Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please answer these 3 short questions FINA2040 Tutorial 6 - Microsoft Word ings Review View Title 1 Normal A4 EEEEEE IT . - A 1

please answer these 3 short questions

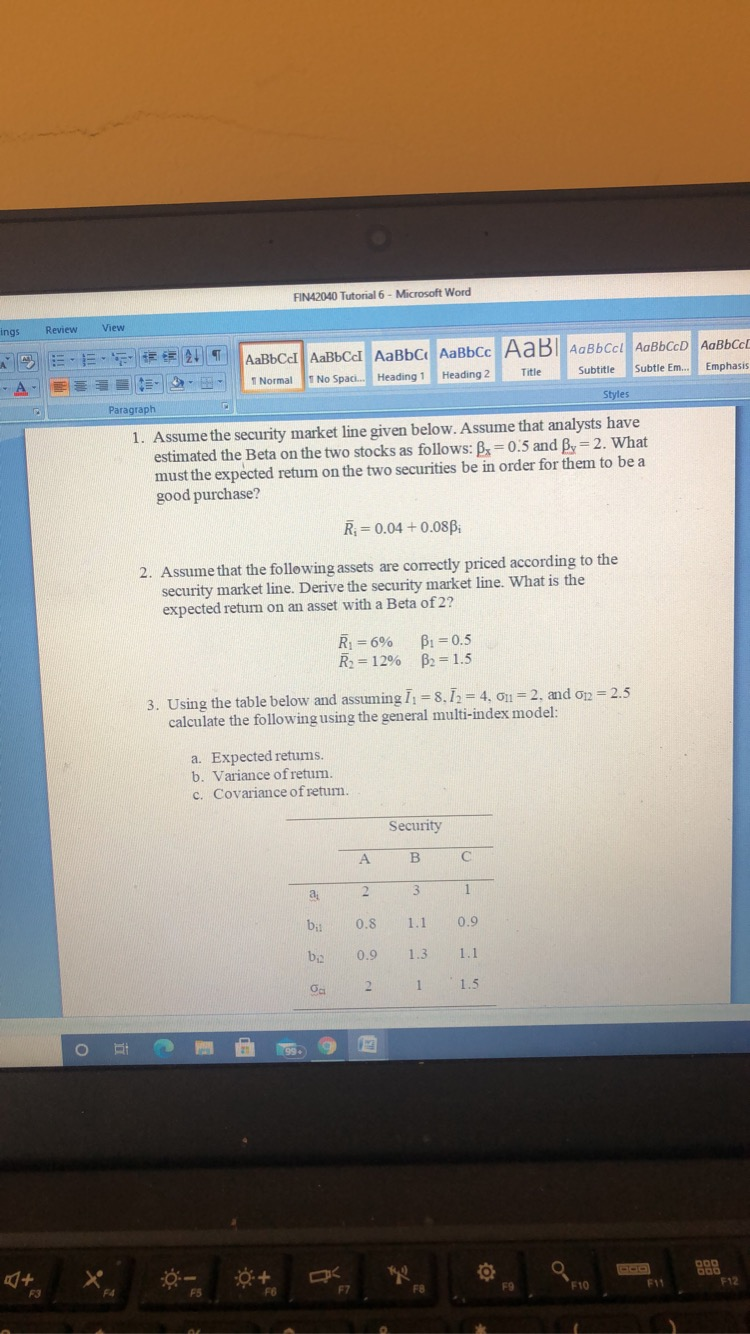

FINA2040 Tutorial 6 - Microsoft Word ings Review View Title 1 Normal A4 EEEEEE IT . - A 1 No Spac... Heading 1 Heading 2 Subtitle Subtle Em.. Emphasis Paragraph Styles 1. Assume the security market line given below. Assume that analysts have estimated the Beta on the two stocks as follows: Bs=0.5 and Bx = 2. What must the expected retum on the two securities be in order for them to be a good purchase? R;= 0.04 +0.08B 2. Assume that the following assets are correctly priced according to the security market line. Derive the security market line. What is the expected return on an asset with a Beta of 2? Ri=6% Bi = 0.5 R2 = 12% B2 = 1.5 3. Using the table below and assuming 11 = 8.12 = 4. on=2. and 012 = 2.5 calculate the following using the general multi-index model: a. Expected retums. b. Variance of retum. c. Covariance of return. Security B a, 2 3 1 bi: 0.8 1.1 0.9 be 0.9 1.3 1.1 OG 2 1 1.5 0 Q F10 000 Boo F12 F1 F3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Healthcare Finance An Introduction To Accounting And Financial Management

Authors: Louis C. Gapenski

5th Edition

1567934250, 978-1567934250