Question

please choose following accounts Accounts Payable Accumulated Depreciation - Buildings Accumulated Depreciation - Equipment Accumulated Depreciation - Leasehold Improvements Accumulated Depreciation - Machinery Accumulated Depreciation

please choose following accounts

Accounts Payable

Accumulated Depreciation - Buildings

Accumulated Depreciation - Equipment

Accumulated Depreciation - Leasehold Improvements

Accumulated Depreciation - Machinery

Accumulated Depreciation - Vehicle Overhaul

Accumulated Depreciation - Vehicles

Advertising Expense

Asset Retirement Obligation

Buildings

Cash

Common Shares

Contributed Surplus - Donated Capital

Cost of Goods Sold

Deferred Revenue - Government Grants

Depreciation Expense

Donation Revenue

Equipment

Finance Expense

Gain on Disposal of Buildings

Gain on Disposal of Equipment

Gain on Disposal of Machinery

Gain on Disposal of Vehicles

Gain on Vehicle Overhaul

Gain or Loss in Value of Investment Property

GST Receivable

Interest Expense

Interest Payable

Inventory

Investment Property

Land

Land Improvements

Legal Expense

Loss on Disposal of Buildings

Loss on Disposal of Equipment

Loss on Disposal of Machinery

Loss on Disposal of Vehicles

Loss on Vehicle Overhaul

Machinery

Mineral Resources

Mortgage Payable

No Entry

Notes Payable

Office Expense

Prepaid Expenses

Prepaid Insurance

Purchase Discounts

Repairs and Maintenance Expense

Revaluation Gain or Loss

Revaluation Surplus (AOCI)

Revaluation Surplus (OCI)

Revenue - Government Grants

Salaries and Wages Expense

Sales Revenue

Service Revenue

Supplies

Tenant Deposits Liability

Vehicle Overhaul

Vehicles

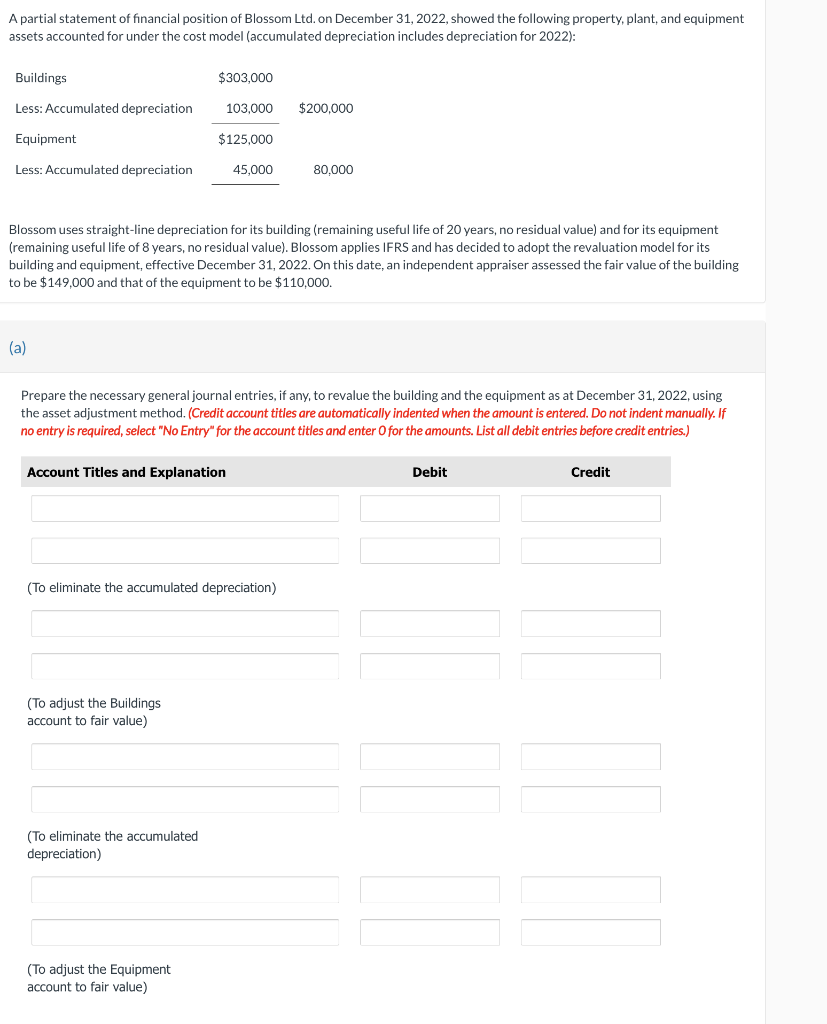

A partial statement of financial position of Blossom Ltd. on December 31, 2022, showed the following property, plant, and equipment assets accounted for under the cost model (accumulated depreciation includes depreciation for 2022): Blossom uses straight-line depreciation for its building (remaining useful life of 20 years, no residual value) and for its equipment (remaining useful life of 8 years, no residual value). Blossom applies IFRS and has decided to adopt the revaluation model for its building and equipment, effective December 31, 2022. On this date, an independent appraiser assessed the fair value of the building to be $149,000 and that of the equipment to be $110,000. (a) Prepare the necessary general journal entries, if any, to revalue the building and the equipment as at December 31,2022 , using the asset adjustment method. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Corporate Culture Audit

Authors: Nigel Bristow, Sarah J. Sandberg

1st Edition

095597075X, 978-0955970757