Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please do it in 25 minutes please urgently... I'll give you up thumb definitely XYZ Corporation enters into a 6-year interest rate swap with a

please do it in 25 minutes please urgently... I'll give you up thumb definitely

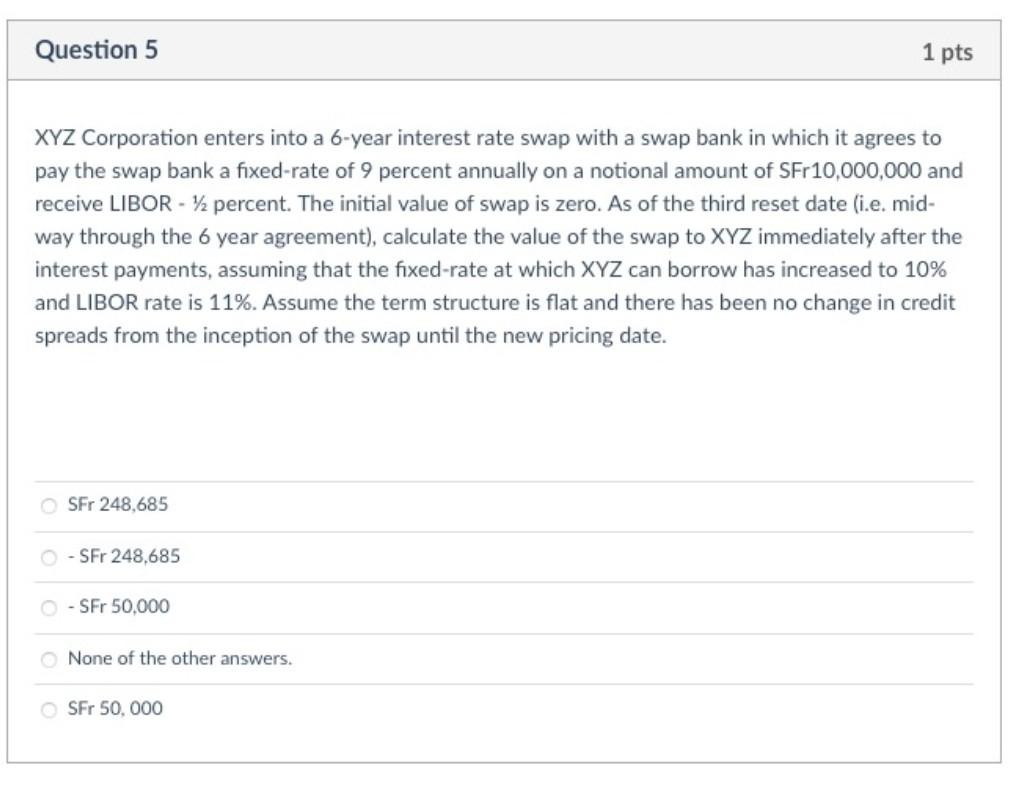

XYZ Corporation enters into a 6-year interest rate swap with a swap bank in which it agrees to pay the swap bank a fixed-rate of 9 percent annually on a notional amount of SFr10,000,000 and receive LIBOR - 1/2 percent. The initial value of swap is zero. As of the third reset date (i.e. midway through the 6 year agreement), calculate the value of the swap to XYZ immediately after the interest payments, assuming that the fixed-rate at which XYZ can borrow has increased to 10% and LIBOR rate is 11%. Assume the term structure is flat and there has been no change in credit spreads from the inception of the swap until the new pricing date. SFr 248,685 - SFr 248,685 - SFr 50,000 None of the other answers. SFr 50,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Reinventing The CFO How Financial Managers Can Transform Their Roles And Add Greater Value

Authors: Jeremy Hope

1st Edition

1591399459, 978-1591399452