Please answer this!

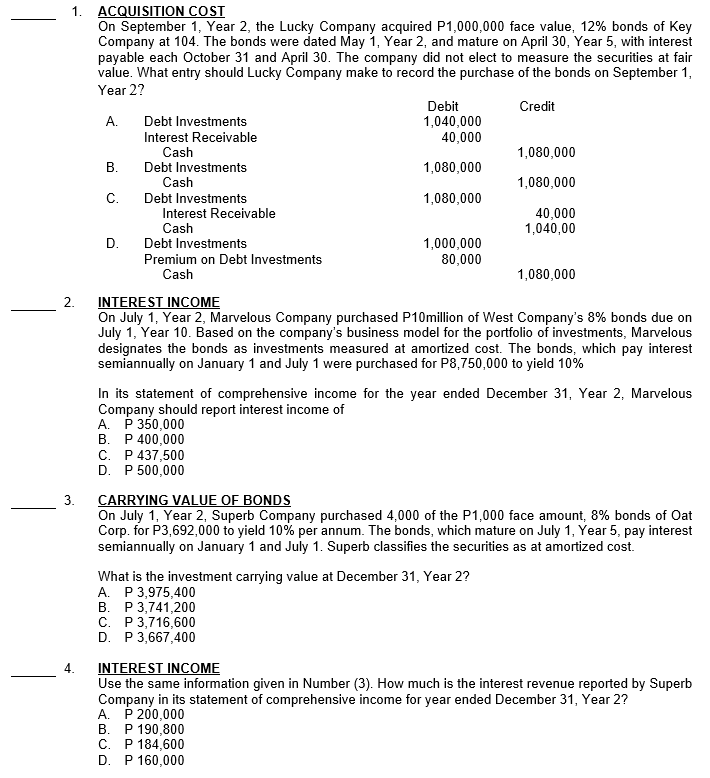

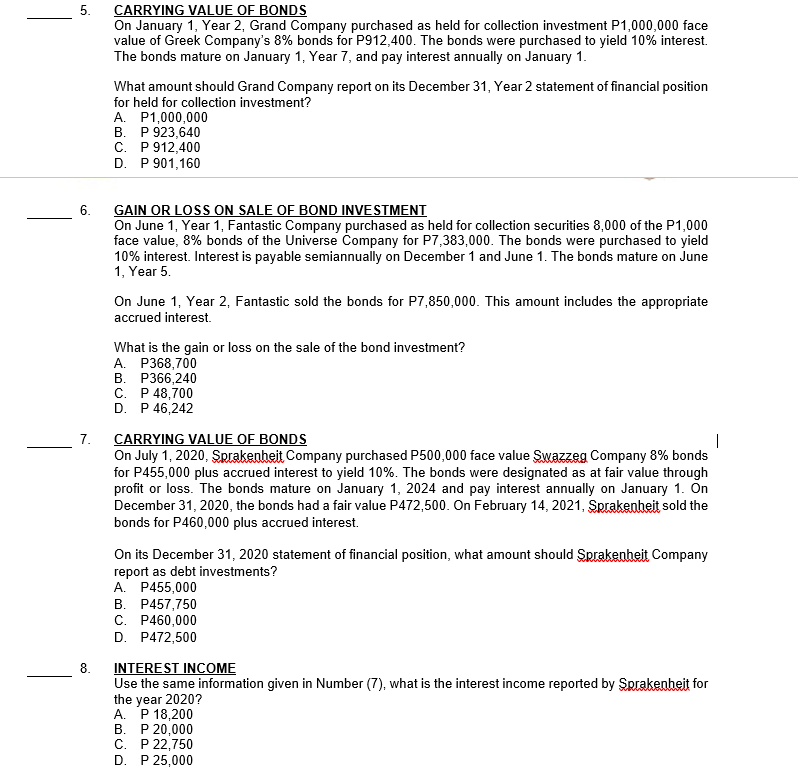

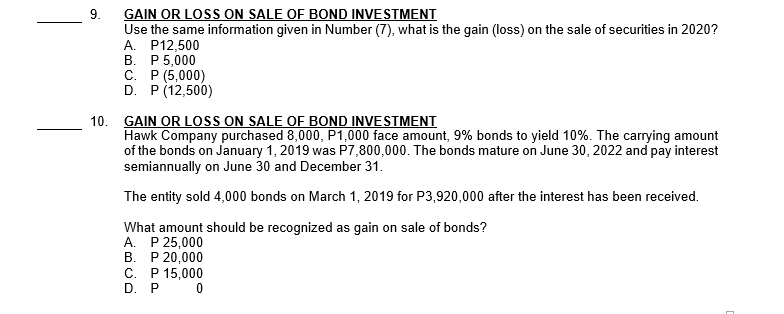

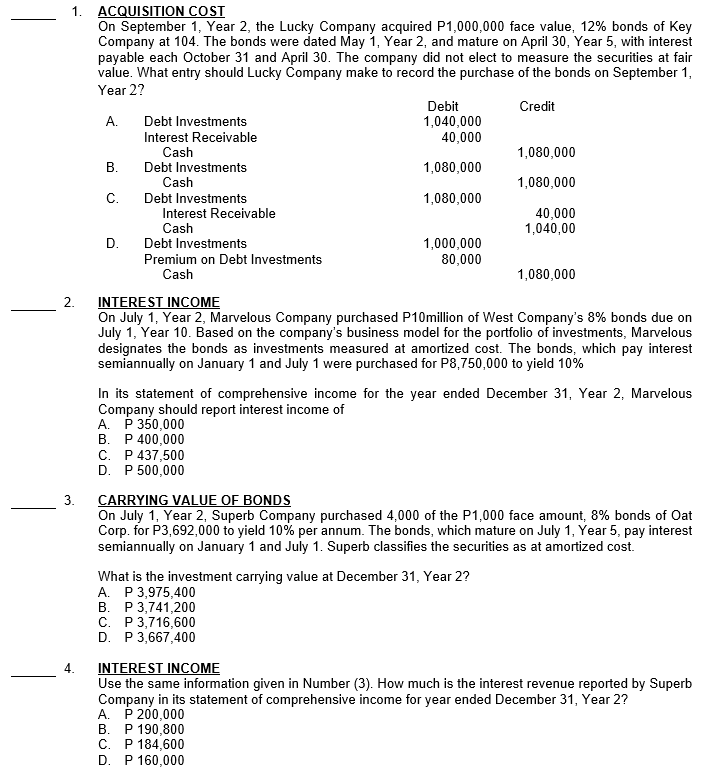

1 . 2. AC UISITION COST On September 1, Year 2, the Lucky Company acquired P1,000,000 face value, 1205 bonds of Key Company at 104. The bonds were dated May 1, Year 2, and mature on April 30, Year 5, with interest payable each October 31 and April 30. The company rid not elect to measure the securities at fair value. What entry should Lucky Company make to record the purchase of the bonds on September 1, Year 2? Debit Credt A. Debt Investments 1,040,000 Interest Receivable 40,000 Cash 1,050 ,0 00 I3. Debt Investments 1,030,121 00 Cash 1,050 ,0 00 C. Debt Investments 1,050,0 00 Interest Receivable 40,0 00 Cash 1,040,00 D. Debt Investments 1,000,000 Premium on Debt Investments 50,000 Cash 1,050 ,0 00 INTEREST INCOME On July 1, Year 2, Marvelous Company purchased P10million of West Company's 335 bends due on July 1, Year 10. Based on the companfs business model for the portfolio of investments, Marvelous designates the bonds as investments measured at amortized cost. The bonds, whidl pay interest semiannually on January 1 and July 1 were purchased for P5,?50,000 to yield 10% In its statement of comprehensive income for the year ended December 31, Year 2, Marvelous Company should report interest income of A. P 350,000 I3. P 400,000 C. P 43?,500 D. P 500,000 CARRYING 1I.I'II!I.LIJE OF BONDS On July 1, Year 2, Superb Company purchased 4,000 of the P1,000 face amount, 5% bonds of Oat Corp. for P1551000 to yield 10% per annum. The bonds, which mature on July 1, Year 5, pay interest semiannually on January 1 and July 1. Superb classies the securities as at amortized cost. What is the investment carrying value at December 31, Year 2? A. P 3,5?5,400 I3. P 3,?41,200 C. P 3,?15,500 D. P 3,55T,400 INTEREST INCOME Use the same information given in Number {3}. How much is the interest revenue reported by Superb Company in its statement of comprehensive income for year ended December 31, Year 2? A. P 200,000 B. P 150,500 C. P 154,500 D. P 150,000 5. CARRYING VALUE OF BONDS On January 1, Year 2, Grand Company purchased as held for collection investment P1,000,000 face value of Greek Company's 8% bonds for P912,400. The bonds were purchased to yield 10% interest. The bonds mature on January 1, Year 7, and pay interest annually on January 1. What amount should Grand Company report on its December 31, Year 2 statement of financial position for held for collection investment? A. 00.00 B. P 923,640 C. P 912,400 P 901,160 6. GAIN OR LOSS ON SALE OF BOND INVESTMENT On June 1, Year 1, Fantastic Company purchased as held for collection securities 8,000 of the P1,000 face value, 8% bonds of the Universe Company for P7,383,000. The bonds were purchased to yield 10% interest. Interest is payable semiannually on December 1 and June 1. The bonds mature on June 1, Year 5. On June 1, Year 2, Fantastic sold the bonds for P7,850,000. This amount includes the appropriate accrued interest. What is the gain or loss on the sale of the bond investment? A. P368,700 P366,240 P 48,700 P 46,242 7. CARRYING VALUE OF BONDS On July 1, 2020, Sprakenheit Company purchased P500,000 face value Swazzeg Company 8% bonds for P455,000 plus accrued interest to yield 10%. The bonds were designated as at fair value through profit or loss. The bonds mature on January 1, 2024 and pay interest annually on January 1. On December 31, 2020, the bonds had a fair value P472,500. On February 14, 2021, Sprakenheit sold the bonds for P460,000 plus accrued interest. On its December 31, 2020 statement of financial position, what amount should Sprakenheit Company report as debt investments? A. P455,000 B. P457,750 C. P460,000 D. P472,500 8 INTEREST INCOME Use the same information given in Number (7), what is the interest income reported by Sprakenheit for the year 2020? A. P 18,200 P 20,000 P 22,750 D. P 25,0009. GAIN OR LOSS ON SALE OF BOND INVESTMENT Use the same information given in Number (7), what is the gain (loss) on the sale of securities in 2020? A. P12,500 B. P 5,000 C. P (5,000) D. P (12,500) 10. GAIN OR LOSS ON SALE OF BOND INVESTMENT Hawk Company purchased 8,000, P1,000 face amount, 9% bonds to yield 10%. The carrying amount of the bonds on January 1, 2019 was P7,800,000. The bonds mature on June 30, 2022 and pay interest semiannually on June 30 and December 31. The entity sold 4,000 bonds on March 1, 2019 for P3,920,000 after the interest has been received. What amount should be recognized as gain on sale of bonds? A. P 25,000 B. P 20,000 C. P 15,000 D. P