please do part d e f

please do part d e f

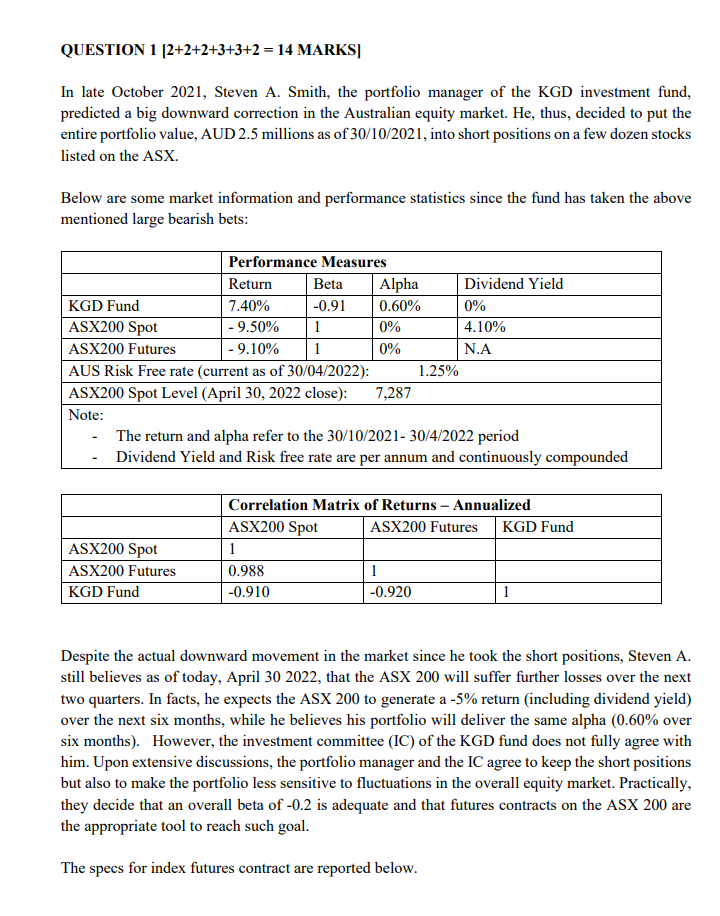

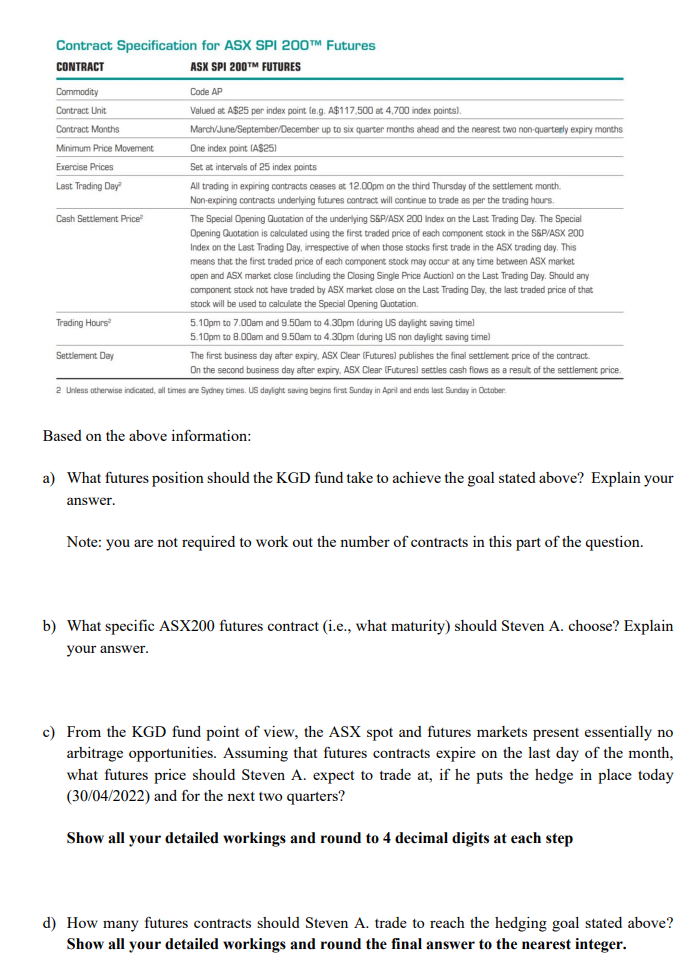

QUESTION 1 [2+2+2+3+3+2 = 14 MARKS] In late October 2021, Steven A. Smith, the portfolio manager of the KGD investment fund, predicted a big downward correction in the Australian equity market. He, thus, decided to put the entire portfolio value, AUD 2.5 millions as of 30/10/2021, into short positions on a few dozen stocks listed on the ASX. Below are some market information and performance statistics since the fund has taken the above mentioned large bearish bets: Performance Measures Return Beta Alpha Dividend Yield KGD Fund 7.40% -0.91 0.60% 0% ASX200 Spot - 9.50% 1 0% 4.10% ASX200 Futures - 9.10% 1 0% N.A AUS Risk Free rate (current as of 30/04/2022): 1.25% ASX200 Spot Level (April 30, 2022 close): 7,287 Note: The return and alpha refer to the 30/10/2021-30/4/2022 period Dividend Yield and Risk free rate are per annum and continuously compounded Correlation Matrix of Returns - Annualized ASX200 Spot ASX200 Futures KGD Fund ASX200 Spot 1 ASX200 Futures 0.988 1 KGD Fund -0.910 -0.920 1 Despite the actual downward movement in the market since he took the short positions, Steven A. still believes as of today, April 30 2022, that the ASX 200 will suffer further losses over the next two quarters. In facts, he expects the ASX 200 to generate a -5% return (including dividend yield) over the next six months, while he believes his portfolio will deliver the same alpha (0.60% over six months). However, the investment committee (IC) of the KGD fund does not fully agree with him. Upon extensive discussions, the portfolio manager and the IC agree to keep the short positions but also to make the portfolio less sensitive to fluctuations in the overall equity market. Practically, they decide that an overall beta of -0.2 is adequate and that futures contracts on the ASX 200 are the appropriate tool to reach such goal. The specs for index futures contract are reported below. Contract Specification for ASX SPI 200 Futures CONTRACT ASX SPI 200TM FUTURES Commodity Code AP Contract Unit Valued at A$25 per index point (e.g. A$117,500 at 4,700 index points). Contract Months March/June/September/December up to six quarter months ahead and the nearest two non-quarterly expiry months Minimum Price Movement One index point (A$25) Exercise Prices Set at intervals of 25 index points Last Trading Day All trading in expiring contracts ceases at 12.00pm on the third Thursday of the settlement month. Non-expiring contracts underlying futures contract will continue to trade as per the trading hours. Cash Settlement Price The Special Opening Quotation of the underlying S&P/ASX 200 Index on the Last Trading Day. The Special Opening Quotation is calculated using the first traded price of each component stock in the S&P/ASX 200 Index on the Last Trading Day, irrespective of when those stocks first trade in the ASX trading day. This means that the first traded price of each component stock may occur at any time between ASX market open and ASX market close (including the Closing Single Price Auction) on the Last Trading Day. Should any component stock not have traded by ASX market close on the Last Trading Day, the last traded price of that stock will be used to calculate the Special Opening Quotation. Trading Hours 5.10pm to 7.00am and 9.50am to 4.30pm (during US daylight saving timel 5.10pm to 8.00am and 9.50am to 4.30pm (during US non daylight saving time) Settlement Day The first business day after expiry, ASX Clear (Futures) publishes the final settlement price of the contract. On the second business day after expiry, ASX Clear (Futures) settles cash flows as a result of the settlement price. 2 Unless otherwise indicated, all times are Sydney times. US daylight saving begins first Sunday in April and ends last Sunday in October Based on the above information: a) What futures position should the KGD fund take to achieve the goal stated above? Explain your answer. Note: you are not required to work out the number of contracts in this part of the question. b) What specific ASX200 futures contract (i.e., what maturity) should Steven A. choose? Explain your answer. c) From the KGD fund point of view, the ASX spot and futures markets present essentially no arbitrage opportunities. Assuming that futures contracts expire on the last day of the month, what futures price should Steven A. expect to trade at, if he puts the hedge in place today (30/04/2022) and for the next two quarters? Show all your detailed workings and round to 4 decimal digits at each step d) How many futures contracts should Steven A. trade to reach the hedging goal stated above? Show all your detailed workings and round the final answer to the nearest integer. e) With the above hedging strategy in place, what risks (if any) will the KGD fund be exposed to until expiration of the futures position? Explain your answer. f) The IC asks Steven A. what return the hedged portfolio is expected to earn during the hedging period. Given the hedging strategy you suggest above and given all the information provided, what should Steve A. expect to earn on his overall (i.e., hedged) position during the hedging period? Show all your detailed workings. Note: you can assume that the riskfree rate over the upcoming six-months is half of the annualized rate reported above (i.e, 1.25%/2 = 0.625%) QUESTION 1 [2+2+2+3+3+2 = 14 MARKS] In late October 2021, Steven A. Smith, the portfolio manager of the KGD investment fund, predicted a big downward correction in the Australian equity market. He, thus, decided to put the entire portfolio value, AUD 2.5 millions as of 30/10/2021, into short positions on a few dozen stocks listed on the ASX. Below are some market information and performance statistics since the fund has taken the above mentioned large bearish bets: Performance Measures Return Beta Alpha Dividend Yield KGD Fund 7.40% -0.91 0.60% 0% ASX200 Spot - 9.50% 1 0% 4.10% ASX200 Futures - 9.10% 1 0% N.A AUS Risk Free rate (current as of 30/04/2022): 1.25% ASX200 Spot Level (April 30, 2022 close): 7,287 Note: The return and alpha refer to the 30/10/2021-30/4/2022 period Dividend Yield and Risk free rate are per annum and continuously compounded Correlation Matrix of Returns - Annualized ASX200 Spot ASX200 Futures KGD Fund ASX200 Spot 1 ASX200 Futures 0.988 1 KGD Fund -0.910 -0.920 1 Despite the actual downward movement in the market since he took the short positions, Steven A. still believes as of today, April 30 2022, that the ASX 200 will suffer further losses over the next two quarters. In facts, he expects the ASX 200 to generate a -5% return (including dividend yield) over the next six months, while he believes his portfolio will deliver the same alpha (0.60% over six months). However, the investment committee (IC) of the KGD fund does not fully agree with him. Upon extensive discussions, the portfolio manager and the IC agree to keep the short positions but also to make the portfolio less sensitive to fluctuations in the overall equity market. Practically, they decide that an overall beta of -0.2 is adequate and that futures contracts on the ASX 200 are the appropriate tool to reach such goal. The specs for index futures contract are reported below. Contract Specification for ASX SPI 200 Futures CONTRACT ASX SPI 200TM FUTURES Commodity Code AP Contract Unit Valued at A$25 per index point (e.g. A$117,500 at 4,700 index points). Contract Months March/June/September/December up to six quarter months ahead and the nearest two non-quarterly expiry months Minimum Price Movement One index point (A$25) Exercise Prices Set at intervals of 25 index points Last Trading Day All trading in expiring contracts ceases at 12.00pm on the third Thursday of the settlement month. Non-expiring contracts underlying futures contract will continue to trade as per the trading hours. Cash Settlement Price The Special Opening Quotation of the underlying S&P/ASX 200 Index on the Last Trading Day. The Special Opening Quotation is calculated using the first traded price of each component stock in the S&P/ASX 200 Index on the Last Trading Day, irrespective of when those stocks first trade in the ASX trading day. This means that the first traded price of each component stock may occur at any time between ASX market open and ASX market close (including the Closing Single Price Auction) on the Last Trading Day. Should any component stock not have traded by ASX market close on the Last Trading Day, the last traded price of that stock will be used to calculate the Special Opening Quotation. Trading Hours 5.10pm to 7.00am and 9.50am to 4.30pm (during US daylight saving timel 5.10pm to 8.00am and 9.50am to 4.30pm (during US non daylight saving time) Settlement Day The first business day after expiry, ASX Clear (Futures) publishes the final settlement price of the contract. On the second business day after expiry, ASX Clear (Futures) settles cash flows as a result of the settlement price. 2 Unless otherwise indicated, all times are Sydney times. US daylight saving begins first Sunday in April and ends last Sunday in October Based on the above information: a) What futures position should the KGD fund take to achieve the goal stated above? Explain your answer. Note: you are not required to work out the number of contracts in this part of the question. b) What specific ASX200 futures contract (i.e., what maturity) should Steven A. choose? Explain your answer. c) From the KGD fund point of view, the ASX spot and futures markets present essentially no arbitrage opportunities. Assuming that futures contracts expire on the last day of the month, what futures price should Steven A. expect to trade at, if he puts the hedge in place today (30/04/2022) and for the next two quarters? Show all your detailed workings and round to 4 decimal digits at each step d) How many futures contracts should Steven A. trade to reach the hedging goal stated above? Show all your detailed workings and round the final answer to the nearest integer. e) With the above hedging strategy in place, what risks (if any) will the KGD fund be exposed to until expiration of the futures position? Explain your answer. f) The IC asks Steven A. what return the hedged portfolio is expected to earn during the hedging period. Given the hedging strategy you suggest above and given all the information provided, what should Steve A. expect to earn on his overall (i.e., hedged) position during the hedging period? Show all your detailed workings. Note: you can assume that the riskfree rate over the upcoming six-months is half of the annualized rate reported above (i.e, 1.25%/2 = 0.625%)