Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please calculate by using Excel with full answer and show how to calculate it , thank you . Part 3) STC arranged a syndicated loan

Please calculate by using Excel with full answer and show how to calculate it , thank you .

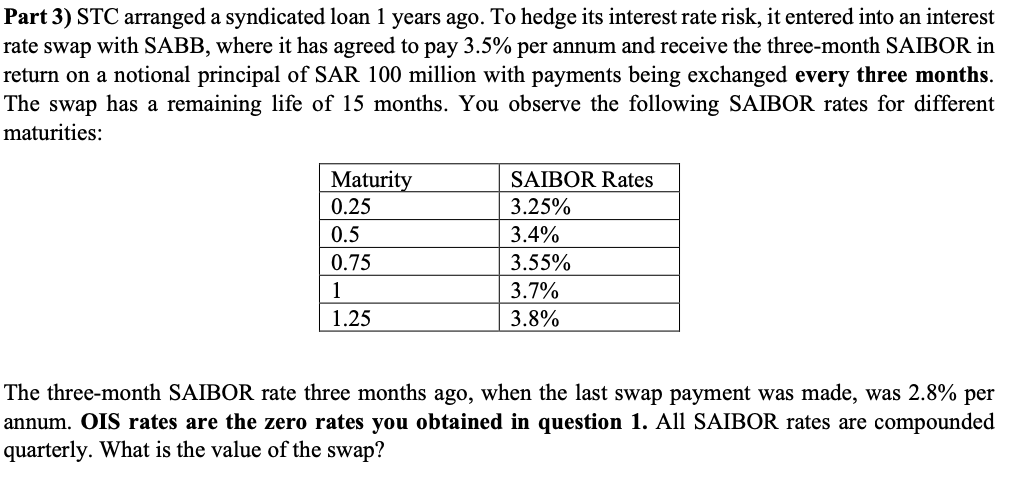

Part 3) STC arranged a syndicated loan 1 years ago. To hedge its interest rate risk, it entered into an interest rate swap with SABB, where it has agreed to pay 3.5% per annum and receive the three-month SAIBOR in return on a notional principal of SAR 100 million with payments being exchanged every three months. The swap has a remaining life of 15 months. You observe the following SAIBOR rates for different maturities: Maturity 0.25 0.5 0.75 1 1.25 SAIBOR Rates 3.25% 3.4% 3.55% 3.7% 3.8% The three-month SAIBOR rate three months ago, when the last swap payment was made, was 2.8% per annum. OIS rates are the zero rates you obtained in question 1. All SAIBOR rates are compounded quarterly. What is the value of the swapStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance Terms Financial Education Is Your Best Investment

Authors: Thomas Herold

1st Edition

1090822871, 978-1090822871