Answered step by step

Verified Expert Solution

Question

1 Approved Answer

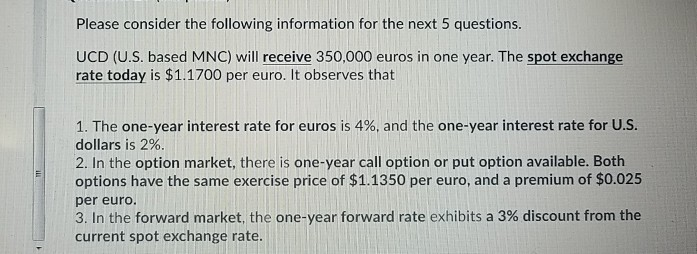

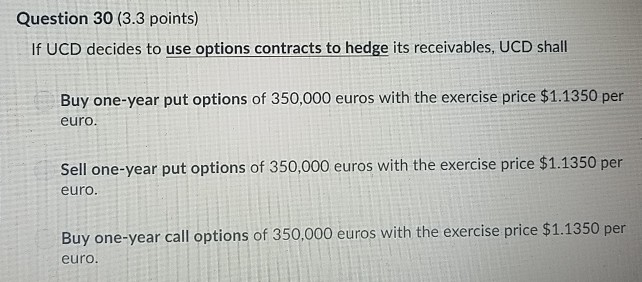

Please consider the following information for the next 5 question:s UCD (U.S. based MNC) will receive 350,000 euros in one year. The spot exchange rate

Please consider the following information for the next 5 question:s UCD (U.S. based MNC) will receive 350,000 euros in one year. The spot exchange rate today is $1.1700 per euro. It observes that I. The one-year interest rate for euros is 4%, and the one-year interest rate for U.S dollars is 2%. 2. In the option market, there is one-year call option or put option available. Both options have the same exercise price of $1.1350 per euro, and a premium of $0.025 per euro. 3. In the forward market, the one-year forward rate exhibits a 3% discount from the current spot exchange rate. Question 30 (3.3 points) If UCD decides to use options contracts to hedge its receivables, UCD shall Buy one-year put options of 350,000 euros with the exercise price $1.1350 per euro Sell one-year put options of 350,000 euros with the exercise price $1.1350 per euro. Buy one-year call options of 350.000 euros with the exercise price $1.1350 per euro

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles and Applications

Authors: Sheridan Titman, Arthur Keown, John Martin

12th edition

133423824, 978-0133423822