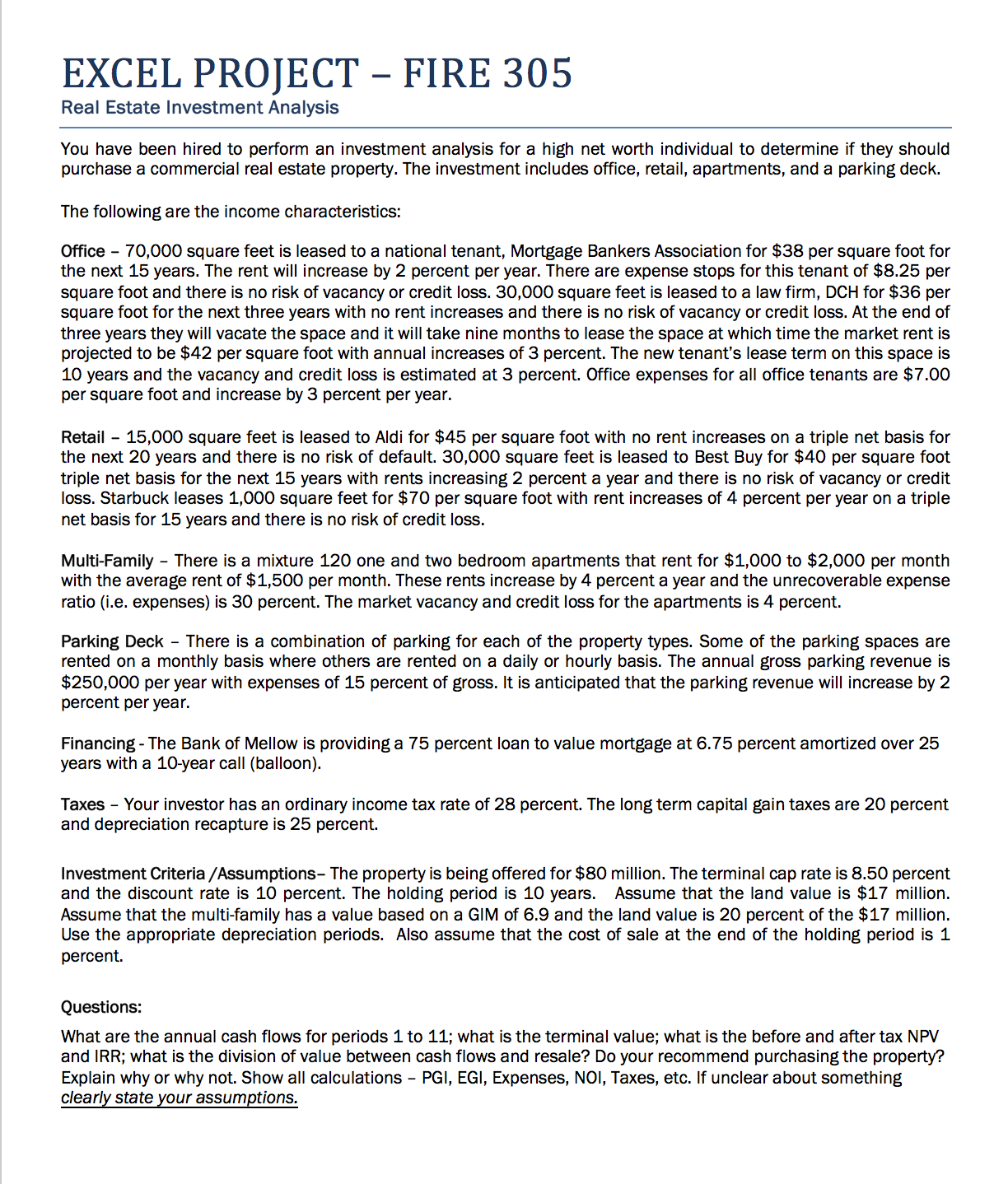

Please answer using Excel in the exact format given below

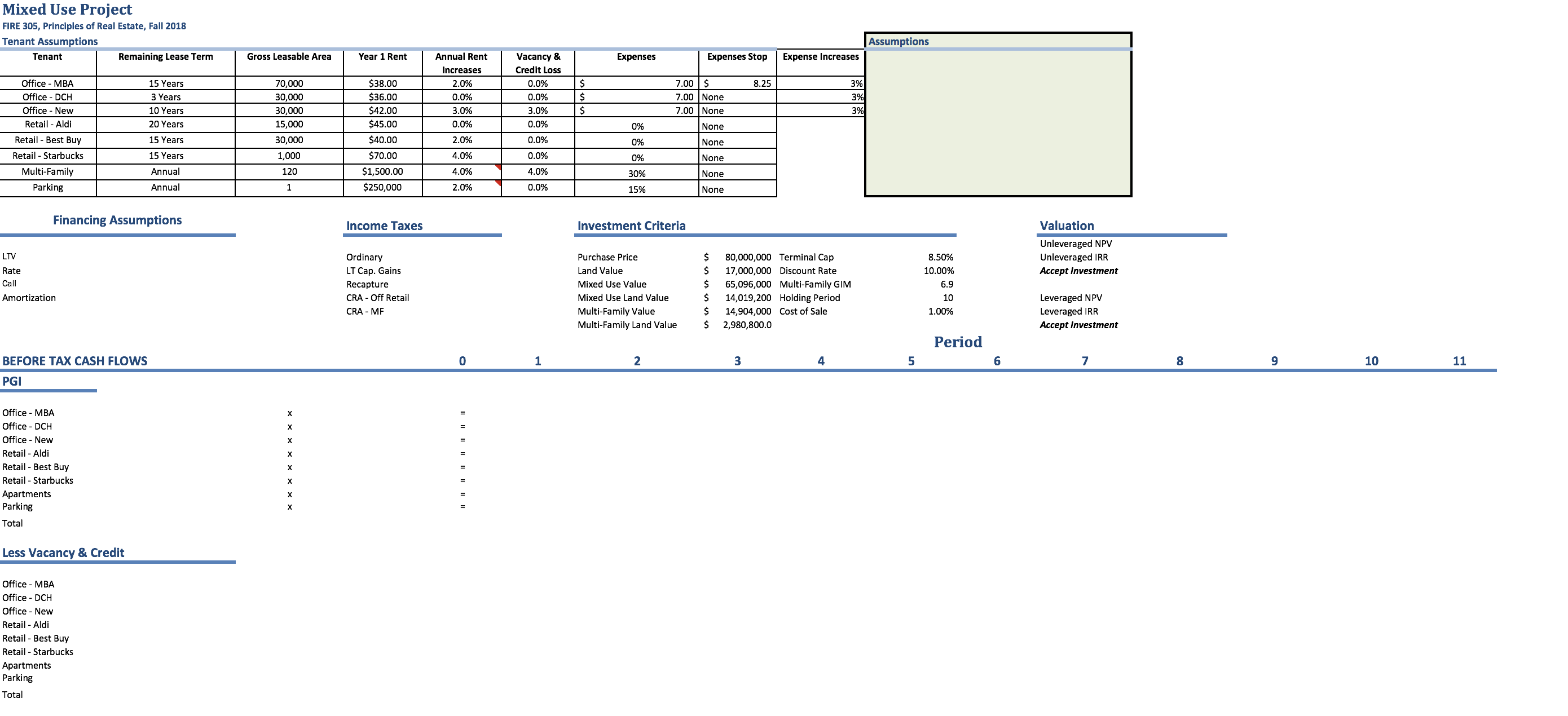

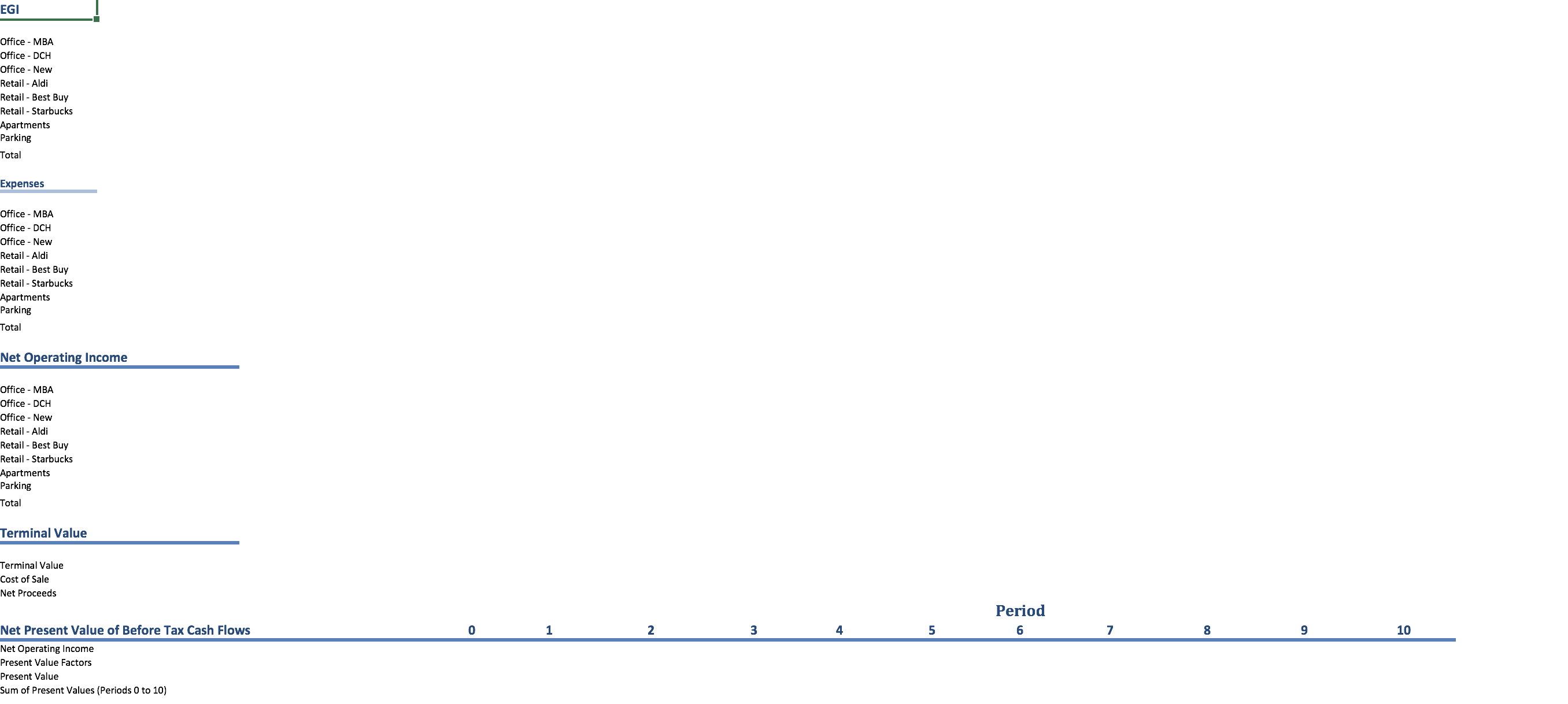

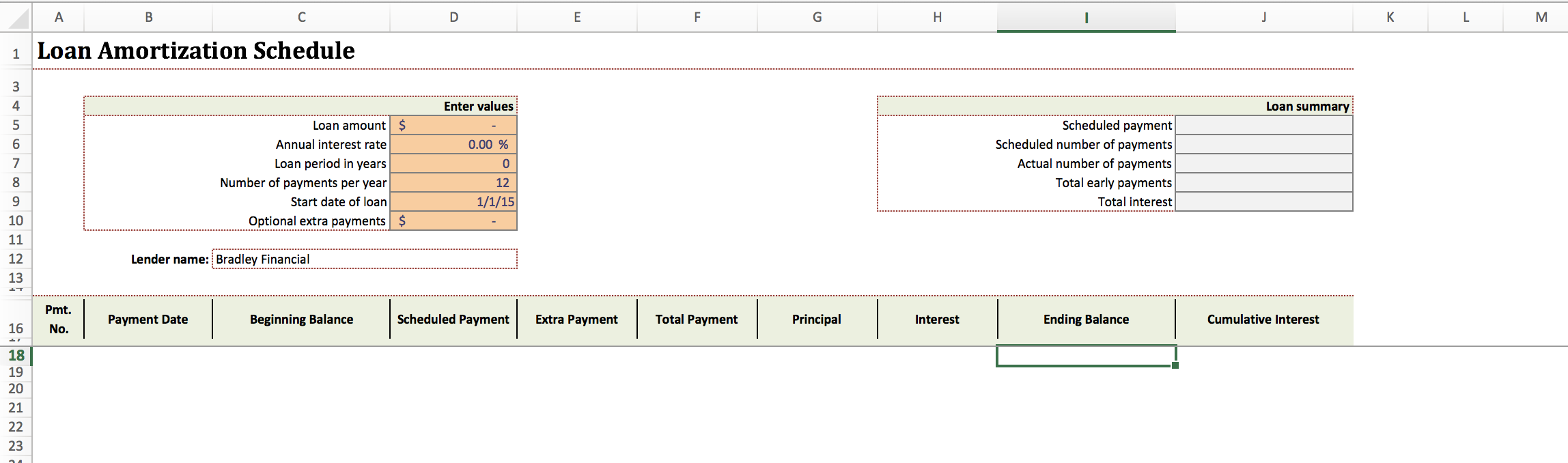

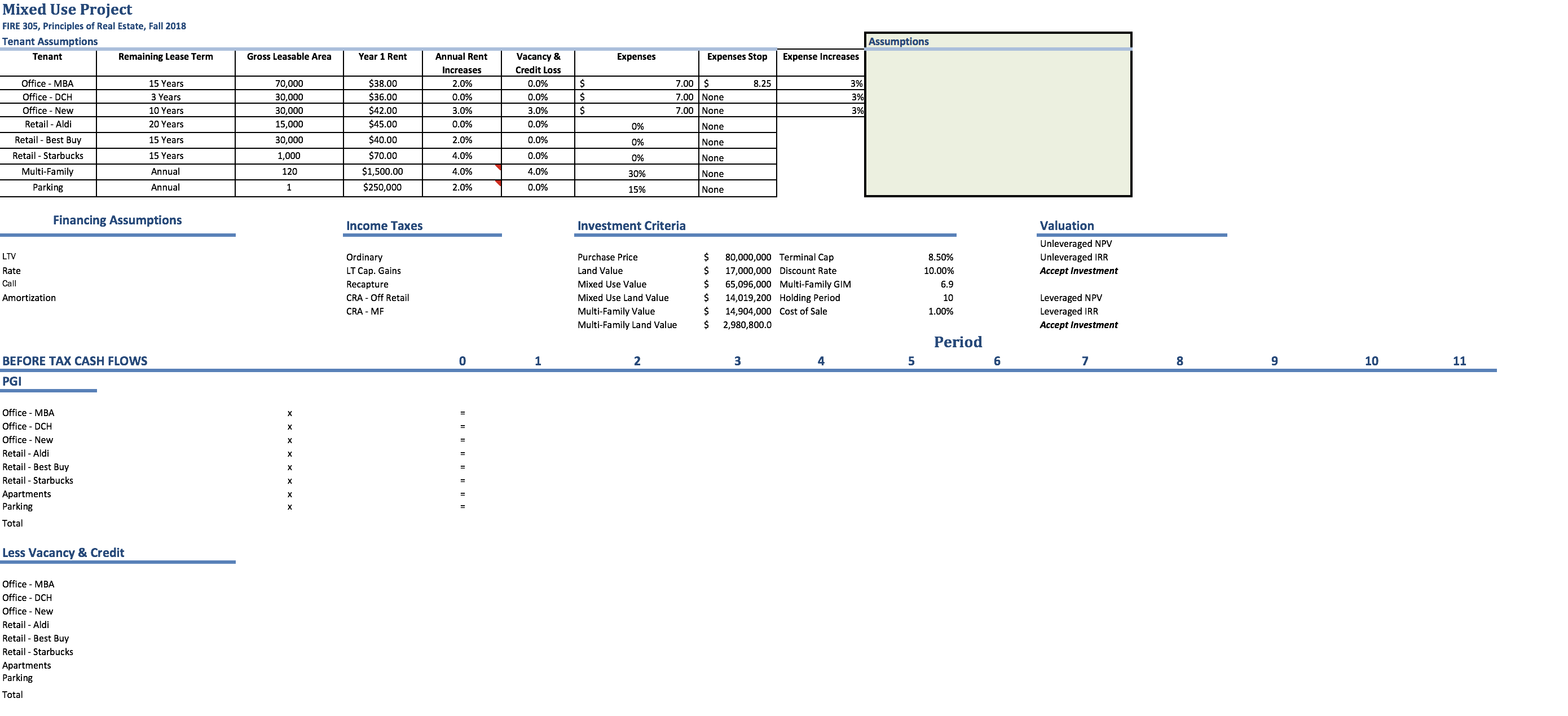

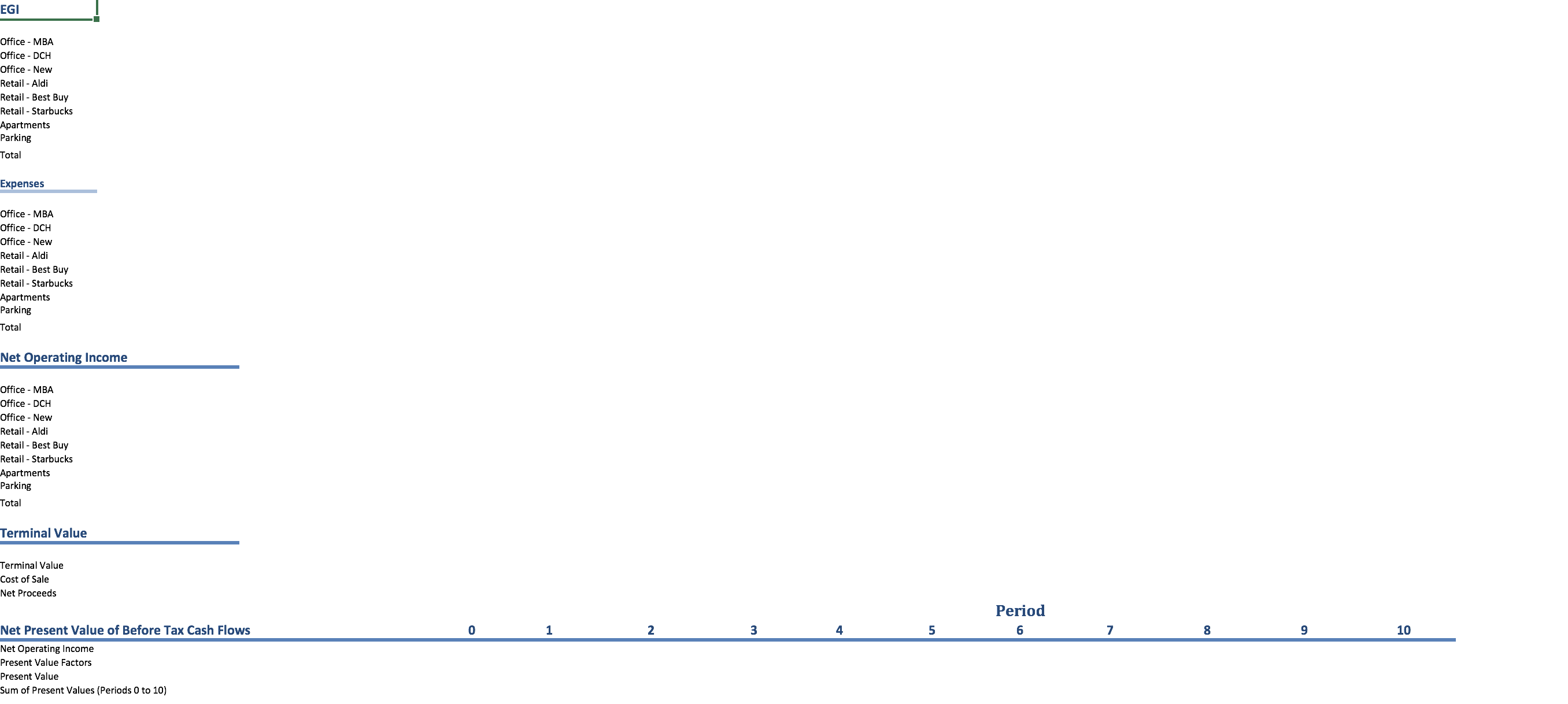

Mixed Use Project FIRE 305, Principles of Real Estate, Fall 2018 Tenant Assumptions Assumptions Tenant Remaining Lease Term Gross Leasable Area Year 1 Rent Annual Rent Vacancy & Expenses Expenses Stop Expense Increases Increases Credit Loss Office - MBA 15 Years 70,000 $38.00 2.0% 0.0% S 7.00 |$ 8.25 3% Office - DCH 3 Years 30.000 $36.00 0.0% 0.09 LS 7.00 | None 3% Office - New 10 Years 30,000 $42.00 3.0% 3.0% IS 7.00 |None 3% Retail - Aldi 20 Years 15,000 $45.00 0.09% 0.0% 0% None Retail - Best Buy 15 Years 30,000 $40.00 2.0% 0.09 0% None Retail - Starbucks 15 Years 1,000 $70.00 0.0% 0% None Multi-Family Annual 120 $1,500.00 4.0% 4.0% 30% None Parking Annua $250,000 2.0% 0.0% 15% None Financing Assumptions Income Taxes Investment Criteria Valuation Unleveraged NPV LTV Ordinary Purchase Price nu 80,000,000 Terminal Cap 8.50% Unleveraged IRR Rate LT Cap. Gains Land Value 7,000,000 Discount Rate 10.00% Accept Investment Call Recapture Mixed Use Value 65,096,000 Multi-Family GIM 6.9 Amortization CRA - Off Retail Mixed Use Land Value 14,019,200 Holding Period 10 Leveraged NPV CRA - MF Multi-Family Value 14,904,000 Cost of Sale 1.00% Leveraged IRR Multi-Family Land Value 2,980,800.0 Accept Investment Period BEFORE TAX CASH FLOWS 0 3 5 8 9 10 11 PGI Office - MBA Office - DCH Office - New x x x x x x xx Retail - Best Buy Retail - Starbucks Apartments Parking Total Less Vacancy & Credit Office - MBA - DCH Office - New Retail - Aldi Retail - Best Buy Retail - Starbucks Apartments Parking TotalEGI Office - MBA Office - DCH Office - New Retail - Aldi Retail - Best Buy Retail - Starbucks Apartments Parking Total Expenses Office - MBA Office - DCH Office - New Retail - Aldi Retail - Best Buy Retail - Starbucks Apartments Parking Net Operating Income Office - MBA Office - DCH Office - New Retail - Aldi Retail - Best Buy Retail - Starbucks Apartments Parking Tota Terminal Value Terminal Value Cost of Sale let Proceeds Period Net Present Value of Before Tax Cash Flows 3 5 8 9 10 Net Operating Income Present Value Factors Present Value Sum of Present Values (Periods 0 to 10)Period Net Present Value of After Tax Cash Flows 0 5 6 8 9 10 Net Operating Income 000000 0 resent Value Factors 2,000000 000000 0 0.000000 2.000000 0.000000 0.000000 0.000000 0.000000 2.000000 000000 0 resent Value Sum of Present Values (Periods 0 to 10) Using NPV and IRR functions NPV If the NPV is positive, accept the investment. If the NPV is positive the IRR is greater than the required Total Value of the Property RR rate. Note the power of leverage. By financing, the investment has a higher NPV and IRR. Value from Net Reversion 9 69 69 Value from Cash Flows A D G K Loan Amortization Schedule .............................................. Enter values ........... ............ Loan summary Loan amount $ Scheduled payment Annual interest rate 0.00 % Scheduled number of payments Loan period in years Actual number of payments 50 NOVA Number of payments per year 12 Total early payments Start date of loan Total interest Optional extra payments ...............................................................-- $ Lender name: |Bradley ey Financial 13 .............. Pmt. Payment Date Beginning Balance Scheduled Payment Extra Payment Total Payment Principal Interest Ending Balance Cumulative Interest ON 16 18 19EXCEL PROJECT FIRE 305 Real Estate Investment Analysis You have been hired to perform an investment analysis for a high net worth individual to determine if they should purchase a commercial real estate property. The investment includes ofce, retail, apartments, and a parking deck. The following are the income characteristics: Ofce - 70,000 square feet is leased to a national tenant, Mortgage Bankers Association for $38 per square foot for the next 15 years. The rent will increase by 2 percent per year. There are expense stops for this tenant of $8.25 per square foot and there is no risk of vacancy or credit loss. 30,000 square feet is leased to a law firm, DCH for $36 per square foot for the next three years with no rent increases and there is no risk of vacancy or credit loss. At the end of three years they will vacate the space and it will take nine months to lease the space at which time the market rent is projected to be $42 per square foot with annual increases of 3 percent. The new tenant's lease term on this space is 10 years and the vacancy and credit loss is estimated at 3 percent. Ofce expenses for all ofce tenants are $7.00 per square foot and increase by 3 percent per year. Retail - 15,000 square feet is leased to Aldi for $45 per square foot with no rent increases on a triple net basis for the next 20 years and there is no risk of default. 30,000 square feet is leased to Best Buy for $40 per square foot triple net basis for the next 15 years with rents increasing 2 percent a year and there is no risk of vacancy or credit loss. Starbuck leases 1,000 square feet for $70 per square foot with rent increases of 4 percent per year on a triple net basis for 15 years and there is no risk of credit loss. Mufti-Family There is a mixture 120 one and two bedroom apartments that rent for $1,000 to $2,000 per month with the average rent of $1,500 per month. These rents increase by 4 percent a year and the unrecoverable expense ratio (i.e. expenses) is 30 percent. The market vacancy and credit loss for the apartments is 4 percent. Parking Deck There is a combination of parking for each of the property types. Some of the parking spaces are rented on a monthly basis where others are rented on a daily or hourly basis. The annual gross parking revenue is $250,000 per year with expenses of 15 percent of gross. It is anticipated that the parking revenue will increase by 2 percent per year. Financing- The Bank of Mellow is providing a 75 percent loan to value mortgage at 6.75 percent amortized over 25 years with a 10year call (balloon). Taxes Your investor has an ordinary income tax rate of 28 percent The long term capital gain taxes are 20 percent and depreciation recapture is 25 percent. Investment Criteria /Assumptions- The property is being offered for $80 million. The terminal cap rate is 8.50 percent and the discount rate is 10 percent. The holding period is 10 years. Assume that the land value is $17 million. Assume that the multi-family has a value based on a GIM of 6.9 and the land value is 20 percent of the $17 million. Use the appropriate depreciation periods. Also assume that the cost of sale at the end of the holding period is 1 percent. Questions: What are the annual cash flows for periods 1 to 11; what is the terminal value; what is the before and after tax NPV and IRR; what is the division of value between cash flows and resale? Do your recommend purchasing the property? Explain why or why not. Show all calculations PGI, EGI. Expenses, NOI, Taxes, etc. If unclear about something clearly state your assumptions