Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please do not copy and paste. Consider a financial world in which there are only two risky assets, A and B, and a risk-free asset

Please do not copy and paste.

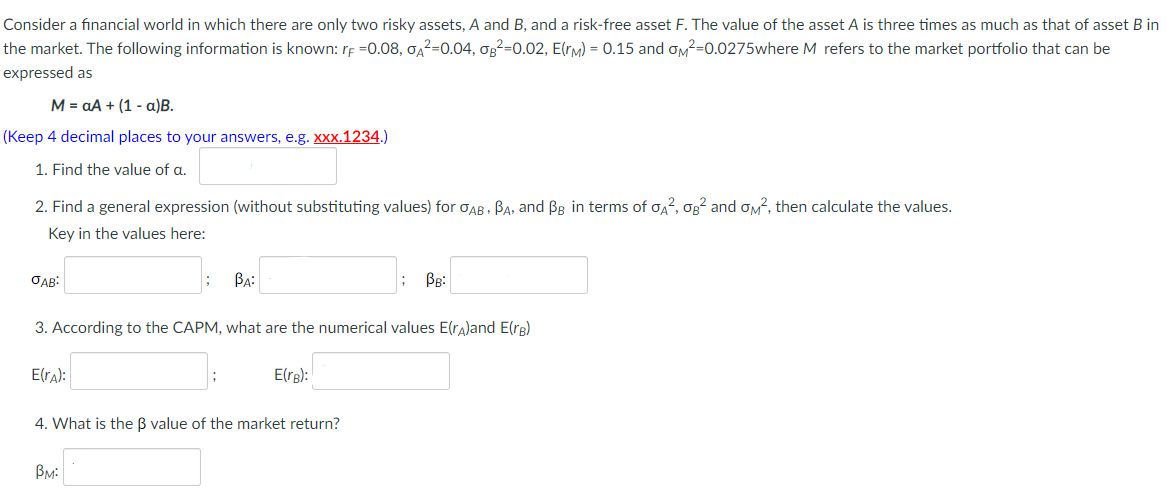

Consider a financial world in which there are only two risky assets, A and B, and a risk-free asset F. The value of the asset A is three times as much as that of asset B in the market. The following information is known: rF=0.08, A2=0.04, 082=0.02, E(rm) = 0.15 and Om2=0.0275where M refers to the market portfolio that can be expressed as M = A + (1 - a)B. (Keep 4 decimal places to your answers, e.g. xxx.1234.) 1. Find the value of a. 2. Find a general expression (without substituting values) for OAB, BA, and Be in terms of 0A, og and om?, then calculate the values. Key in the values here: : : BA: BB: 3. According to the CAPM, what are the numerical values E(ra)and E(rb) Elra): Elrs): 4. What is the B value of the market return? BM: Consider a financial world in which there are only two risky assets, A and B, and a risk-free asset F. The value of the asset A is three times as much as that of asset B in the market. The following information is known: rF=0.08, A2=0.04, 082=0.02, E(rm) = 0.15 and Om2=0.0275where M refers to the market portfolio that can be expressed as M = A + (1 - a)B. (Keep 4 decimal places to your answers, e.g. xxx.1234.) 1. Find the value of a. 2. Find a general expression (without substituting values) for OAB, BA, and Be in terms of 0A, og and om?, then calculate the values. Key in the values here: : : BA: BB: 3. According to the CAPM, what are the numerical values E(ra)and E(rb) Elra): Elrs): 4. What is the B value of the market return? BMStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Sustainability In Public Administration Exploring The Concept Of Financial Health

Authors: Manuel Pedro Rodríguez Bolívar

1st Edition

3319579614, 3319579622, 9783319579610, 9783319579627