Answered step by step

Verified Expert Solution

Question

1 Approved Answer

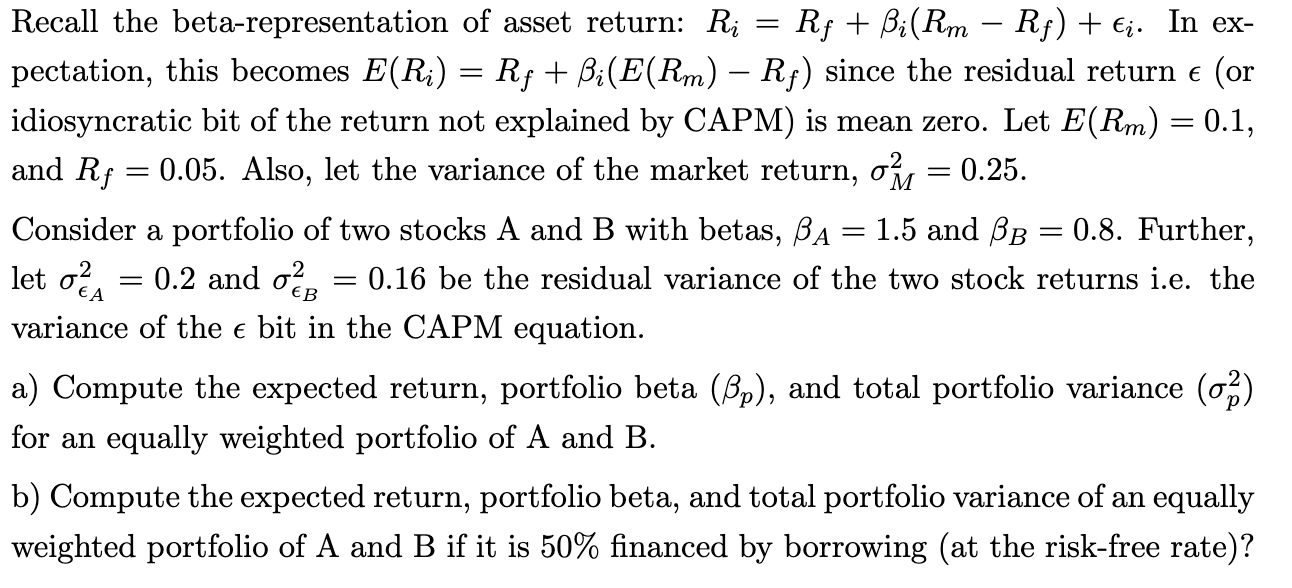

Please answer this question. Recall the beta-representation of asset return: R,- = Rf + 3,-(Rm Rf) + 6,. In ex- pectation, this becomes E(R,-) =

Please answer this question.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exploring Economics

Authors: Robert L Sexton

5th Edition

978-1439040249, 1439040249