Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please do not answer unless the answer can be completed correctly and easily understood. I have to repost many questions because it doesn't get answered

please do not answer unless the answer can be completed correctly and easily understood. I have to repost many questions because it doesn't get answered completely and it uses up my 20 questions.

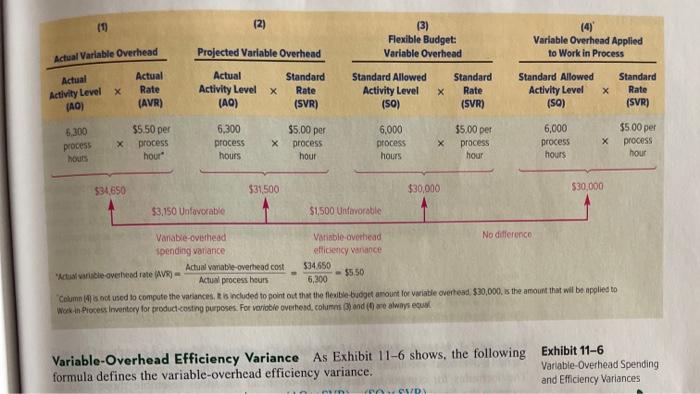

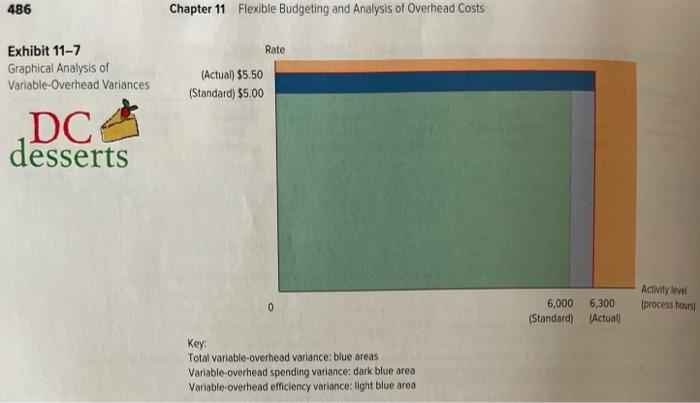

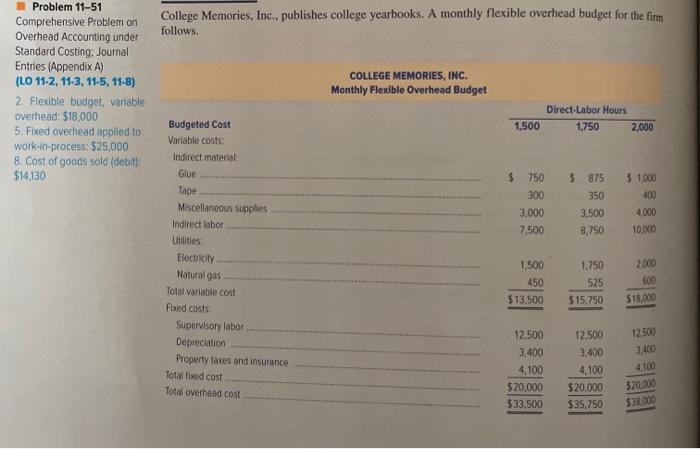

College Memories, Inc. publishes college yearbooks. A monthly flexible overhead budget for the firm follows. Problem 11-51 Comprehensive Problem on Overhead Accounting under Standard Costing, Journal Entries (Appendix A) (LO 11-2, 11-3, 11-5, 11-8) 2. Flexible budget, variable overhead: $18,000 5. Fixed overhead applied to work-in-process: $25,000 8. Cost of goods sold (debit) $14,130 COLLEGE MEMORIES, INC. Monthly Flexible Overhead Budget Direct-Labor Hours 1,500 1,750 2.000 $1,000 Budgeted Cost Variable costs: Indirect material Glue Tape Miscellaneous supplies Indirect labor... Utilities: Electricity... $ 750 300 3,000 7,500 $ 875 350 3,500 8.750 4.000 10,000 1,500 2.000 Natural gas 450 1,750 525 $15.750 600 $18.000 $13,500 Total variable cost Fixed costs Supervisory labor Depreciation Property taxes and insurance Totalfixed cost Total overhead cost 12,500 3,400 4.100 $20,000 $33,500 12,500 3.400 4,100 $20,000 $35,750 12.500 3,400 4.109 $20,000 $38.000 February, College Memories, Inc., produced 8,000 yearbooks and actually used 2,100 direct-labor 25 hour per book and overhead is budgeted and applied on the basis of direct-labor hours. During hours. The actual overhead costs for the month were as follows: Uverhead Costs The planned monthly production is 6,400 yearbooks. The standard direct-labor allowance is Actual variable overhead Actual fixed overhead $19,530 37,600 Required: 1. Determine the formula-style flexible overhead budget for College Memories, Inc. 2. Prepare a display similar to Exhibit 11-6, which shows College Memories' variable-overhead vari- ances for February. Indicate whether each variance is favorable or unfavorable. 3. Draw a graph similar to Exhibit 11-7, which shows College Memories' variable-overhead vari- ances for February 4. Interpret each of the variances computed in requirement 2. 5. Prepare a display similar to Exhibit 11-8, which shows College Memories' fixed-overhead vari- ances for February 6. Draw a graph similar to Exhibit 11-9, which depicts the company's applied and budgeted fixed overhead for February. Show the firm's February volume variance on the graph. 7. Interpret each of the variances computed in requirement 5. 8. Prepare journal entries to record each of the following: Incurrence of February's actual overhead cost. Application of February's overhead cost to Work-in-Process Inventory. Close underapplied or overapplied overhead into Cost of Goods Sold. 9. Draw T-accounts for all of the accounts used in the journal entries of requirement 8. Then post the journal entries to the T-accounts. . 11 (2) (3) Flexible Budget: Variable Overhead (4) Variable Overhead Applied to Work in Process Actual Variable Overhead Actual Activity Level (10) Projected Variable Overhead Actual Standard Activity Level Rate (AO) (SVR) Actual Rate (AVR) X Standard Allowed Activity Level (50) X Standard Rate (SVR) Standard Allowed Activity Level (SO) Standard Rate (SVR) $5.50 per $5.00 per $500 per 6.300 process 6,300 process X X X 6,000 process hours process hour process hour $5.00 per process hour X 6,000 process hours process hour hours $34,690 $31.500 $30,000 $30,000 $3,150 Unfavorable $1500 Unfavorable Vanable-overhead Variable overhead No difference spending variance efficiency wavance Actual variable-overhead cost $34650 "Actual variable overhead rate (AVR) - - $550 Actual process hours 6,300 Column 14 oct used to compute the variances, it is included to point out that the flexible budget amount for variatie overhead $30,000, is the amount that will be applied to Work in Process Inventory for productcasting purposes. For variable overhead. columns 3 and (or always eu Variable-Overhead Efficiency Variance As Exhibit 11-6 shows, the following Exhibit 11-6 formula defines the variable-overhead efficiency variance. Variable-Overhead Spending and Efficiency Variances TUT AD 486 Chapter 11 Flexible Budgeting and Analysis of Overhead Costs Rate Exhibit 11-7 Graphical Analysis of Variable-Overhead Variances (Actual) $5.50 (Standard) $5.00 DC desserts Activity level (process hours 0 6,000 6,300 (Standard) Actual : : Total variable-overhead variance: blue areas Variable-overhead spending variance: dark blue area Variable overhead efficiency varionce: light blue area if you can only do 1-4 that is okay please number so I know. I provided Figure 11-6 and 11-7 as well so you know the format. Thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using QuickBooks Online For Accounting

Authors: Glenn Owen

3rd Edition

0357391691, 9780357391693