Question

Please assist with A-C! Thank you! Analyzing Risk and Return on Chargers Products' Investments Junior Sayou, a financial analyst for Chargers Products, a manufacturer of

Please assist with A-C! Thank you!

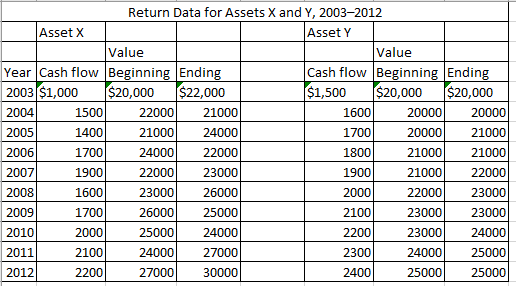

Analyzing Risk and Return on Chargers Products' Investments Junior Sayou, a financial analyst for Chargers Products, a manufacturer of stadium benches, must evaluate the risk and return of two assets, X and Y. The firm is considering adding these assets to its diversified asset portfolio. To assess the return and risk of each asset, Junior gathered data on the annual cash flow and beginning- and end-of-year values of each asset over the immediately preceding 10 years, 2003-2012. These data are summarized in the table below. Junior's investigation suggests that both assets, on average, will tend to perform in the future just as they have during the past 10 years. He therefore believes that the expected annual return can be estimated by finding the average annual return for each asset over the past 10 years.Junior believes that each asset's risk can be assessed in two ways: in isolation and as part of the firm's diversified portfolio of assets. The risk of the assets in isolation can be found by using the standard deviation and coefficient of variation of returns over the past 10 years. The capital asset pricing model(CAPM) can be used to assess the asset's risk as part of the firm's portfolio of assets. Applying some sophisticated quantitative techniques, Junior estimated betas for assets X and Y of 1.60 and 1.10,respectively. In addition, he found that the risk-free rate is currently 7.0% and that the market return is 10.0%.

To Do

a. Calculate the annual rate of return for each asset in each of the 10 preceding years, and use those values to find the average annual return for each asset over the 10-year period.

b. Use the returns calculated in part (a) to find (1) the standard deviation and (2) the coefficient of variation of the returns for each asset over the 10-year period 2003-2012.

c. Use your findings in parts (a) and (b) to evaluate and discuss the return and risk associated with each asset. Which asset appears to be preferable? Explain.

d. Use the CAPM to find the required return for each asset. Compare this value with the average annual returns calculated in part (a).

e. Compare and contrast your findings in parts (c) and (d). What recommendations would you give Junior with regard to investing in either of the two assets? Explain to Junior why he is better off using beta rather than the standard deviation and coefficient of variation to assess the risk of each asset.

f. Rework parts (d) and (e) under each of the following circumstances:

(1) A rise of 1.0% in inflationary expectations causes the risk-free rate to rise to 8.0% and the market return to rise to 11.0%.

(2) As a result of favorable political events, investors suddenly become less risk-averse, causing the market return to drop by 1.0 % to 9.0%.

Return Data for Assets X and Y, 2003-2012 Asset Asset Y Value Value Year lCash flow Beginning Endin Cash flow Beginning Endin 1,500 $20,000 $20,000 2003 $1,000 $20,000 $22,000 2004 2005 2006 1500 1400 1700 1900 1600 1700 2000 2100 2200 2200021000 21000 2 24000 22000 22000 23000 230002 26000 25000 250002 24000 2 27000 3 1600 1700 1800 1900 2000 2100 2200 2300 2400 2000021000 21000 21000 21000 22000 22000 23000 23000 23000 230002 24000 25000 24000 2008 2009 2010 2011 2012 26000 24000 27000 30000 24000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Everything Guide To Day Trading

Authors: David Borman

1st Edition

1440506213, 978-1440506215