Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please do help with the whole question. Appreciate it. Question 3 You are given the following information: Name UK Govt bonds 9.6%, maturing 20 Oct

Please do help with the whole question. Appreciate it.

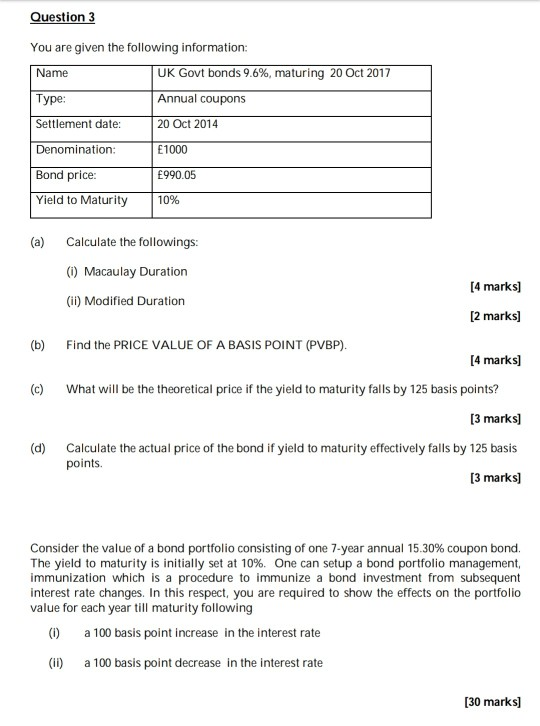

Question 3 You are given the following information: Name UK Govt bonds 9.6%, maturing 20 Oct 2017 Type: Annual coupons Settlement date: 20 Oct 2014 Denomination: Bond price: Yield to Maturity E1000 E990.05 10% Calculate the followings: (1) Macaulay Duration (4 marks) (ii) Modified Duration [2 marks] (b) Find the PRICE VALUE OF A BASIS POINT (PVBP). [4 marks) (c) What will be the theoretical price if the yield to maturity falls by 125 basis points? (d) [3 marks) Calculate the actual price of the bond if yield to maturity effectively falls by 125 basis points. [3 marks) Consider the value of a bond portfolio consisting of one 7-year annual 15.30% coupon bond The yield to maturity is initially set at 10%. One can setup a bond portfolio management, immunization which is a procedure to immunize a bond investment from subsequent interest rate changes. In this respect, you are required to show the effects on the portfolio value for each year till maturity following 0 a 100 basis point increase in the interest rate (11) a 100 basis point decrease in the interest rate [30 marks) Question 3 You are given the following information: Name UK Govt bonds 9.6%, maturing 20 Oct 2017 Type: Annual coupons Settlement date: 20 Oct 2014 Denomination: Bond price: Yield to Maturity E1000 E990.05 10% Calculate the followings: (1) Macaulay Duration (4 marks) (ii) Modified Duration [2 marks] (b) Find the PRICE VALUE OF A BASIS POINT (PVBP). [4 marks) (c) What will be the theoretical price if the yield to maturity falls by 125 basis points? (d) [3 marks) Calculate the actual price of the bond if yield to maturity effectively falls by 125 basis points. [3 marks) Consider the value of a bond portfolio consisting of one 7-year annual 15.30% coupon bond The yield to maturity is initially set at 10%. One can setup a bond portfolio management, immunization which is a procedure to immunize a bond investment from subsequent interest rate changes. In this respect, you are required to show the effects on the portfolio value for each year till maturity following 0 a 100 basis point increase in the interest rate (11) a 100 basis point decrease in the interest rate [30 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Value Based Management Context And Application

Authors: Glen Arnold, Matt Davies

1st Edition

0471899860, 978-0471899860