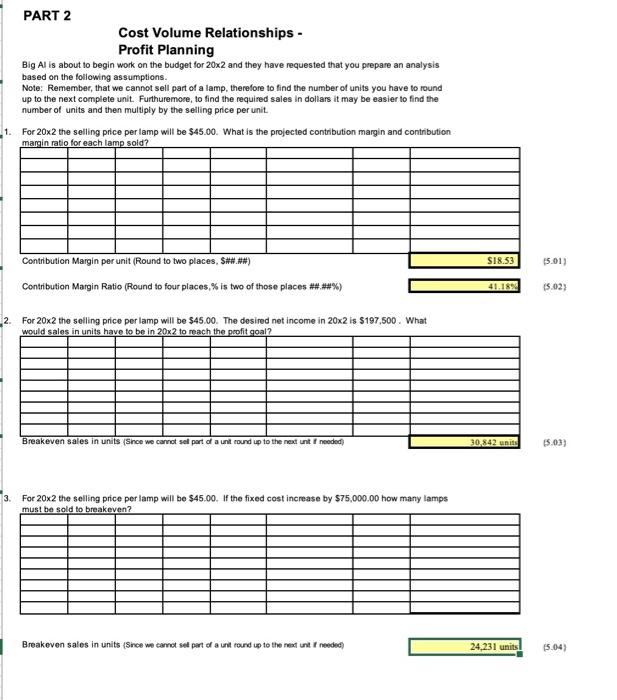

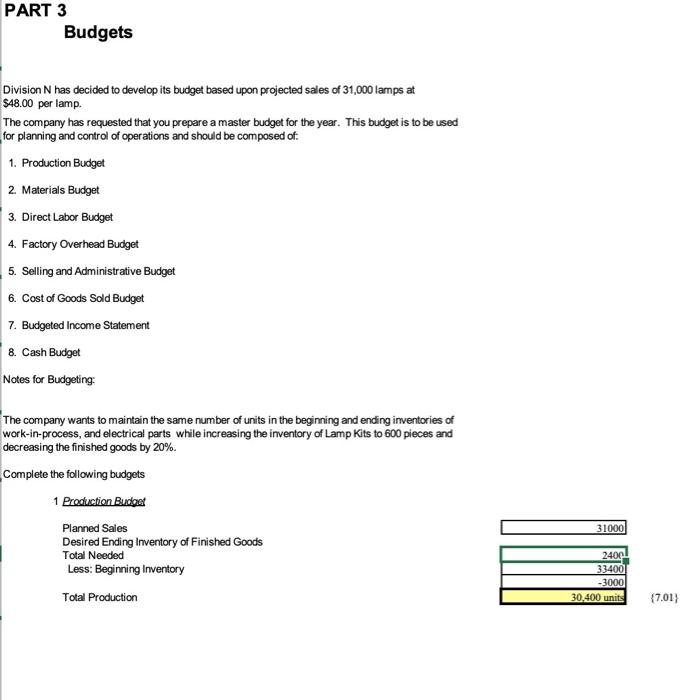

7 Bu Kooted Income Statement Srbs Cost of Goods Sold Gross Profit Selling Expenses & Admin Expenses Net Income (10.01) 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattem below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 20.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February 2. 89.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February 3. All other manufacturing and operating costs are paid for when incurred. 4. The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. 5. Minimum Cash Balance needed for 20x2. $195,000 I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Round dollars to two places SM.M Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) Sales made and collected in 2012 Cash Available (10.02) 110.03) (10.04) 110.05) Cash Outflows: Purchases Accounts Payable (Purchases last year) Purchases made and paid for in 20x2 Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative Loss: Depreciation Total Cash Outflows Budgeted Cash Balance before financing Needed Minimum Balance Amount to be borrowed of any) (10.06) (10.07) (10.08) (10.09 Budgeted Cash Balance (10.10) See The Light Projected Income Statement For the Period Ending December 31, 20x1 Sales 25,000 lamps @ $45.00 Cost of Goods Sold @ $30.00 Gross Profit Selling Expenses: Fixed Variable (Commission per unit) $3.00 Administrative Expenses Fixed Variable @ $2.00 Total Selling and Administrative Expenses: Net Profit $ 1.125,000.00 750,000.00 $375,000.00 $ 23,000.00 75,000.00 $ 98,000.00 $ 42,000.00 50,000.00 92.000.00 190,000.00 $ 185.000.00 I See The Light Projected Balance Sheet As of December 31, 20x1 34.710.00 67,500.00 8,000.00 Current Assets Cash Accounts Receivable Inventory Raw Material Lamp Kits Work in Process Finished Goods Total Current Assets Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets 500 @ $16.00 3000 @ $30.00 0 90.000.00 200.210.00 20,000.00 6,800.00 13.200.00 213.410.00 54.000.00 54,000.00 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity $ 12,000.00 147.410.00 $ 159.410.00 213 410.00 4 I See The Light, Inc Schedule of Projected Costs 5 6 7 9 Variable Manufacturing Unit Cost 20x1 Cost Projected Percent Increase 20x2 Cost Rounded to 2 Decimal Places 16 2 2 6.50% 5% $17.04 $2.10 $2.13 {4.01) 14.02) 14.03) 6.50% 10 11 Lamp Kit 12 Labor 13 Variable Overhead 17 18 Projected Variable Manufacturing Cost Per Unit 19 20 21 25 Total Variable Cost Par Unit $21.27 14.04) 20x 1 Cost Projected Percent Increase 20x2 Cost Rounded to 2 Decimal Places 31 21 3% 5.50% 3.091 211 5.20 14.05) 14.06) (4.04) 27 Variable Selling 23 Variable Administrative 2 Projected Variable Manufacturing Unit Cost 33 34 35 Projected Total Variable Cost Per Unit 20.47 (4.07) 36 41 42 Schedule Eixed Coats 20x1 Cost 20x2 Cost Projected Percent Increase 295,000.00 14.08) 43 44 Fixed Overhead 45 (normal capacity of 49 Fixed Selling 50 Fixed Administrative lamps $ 29,000.00 50,000.00 (4,091 (4.10) 51 374,000.00 (4.11) 52 Projected Total Fixed Costs 53 57 58 59 2 Materials Budget Lamp Kits Needed for Production Desired Ending Inventory Total Needed Less: Beginning Inventory Total Purchases Cost per piece Cost of Purchases (Round to two places, S##.##) 3 Direct Labor Budget Labor Cost Per Lamp Production Total Labor Cost (Round to two places, S##.##) 30.400 units 600 units 31,000 units 500 units 30,500 units 17.04 519,720.00 {8.01) {8.02) {8.03) (8.04) $ $ (8.05) {8.06) 2.1 2.10 $ {8.07) 63,840.00 {8.08) S 4 Factory Overhead Budget Variable Factory Overhead: Variable Factory Overhead Cost Per Unit Number of Units to be produced Total Variable Factory Overhead (Round to two places, $####) Fixed Factory Overhead Total Factory Overhead (Round to two places, S##.##) 2.1300000 2 units $ 295,000.00 (8.09) (8.10) D {8.11) $ 295,000.00 4. For 20x2 the selling price per lamp will be $45.00. If the variable cost increase by $7.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 33,908 units (6.01) 5. For 20x2 the selling price per lamp will be $45,00. If the variable cost decreased by $7.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 14,369 units (6.02) 6. If for 20x2 the selling price per lamp is increased to $52.50 a unit how many lamps must be sold to breakeven Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 14,269 units (6.03) 7 If for 20x2 the selling price per lamp is decreased to $37.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 33.908 unit: (6.04) 4 Factory Overhead Budget $9.70 1901) Overhead Allocation rate based on 1. Number of Units Total Factory Overhead / Number of Units (Round to two places, $.10) 5 Cost of making one unit next year Cost of one Lamp k Labor Cost Per Lamp Factory overhead per unit Total cost of one unit (Round to two places. $1.) 1902) $28.84 1903) 6 Selling and Admin Budget Fixed Seling Variable Selling (Round to two places. Sese) Faced Administrative Variable Administrative (Round to two places. S.) Total Seiling and Administrative (Round to two places, Sr. #) 19.04) 19:05) 1906) Round dollars to two places, S. 90.000.00 19.07) Goods. 7 Sold Budget Beginning Inventory. Finished Goods Production Costs: Materials: Lamp Kits: Beginning Inventory Purchased Available for Use Ending Inventory of Lamp Kits Lamp Kits Used In Production Total Materials: Labor Overhead Cost of Goods Available Less: Ending Inventory. Finished Goods Cost of Goods Sold $ $ $ 8.000.000 519.720.000 527.720.000 19.08) $ $27.220.000 $ $ 63,840.00 295.000.00 19.09) 19.10) 19.11) 19.12) 19.13) PART 2 Cost Volume Relationships - Profit Planning Big Al is about to begin work on the budget for 20x2 and they have requested that you prepare an analysis based on the following assumptions. Note: Remember, that we cannot sell part of a lamp, therefore to find the number of units you have to round up to the next complete unit. Furthuremore, to find the required sales in dollars it may be easier to find the number of units and then multiply by the selling price per unit 1. For 20x2 the selling price per lamp will be $45.00. What is the projected contribution margin and contribution margin ratio for each lamp sold? Contribution Margin per unit (Round to two places, S##.##) S18.53 15.01) Contribution Margin Ratio (Round to four places, % is two of those places ## ##%) 41.18% 15.02) 2. For 20x2 the selling price per lamp will be $45.00. The desired net income in 20x2 is $197.500. What would sales in units have to be in 20x2 to mach the profit goal? Breakeven sales in units (Since we cannot sel part of a unit round up to the next unt needed 30.842 units 15.03) 3 For 20x2 the selling price per lamp will be $45.00. If the fixed cost increase by $75,000.00 how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sel part of a unit round up to the next unt I needed 24,231 units! 15.04) PART 3 Budgets Division N has decided to develop its budget based upon projected sales of 31,000 lamps at $48.00 per lamp. The company has requested that you prepare a master budget for the year. This budget is to be used for planning and control of operations and should be composed of. 1. Production Budget 2. Materials Budget 3. Direct Labor Budget 4. Factory Overhead Budget 5. Selling and Administrative Budget 6. Cost of Goods Sold Budget 7. Budgeted Income Statement 8. Cash Budget Notes for Budgeting The company wants to maintain the same number of units in the beginning and ending inventories of work-in-process, and electrical parts while increasing the inventory of Lamp Kits to 600 pieces and decreasing the finished goods by 20%. Complete the following budgets 1 Production Budget Planned Sales Desired Ending Inventory of Finished Goods Total Needed Less: Beginning Inventory Total Production 31000 2400 334001 -30001 30.400 units {7.01) 7 Bu Kooted Income Statement Srbs Cost of Goods Sold Gross Profit Selling Expenses & Admin Expenses Net Income (10.01) 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattem below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 20.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February 2. 89.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February 3. All other manufacturing and operating costs are paid for when incurred. 4. The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. 5. Minimum Cash Balance needed for 20x2. $195,000 I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Round dollars to two places SM.M Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) Sales made and collected in 2012 Cash Available (10.02) 110.03) (10.04) 110.05) Cash Outflows: Purchases Accounts Payable (Purchases last year) Purchases made and paid for in 20x2 Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative Loss: Depreciation Total Cash Outflows Budgeted Cash Balance before financing Needed Minimum Balance Amount to be borrowed of any) (10.06) (10.07) (10.08) (10.09 Budgeted Cash Balance (10.10) See The Light Projected Income Statement For the Period Ending December 31, 20x1 Sales 25,000 lamps @ $45.00 Cost of Goods Sold @ $30.00 Gross Profit Selling Expenses: Fixed Variable (Commission per unit) $3.00 Administrative Expenses Fixed Variable @ $2.00 Total Selling and Administrative Expenses: Net Profit $ 1.125,000.00 750,000.00 $375,000.00 $ 23,000.00 75,000.00 $ 98,000.00 $ 42,000.00 50,000.00 92.000.00 190,000.00 $ 185.000.00 I See The Light Projected Balance Sheet As of December 31, 20x1 34.710.00 67,500.00 8,000.00 Current Assets Cash Accounts Receivable Inventory Raw Material Lamp Kits Work in Process Finished Goods Total Current Assets Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets 500 @ $16.00 3000 @ $30.00 0 90.000.00 200.210.00 20,000.00 6,800.00 13.200.00 213.410.00 54.000.00 54,000.00 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity $ 12,000.00 147.410.00 $ 159.410.00 213 410.00 4 I See The Light, Inc Schedule of Projected Costs 5 6 7 9 Variable Manufacturing Unit Cost 20x1 Cost Projected Percent Increase 20x2 Cost Rounded to 2 Decimal Places 16 2 2 6.50% 5% $17.04 $2.10 $2.13 {4.01) 14.02) 14.03) 6.50% 10 11 Lamp Kit 12 Labor 13 Variable Overhead 17 18 Projected Variable Manufacturing Cost Per Unit 19 20 21 25 Total Variable Cost Par Unit $21.27 14.04) 20x 1 Cost Projected Percent Increase 20x2 Cost Rounded to 2 Decimal Places 31 21 3% 5.50% 3.091 211 5.20 14.05) 14.06) (4.04) 27 Variable Selling 23 Variable Administrative 2 Projected Variable Manufacturing Unit Cost 33 34 35 Projected Total Variable Cost Per Unit 20.47 (4.07) 36 41 42 Schedule Eixed Coats 20x1 Cost 20x2 Cost Projected Percent Increase 295,000.00 14.08) 43 44 Fixed Overhead 45 (normal capacity of 49 Fixed Selling 50 Fixed Administrative lamps $ 29,000.00 50,000.00 (4,091 (4.10) 51 374,000.00 (4.11) 52 Projected Total Fixed Costs 53 57 58 59 2 Materials Budget Lamp Kits Needed for Production Desired Ending Inventory Total Needed Less: Beginning Inventory Total Purchases Cost per piece Cost of Purchases (Round to two places, S##.##) 3 Direct Labor Budget Labor Cost Per Lamp Production Total Labor Cost (Round to two places, S##.##) 30.400 units 600 units 31,000 units 500 units 30,500 units 17.04 519,720.00 {8.01) {8.02) {8.03) (8.04) $ $ (8.05) {8.06) 2.1 2.10 $ {8.07) 63,840.00 {8.08) S 4 Factory Overhead Budget Variable Factory Overhead: Variable Factory Overhead Cost Per Unit Number of Units to be produced Total Variable Factory Overhead (Round to two places, $####) Fixed Factory Overhead Total Factory Overhead (Round to two places, S##.##) 2.1300000 2 units $ 295,000.00 (8.09) (8.10) D {8.11) $ 295,000.00 4. For 20x2 the selling price per lamp will be $45.00. If the variable cost increase by $7.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 33,908 units (6.01) 5. For 20x2 the selling price per lamp will be $45,00. If the variable cost decreased by $7.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 14,369 units (6.02) 6. If for 20x2 the selling price per lamp is increased to $52.50 a unit how many lamps must be sold to breakeven Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 14,269 units (6.03) 7 If for 20x2 the selling price per lamp is decreased to $37.50 a unit how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 33.908 unit: (6.04) 4 Factory Overhead Budget $9.70 1901) Overhead Allocation rate based on 1. Number of Units Total Factory Overhead / Number of Units (Round to two places, $.10) 5 Cost of making one unit next year Cost of one Lamp k Labor Cost Per Lamp Factory overhead per unit Total cost of one unit (Round to two places. $1.) 1902) $28.84 1903) 6 Selling and Admin Budget Fixed Seling Variable Selling (Round to two places. Sese) Faced Administrative Variable Administrative (Round to two places. S.) Total Seiling and Administrative (Round to two places, Sr. #) 19.04) 19:05) 1906) Round dollars to two places, S. 90.000.00 19.07) Goods. 7 Sold Budget Beginning Inventory. Finished Goods Production Costs: Materials: Lamp Kits: Beginning Inventory Purchased Available for Use Ending Inventory of Lamp Kits Lamp Kits Used In Production Total Materials: Labor Overhead Cost of Goods Available Less: Ending Inventory. Finished Goods Cost of Goods Sold $ $ $ 8.000.000 519.720.000 527.720.000 19.08) $ $27.220.000 $ $ 63,840.00 295.000.00 19.09) 19.10) 19.11) 19.12) 19.13) PART 2 Cost Volume Relationships - Profit Planning Big Al is about to begin work on the budget for 20x2 and they have requested that you prepare an analysis based on the following assumptions. Note: Remember, that we cannot sell part of a lamp, therefore to find the number of units you have to round up to the next complete unit. Furthuremore, to find the required sales in dollars it may be easier to find the number of units and then multiply by the selling price per unit 1. For 20x2 the selling price per lamp will be $45.00. What is the projected contribution margin and contribution margin ratio for each lamp sold? Contribution Margin per unit (Round to two places, S##.##) S18.53 15.01) Contribution Margin Ratio (Round to four places, % is two of those places ## ##%) 41.18% 15.02) 2. For 20x2 the selling price per lamp will be $45.00. The desired net income in 20x2 is $197.500. What would sales in units have to be in 20x2 to mach the profit goal? Breakeven sales in units (Since we cannot sel part of a unit round up to the next unt needed 30.842 units 15.03) 3 For 20x2 the selling price per lamp will be $45.00. If the fixed cost increase by $75,000.00 how many lamps must be sold to breakeven? Breakeven sales in units (Since we cannot sel part of a unit round up to the next unt I needed 24,231 units! 15.04) PART 3 Budgets Division N has decided to develop its budget based upon projected sales of 31,000 lamps at $48.00 per lamp. The company has requested that you prepare a master budget for the year. This budget is to be used for planning and control of operations and should be composed of. 1. Production Budget 2. Materials Budget 3. Direct Labor Budget 4. Factory Overhead Budget 5. Selling and Administrative Budget 6. Cost of Goods Sold Budget 7. Budgeted Income Statement 8. Cash Budget Notes for Budgeting The company wants to maintain the same number of units in the beginning and ending inventories of work-in-process, and electrical parts while increasing the inventory of Lamp Kits to 600 pieces and decreasing the finished goods by 20%. Complete the following budgets 1 Production Budget Planned Sales Desired Ending Inventory of Finished Goods Total Needed Less: Beginning Inventory Total Production 31000 2400 334001 -30001 30.400 units {7.01)