Answered step by step

Verified Expert Solution

Question

1 Approved Answer

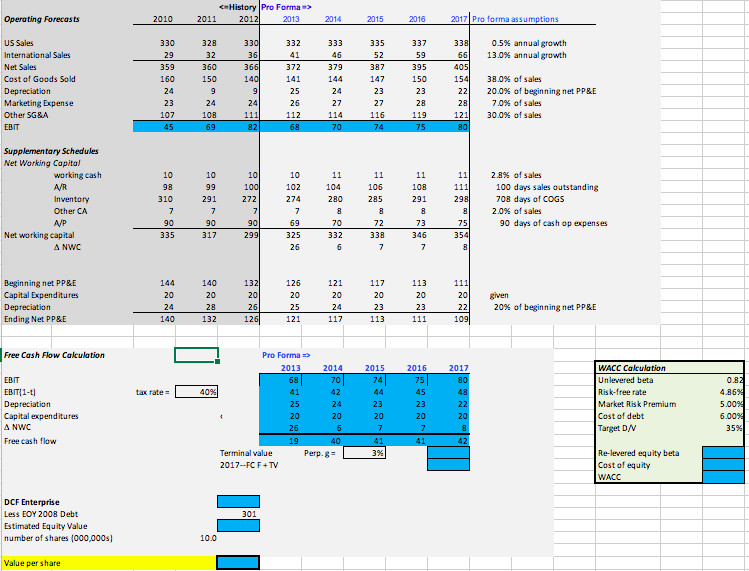

Please calculate WACC and DCF Enterprise 2013 2014 68 70 40%) 41 42 25 24 20 20 26 6 19 40 Terminal value Perp.gr 2017-FC

Please calculate WACC and DCF Enterprise

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Monetary Policy After The Great Recession The Role Of Interest Rates

Authors: Arkadiusz Sieron

1st Edition

0367471892, 978-0367471897