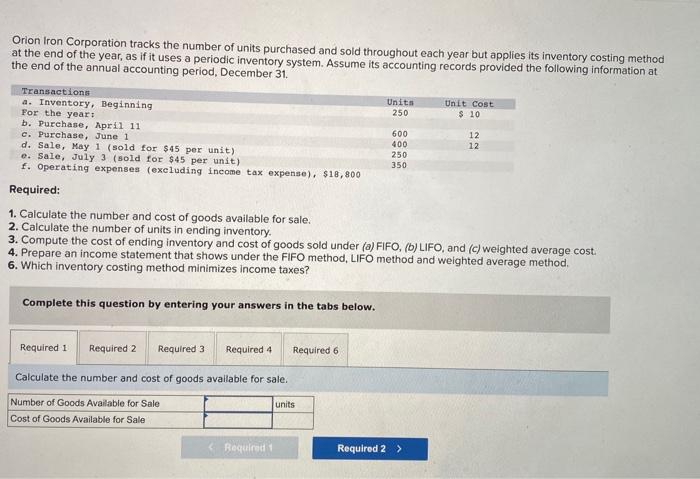

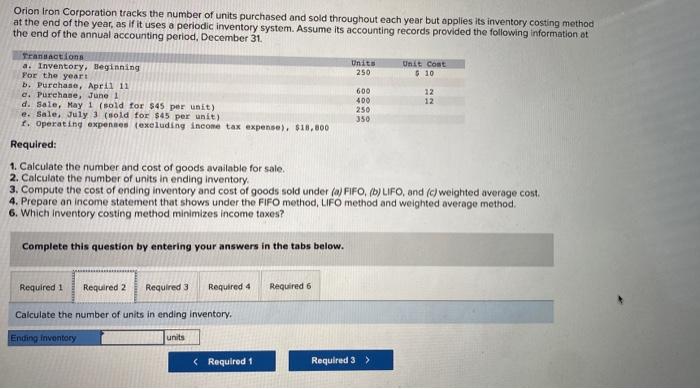

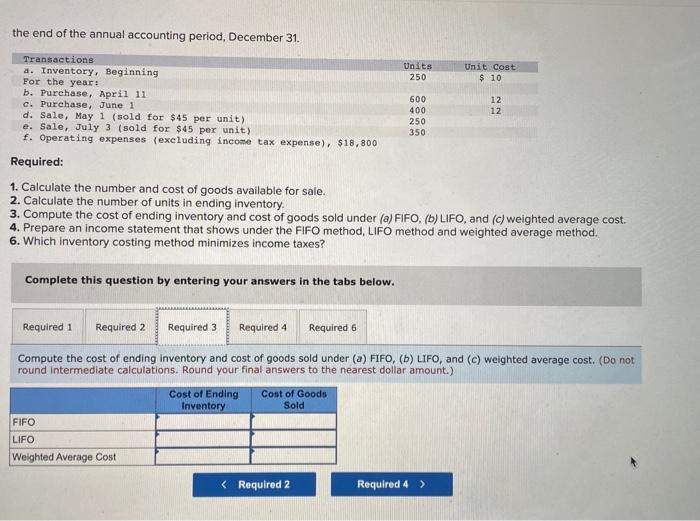

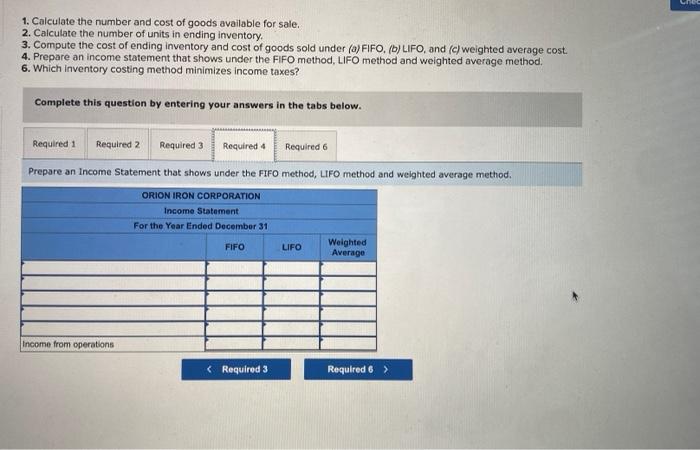

Orion Iron Corporation tracks the number of units purchased and sold throughout each year but applies its inventory costing method at the end of the year, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31 . Required: 1. Calculate the number and cost of goods available for sale. 2. Calculate the number of units in ending inventory. 3. Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. 4. Prepare an income statement that shows under the FIFO method, LIFO method and weighted average method. 5. Which inventory costing method minimizes income taxes? Complete this question by entering your answers in the tabs below. Calculate the number and cost of goods available for sale. Orion Iron Corporation tracks the number of units purchased and sold throughout each year but applies its inventory costing method at the end of the year, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31. Required: 1. Calculate the number and cost of goods available for sale. 2. Calculate the number of units in ending inventory. 3. Compute the cost of ending inventory and cost of goods sold under (a) FFO, (b) LIFO, and (c) weighted average cost. 4. Prepare an income statement that shows under the FiFO method, LIFO method and weighted average method. 6. Which inventory costing method minimizes income taxes? Complete this question by entering your answers in the tabs below. Caiculate the number of units in ending inventory. the end of the annual accounting period, December 31 . Required: 1. Calculate the number and cost of goods available for sale. 2. Calculate the number of units in ending inventory. 3. Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. 4. Prepare an income statement that shows under the FIFO method, LIFO method and weighted average method. 6. Which inventory costing method minimizes income taxes? Complete this question by entering your answers in the tabs below. Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. (Do not round intermediate calculations. Round your final answers to the nearest dollar amount.) 1. Calculate the number and cost of goods available for sale. 2. Calculate the number of units in ending inventory. 3. Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. 4. Prepare an income statement that shows under the FIFO method, LIFO method and weighted average method. 6. Which inventory costing method minimizes income taxes? Complete this question by entering your answers in the tabs below. Prepare an income Statement that shows under the FIFO method, LFF method and welghted average method. the end of the annual accounting period, December 31 . Kequired: 1. Calculate the number and cost of goods available for sale. 2. Calculate the number of units in ending inventory. 3. Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. 4. Prepare an income statement that shows under the FIFO method, LIFO method and weighted average method. 6. Which inventory costing method minimizes income taxes? Complete this question by entering your answers in the tabs below. Which inventory costing method minimizes income taxes