Answered step by step

Verified Expert Solution

Question

1 Approved Answer

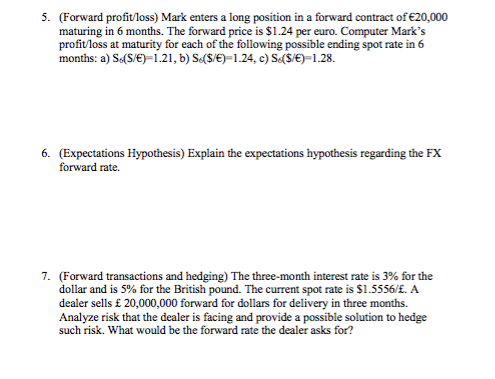

Please complete all and show ALL work. Thank you!! 5. (Forward profit/loss) Mark enters a long position in a forward contract ofE20,000 maturing in 6

Please complete all and show ALL work. Thank you!!

5. (Forward profit/loss) Mark enters a long position in a forward contract ofE20,000 maturing in 6 months. The forward price is $1.24 per euro. Computer Mark's profit/loss at maturity for each ofthe following possible ending spotrate in 6 months: a) So(Sve) 1.21, b Se($e) 1.24, c) Se($/E) 1.28. 6. (Expectations Hypothesis) Explain the expectations hypothesis regarding the FX forward rate. 7. (Forward transactions and hedging) The three-month interest rate is 3% for the dollar and is 5% for the British pound. The current spot rate is si-5556E. A dealer sells f 20,000,000 forward for dollars for delivery in three months. Analyze risk that the dealer is facing and provide apossible solution to hedge such risk. What would be the forward rate the dealer asks for

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

TExES Business And Finance Secrets Study Guide

Authors: TExES Exam Secrets Test Prep Team

1st Edition

1516706862, 978-1516706860