Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please compute d1 and d2. (50 points) Suppose that the stock price follows a geometric Brownian motion: dSt = u Stdt + SidBt, where u

Please compute d1 and d2.

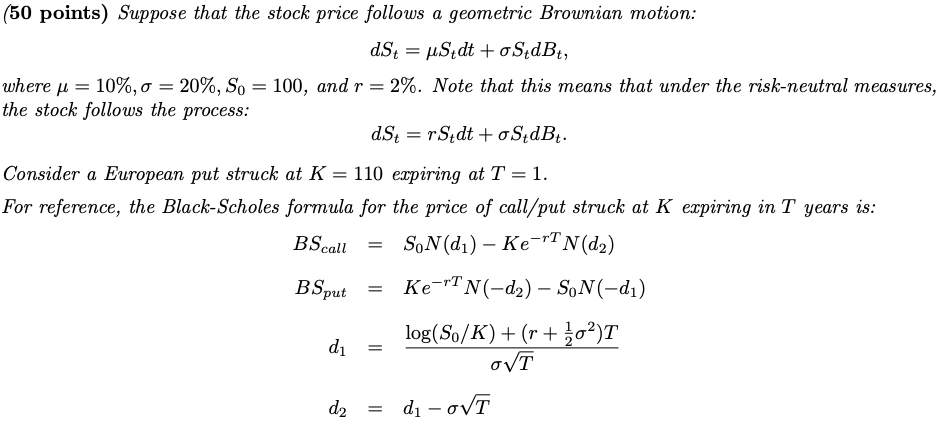

(50 points) Suppose that the stock price follows a geometric Brownian motion: dSt = u Stdt + SidBt, where u = 10%, o = 20%, So = 100, and r = 2%. Note that this means that under the risk-neutral measures, the stock follows the process: dSt = rStdt + oS dBt. = Consider a European put struck at K = 110 expiring at T = 1. For reference, the Black-Scholes formula for the price of call/put struck at K expiring in T years is: BScall SoN(di) - Ke-rT Nd2) Ke-'T N(-d) SoN(-d) log(S./K) + (r + Z02)T di NT B Sput = d2 -di-ovtStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Applications And Theory

Authors: Marcia Cornett, Troy Adair, John Nofsinger

5th Edition

1260013987, 9781260013986