Answered step by step

Verified Expert Solution

Question

1 Approved Answer

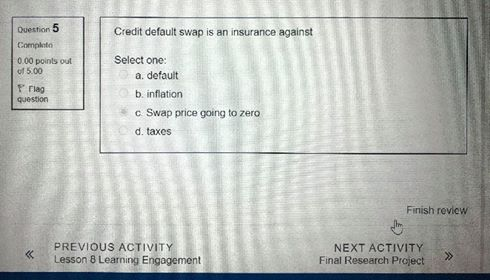

please answer two questions 1) 2) Duestion 5 Credit default swap is an insurance against Complete 0.00 points out of 5.00 Fring question Select one:

please answer two questions

1)

2)

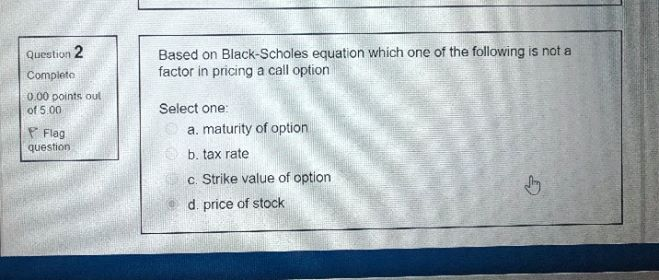

Duestion 5 Credit default swap is an insurance against Complete 0.00 points out of 5.00 Fring question Select one: a default b. inflation c Swap price going to zero d. taxes Finish review PREVIOUS ACTIVITY Lesson 8 Learning Engagement NEXT ACTIVITY Final Research Project >> Question 2 Completo 0.00 points out of 5.00 Based on Black-Scholes equation which one of the following is not a factor in pricing a call option Flag question Select one: a. maturity of option b. tax rate c. Strike value of option d. price of stock

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding The Finance Of Welfare

Authors: Howard Glennerster

2nd Edition

1847421091, 978-1847421098