Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please do it in 30 minutes will upvote use Excel Question #2 (20 points total) You are evaluating two risky stocks, A and B, with

please do it in 30 minutes will upvote use Excel

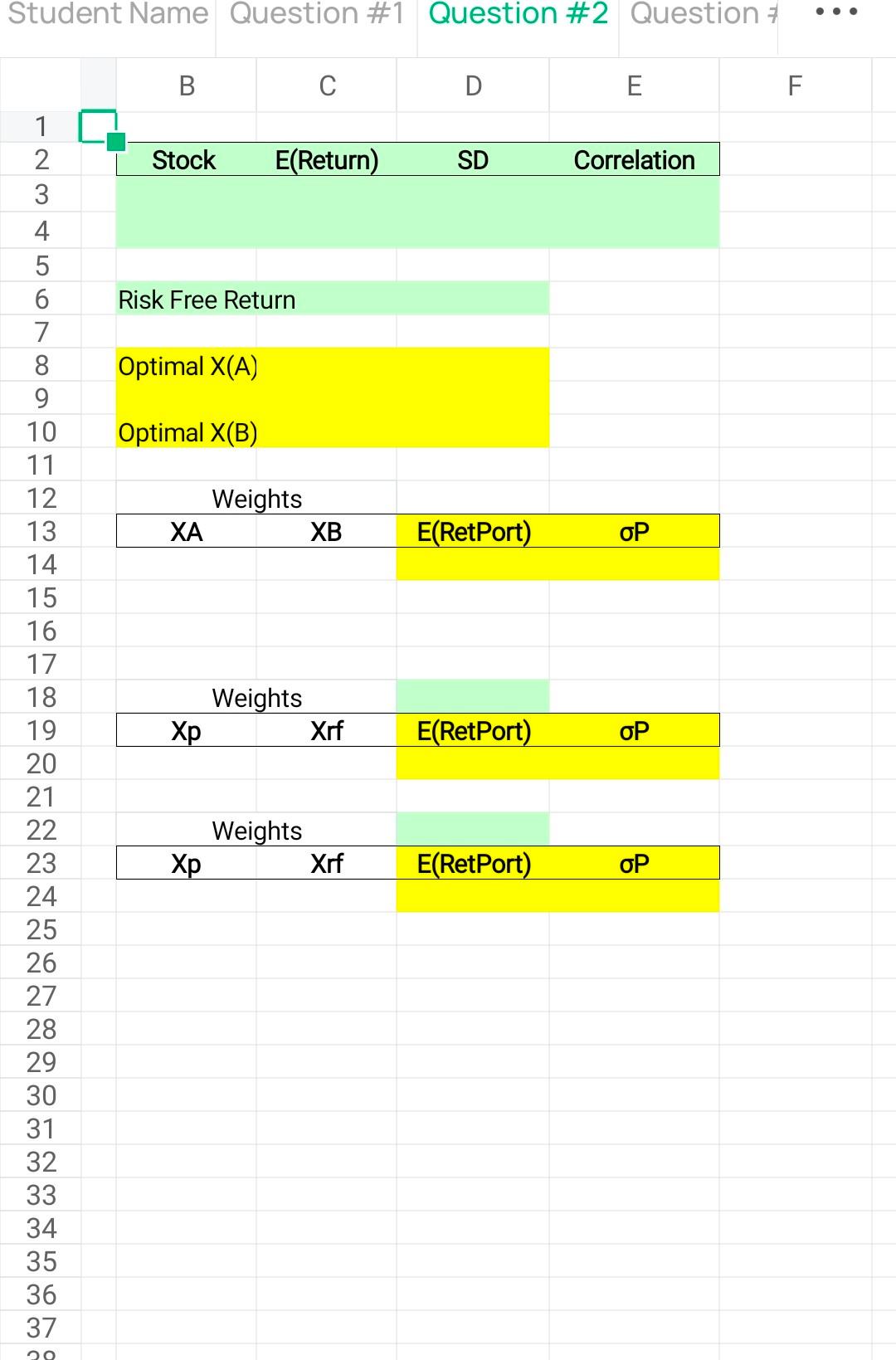

Question #2 (20 points total) You are evaluating two risky stocks, A and B, with expected returns of 7.0% and 16.0%, respectively. Stock A has a standard deviation of 25.0%; Stock B has a standard deviation of 40.0%. The correlation between the two stocks is 0.25. a.) Assume there is a risk-free rate of 1.50%. Solve for the portfolio weights of A and B in the optimal risky portfolio. What is the expected return and standard deviation of this portfolio? Student Name Question #1 Question #2 Question B D E F Stock E(Return) SD Correlation Risk Free Return Optimal X(A) Optimal X(B) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Weights XA XB E(RetPort) OP Weights Xrf E(RetPort) OP 22 Weights Xp Xrf E(RetPort) OP 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 DOStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance A Contemporary Application Of Theory To Policy

Authors: David N. Hyman

5th Edition

0030113172, 978-0030113178