Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE DO ALL QUESTIONS BECAUSE IT'S NOT MUTILPLE QUESTIONS IT'S JUST 1. top picture: Picture of actual problem bottom picture: solution to similar problem please

PLEASE DO ALL QUESTIONS BECAUSE IT'S NOT MUTILPLE QUESTIONS IT'S JUST 1.

top picture: Picture of actual problem

bottom picture: solution to similar problem please follow formula

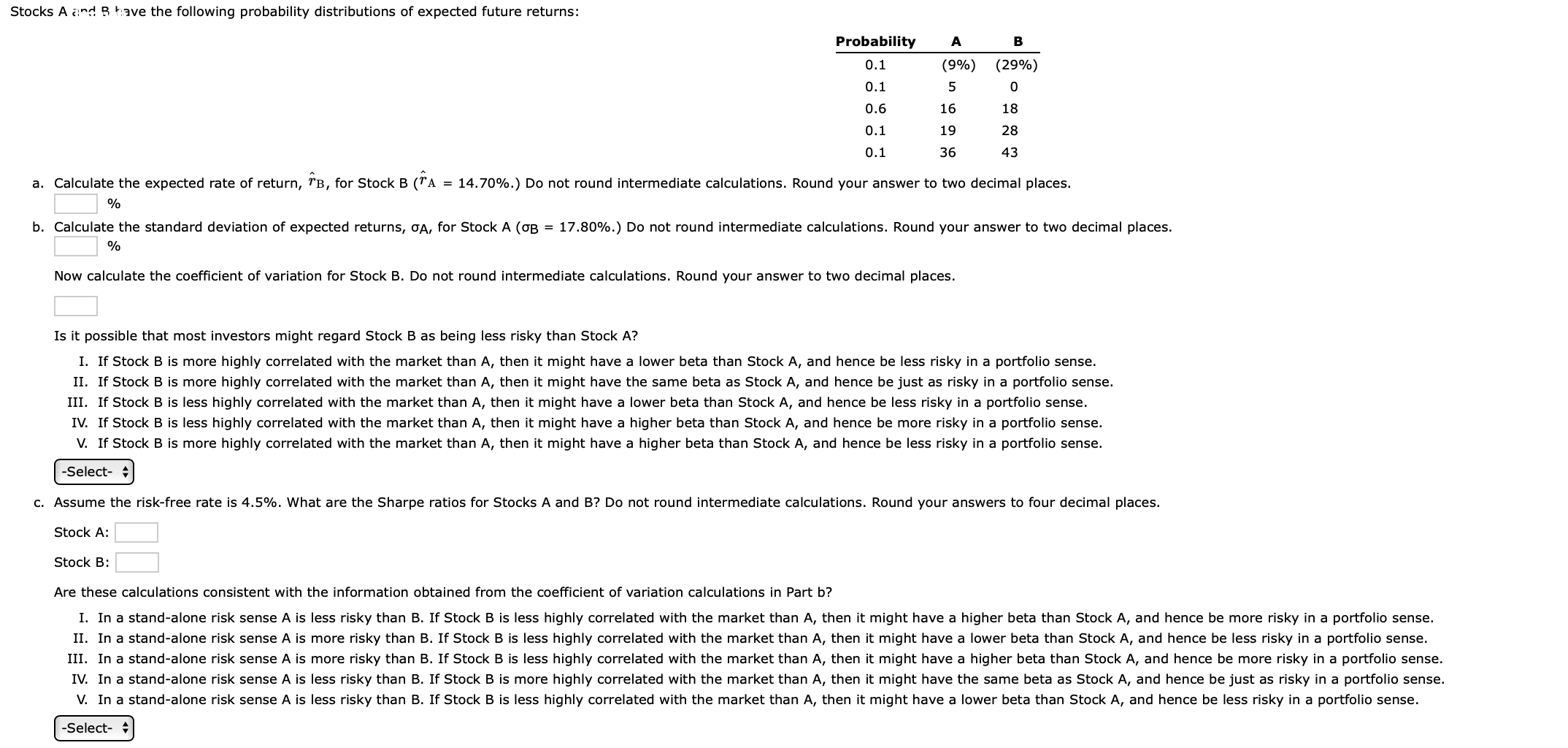

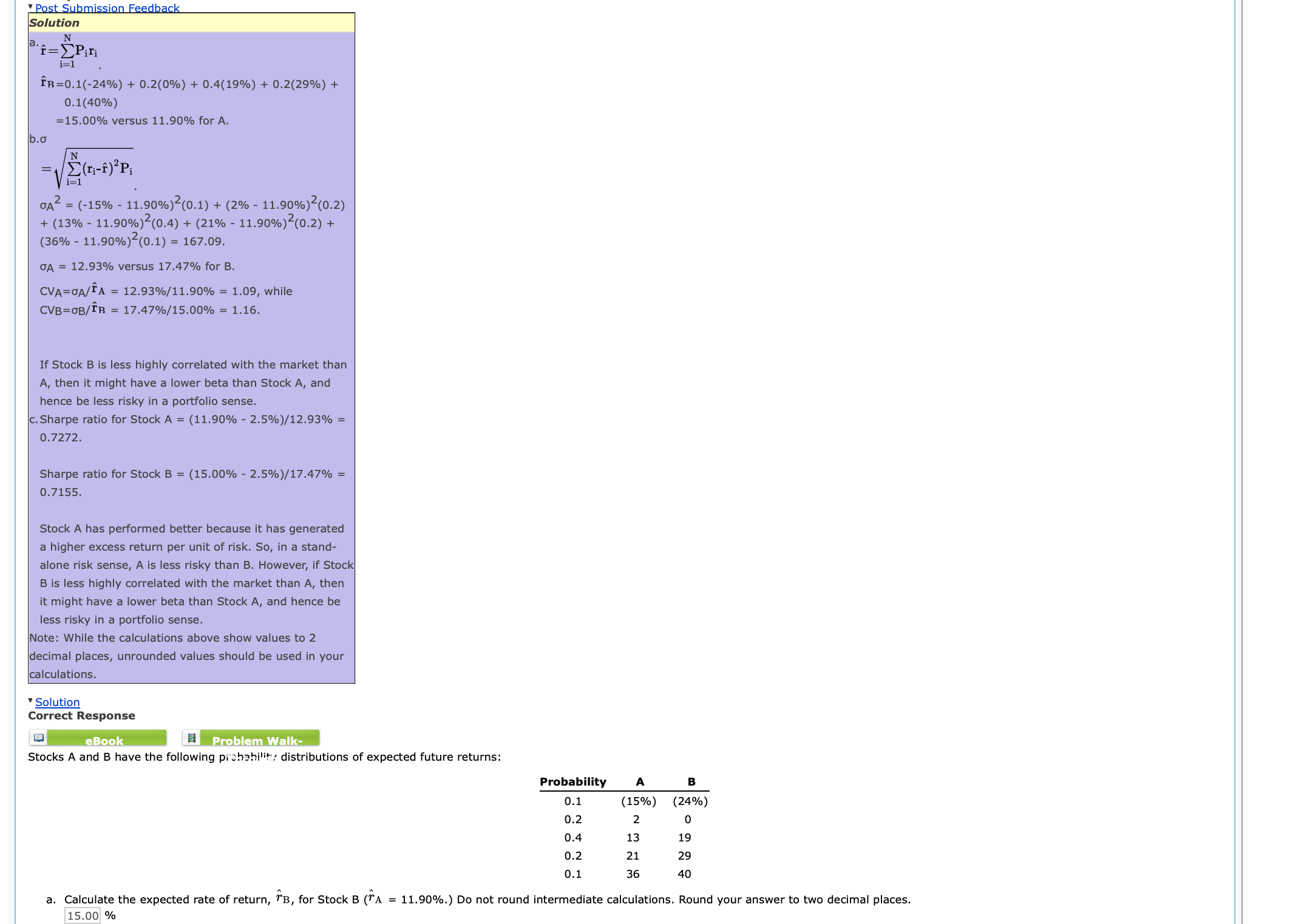

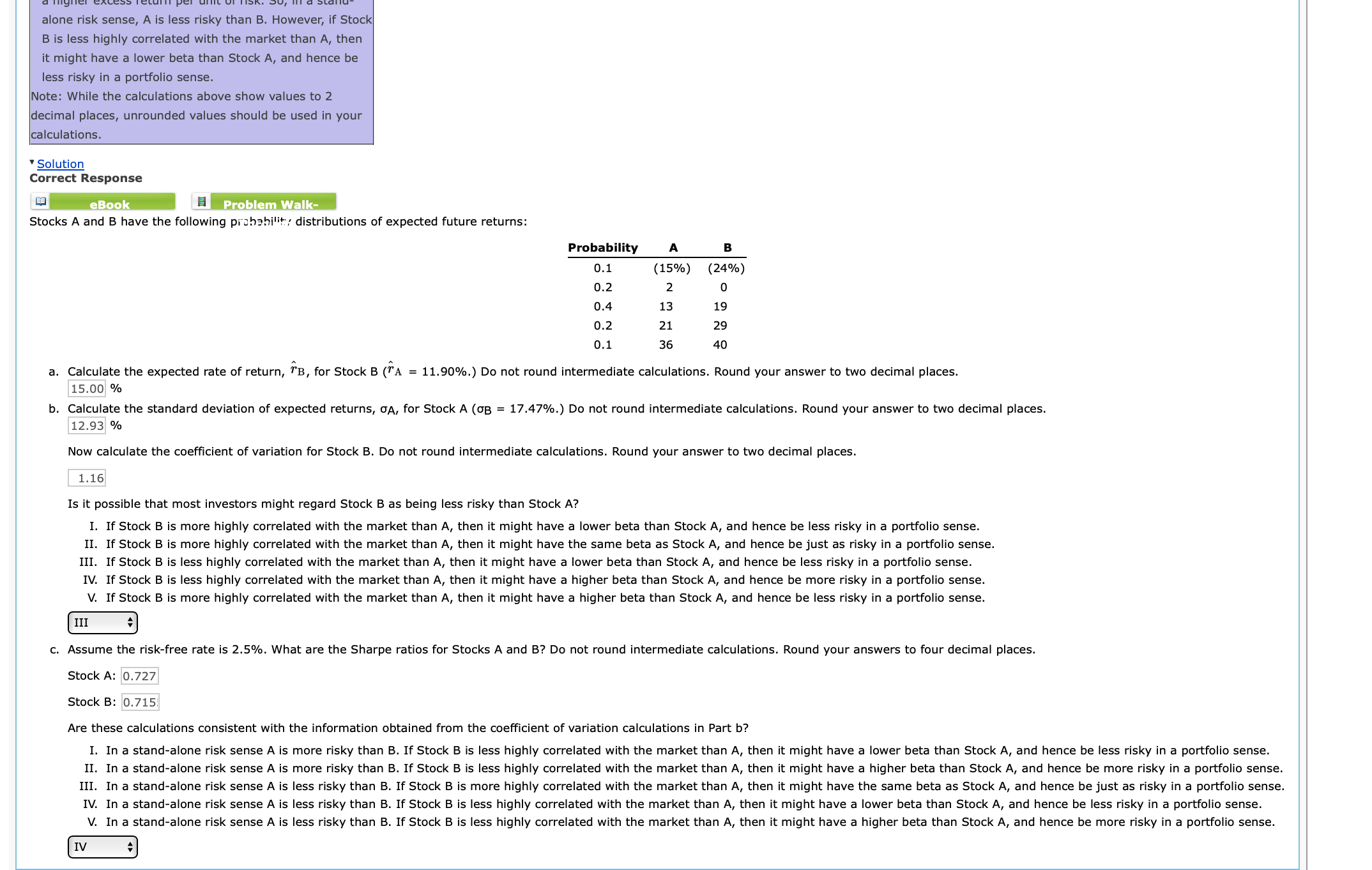

Stocks A ind R have the following probability distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=14.70%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A(B=17.80%.) Do not round intermediate calculations. Round your answer to two decimal places. % Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than Stock A ? I. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. c. Assume the risk-free rate is 4.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? Post Submission Feedback Solution a2r^=i=1NPirir^B=0.1(24%)+0.2(0%)+0.4(19%)+0.2(29%)+0.1(40%)=15.00%versus11.90%forA.=i=1N(rir^)2PiA2=(15%11.90%)2(0.1)+(2%11.90%)2(0.2)+(13%11.90%)2(0.4)+(21%11.90%)2(0.2)+(36%11.90%)2(0.1)=167.09. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. c. Sharpe ratio for Stock A=(11.90%2.5%)/12.93%= 0.7272 . Sharpe ratio for Stock B =(15.00%2.5%)/17.47%= 0.7155 . Stock A has performed better because it has generated a higher excess return per unit of risk. So, in a standalone risk sense, A is less risky than B. However, if Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Note: While the calculations above show values to 2 decimal places, unrounded values should be used in your calculations. Solution Correct Response Stocks A and B have the following prohhilit:; distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=11.90%.) Do not rot alone risk sense, A is less risky than B. However, if Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Note: While the calculations above show values to 2 decimal places, unrounded values should be used in your calculations. Solution Correct Response Stocks A and B have the following probhilit: distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=11.90%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A ( B=17.47%.) Do not round intermediate calculations. Round your answer to two decimal places. % Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. 16 Is it possible that most investors might regard Stock B as being less risky than Stock A ? I. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. c. Assume the risk-free rate is 2.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four Stock A : Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b

Stocks A ind R have the following probability distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=14.70%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A(B=17.80%.) Do not round intermediate calculations. Round your answer to two decimal places. % Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than Stock A ? I. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. c. Assume the risk-free rate is 4.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? Post Submission Feedback Solution a2r^=i=1NPirir^B=0.1(24%)+0.2(0%)+0.4(19%)+0.2(29%)+0.1(40%)=15.00%versus11.90%forA.=i=1N(rir^)2PiA2=(15%11.90%)2(0.1)+(2%11.90%)2(0.2)+(13%11.90%)2(0.4)+(21%11.90%)2(0.2)+(36%11.90%)2(0.1)=167.09. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. c. Sharpe ratio for Stock A=(11.90%2.5%)/12.93%= 0.7272 . Sharpe ratio for Stock B =(15.00%2.5%)/17.47%= 0.7155 . Stock A has performed better because it has generated a higher excess return per unit of risk. So, in a standalone risk sense, A is less risky than B. However, if Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Note: While the calculations above show values to 2 decimal places, unrounded values should be used in your calculations. Solution Correct Response Stocks A and B have the following prohhilit:; distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=11.90%.) Do not rot alone risk sense, A is less risky than B. However, if Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Note: While the calculations above show values to 2 decimal places, unrounded values should be used in your calculations. Solution Correct Response Stocks A and B have the following probhilit: distributions of expected future returns: a. Calculate the expected rate of return, r^B, for Stock B(r^A=11.90%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, A, for Stock A ( B=17.47%.) Do not round intermediate calculations. Round your answer to two decimal places. % Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. 16 Is it possible that most investors might regard Stock B as being less risky than Stock A ? I. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. c. Assume the risk-free rate is 2.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four Stock A : Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ABC Finance Coloring Book Familys First Financial Literacy Book

Authors: Jason Conger

1st Edition

1955961026, 978-1955961028