Please anwer the question as detaied as possible

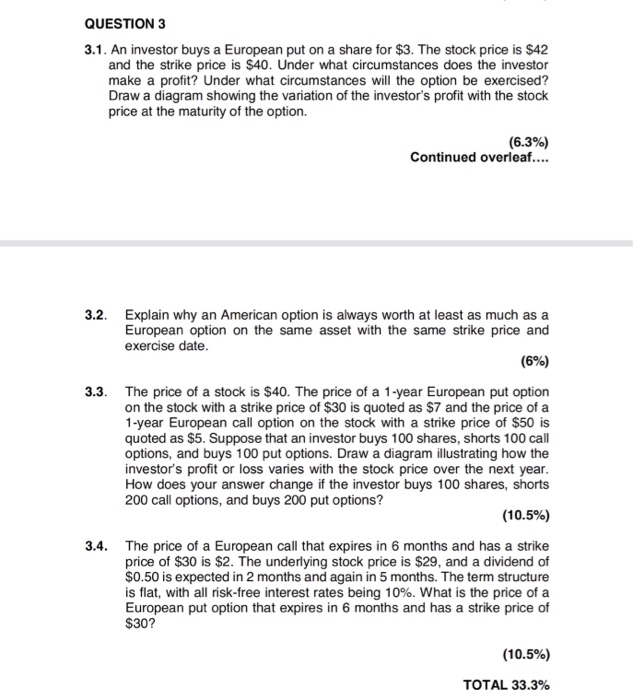

QUESTION 3 3.1. An investor buys a European put on a share for $3. The stock price is $42 and the strike price is $40. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option. (63%) Continued overleaf.... 3.2. Explain why an American option is always worth at least as much as a European option on the same asset with the same strike price and exercise date (6%) 3.3. The price of a stock is $40. The price of a 1-year European put option on the stock with a strike price of $30 is quoted as $7 and the price of a 1-year European call option on the stock with a strike price of $50 is quoted as $5. Suppose that an investor buys 100 shares, shorts 100 call options, and buys 100 put options. Draw a diagram illustrating how the investor's profit or loss varies with the stock price over the next year How does your answer change if the investor buys 100 shares, shorts 200 call options, and buys 200 put options? 5 3 (10.5%) 3.4. The price of a European call that expires in 6 months and has a strike price of $30 is $2. The underlying stock price is $29, and a dividend of $0.50 is expected in 2 months and again in 5 months. The term structure is flat, with all risk-free interest rates being 10%, what is the price of a European put option that expires in 6 months and has a strike price of $30? (10.5%) TOTAL 33.3% QUESTION 3 3.1. An investor buys a European put on a share for $3. The stock price is $42 and the strike price is $40. Under what circumstances does the investor make a profit? Under what circumstances will the option be exercised? Draw a diagram showing the variation of the investor's profit with the stock price at the maturity of the option. (63%) Continued overleaf.... 3.2. Explain why an American option is always worth at least as much as a European option on the same asset with the same strike price and exercise date (6%) 3.3. The price of a stock is $40. The price of a 1-year European put option on the stock with a strike price of $30 is quoted as $7 and the price of a 1-year European call option on the stock with a strike price of $50 is quoted as $5. Suppose that an investor buys 100 shares, shorts 100 call options, and buys 100 put options. Draw a diagram illustrating how the investor's profit or loss varies with the stock price over the next year How does your answer change if the investor buys 100 shares, shorts 200 call options, and buys 200 put options? 5 3 (10.5%) 3.4. The price of a European call that expires in 6 months and has a strike price of $30 is $2. The underlying stock price is $29, and a dividend of $0.50 is expected in 2 months and again in 5 months. The term structure is flat, with all risk-free interest rates being 10%, what is the price of a European put option that expires in 6 months and has a strike price of $30? (10.5%) TOTAL 33.3%