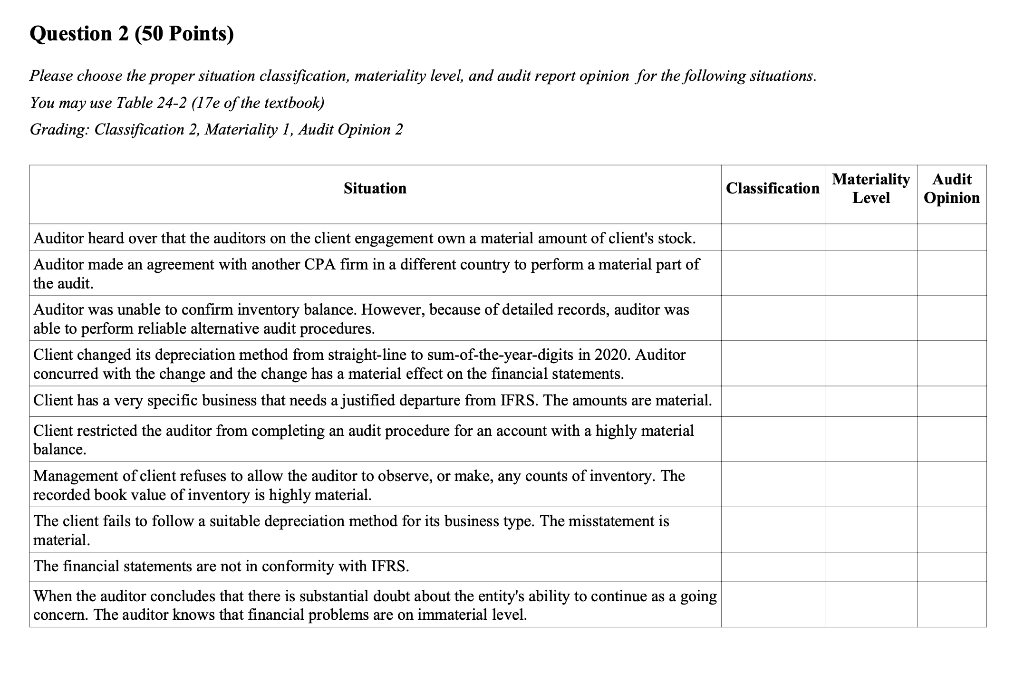

Question

Please choose the proper situation classification, materiality level, and audit report opinion for the following situations. You may use Table 24-2 (17e of the textbook)

Please choose the proper situation classification, materiality level, and audit report opinion for the following situations. You may use Table 24-2 (17e of the textbook) Grading: Classification 2, Materiality 1, Audit Opinion 2

| Situation | Classification | Materiality Level | Audit Opinion |

| Auditor heard over that the auditors on the client engagement own a material amount of client's stock. | |||

| Auditor made an agreement with another CPA firm in a different country to perform a material part of the audit. | |||

| Auditor was unable to confirm inventory balance. However, because of detailed records, auditor was able to perform reliable alternative audit procedures. | |||

| Client changed its depreciation method from straight-line to sum-of-the-year-digits in 2020. Auditor concurred with the change and the change has a material effect on the financial statements. | |||

| Client has a very specific business that needs a justified departure from IFRS. The amounts are material. | |||

| Client restricted the auditor from completing an audit procedure for an account with a highly material balance. | |||

| Management of client refuses to allow the auditor to observe, or make, any counts of inventory. The recorded book value of inventory is highly material. | |||

| The client fails to follow a suitable depreciation method for its business type. The misstatement is material. | |||

| The financial statements are not in conformity with IFRS. | |||

| When the auditor concludes that there is substantial doubt about the entity's ability to continue as a going concern. The auditor knows that financial problems are on immaterial level. |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

COSHH Audit Control Of Substances Hazardous To Health A Complete Guide To Understanding A COSHH Audt For Your Business

Authors: HASTAM

1st Edition

1852520981, 978-1852520984