Please answer two questions, seperately.

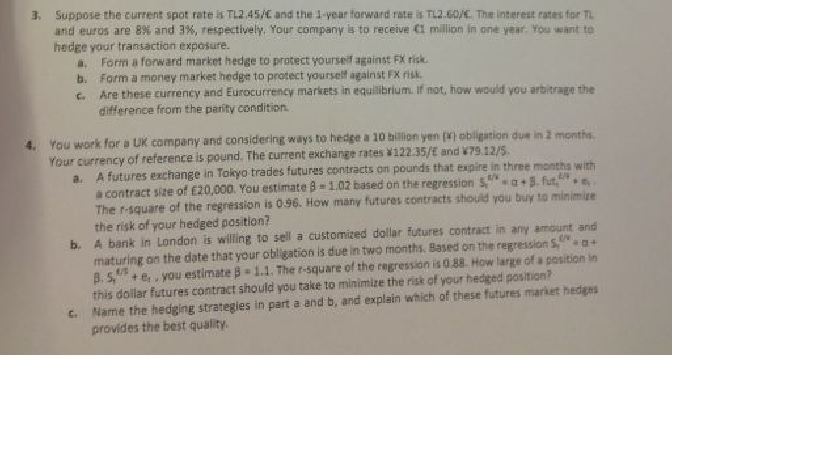

3. Suppose the current spot rate is 192.45/C and the 1-year forward rate : 2.60/. The interest rates for TL and euros are 88 and 3%, respectively, Your company is to receive 1 milion in one year. You want to hedee your transaction exposure. Forma forward market hedge to protect yourself against FX risk. b. Forma money market hedge to protect yourself against FX risk Are these currency and Eurocurrency markets in equilibrium. If not, how would you arbitrage the difference from the party condition. You work for Uk company and considering ways to hega a 10 billion yen obligation due in 3 months Your currency of reference is pound. The current exchange rates 122.35/{ and 79.12/5 a. A futures exchange in Tokyo trades futuras contracts on pounds that expire in three months with a contract size of 20,000. You estimate B - 1.02 based on the regression 5.3. fut. The r-square of the regression is 0.96. How many futures contracts should you buy to the risk of your hedged position b. A bank in London is willing to sell a customized dollar futures contract in any amount and maturing on the date that your obligation is due in two months. Based on the regressions, B. 5."+e.. you estimate B - 1.1. The t-square of the regression is 0.8 How large of a pation in this dollar futures contract should you take to minimize the risk of your hediged position c. Name the hedging strategies in part a and b, and explain which of these futures market hedens provides the best quality 3. Suppose the current spot rate is 192.45/C and the 1-year forward rate : 2.60/. The interest rates for TL and euros are 88 and 3%, respectively, Your company is to receive 1 milion in one year. You want to hedee your transaction exposure. Forma forward market hedge to protect yourself against FX risk. b. Forma money market hedge to protect yourself against FX risk Are these currency and Eurocurrency markets in equilibrium. If not, how would you arbitrage the difference from the party condition. You work for Uk company and considering ways to hega a 10 billion yen obligation due in 3 months Your currency of reference is pound. The current exchange rates 122.35/{ and 79.12/5 a. A futures exchange in Tokyo trades futuras contracts on pounds that expire in three months with a contract size of 20,000. You estimate B - 1.02 based on the regression 5.3. fut. The r-square of the regression is 0.96. How many futures contracts should you buy to the risk of your hedged position b. A bank in London is willing to sell a customized dollar futures contract in any amount and maturing on the date that your obligation is due in two months. Based on the regressions, B. 5."+e.. you estimate B - 1.1. The t-square of the regression is 0.8 How large of a pation in this dollar futures contract should you take to minimize the risk of your hediged position c. Name the hedging strategies in part a and b, and explain which of these futures market hedens provides the best quality