Answered step by step

Verified Expert Solution

Question

1 Approved Answer

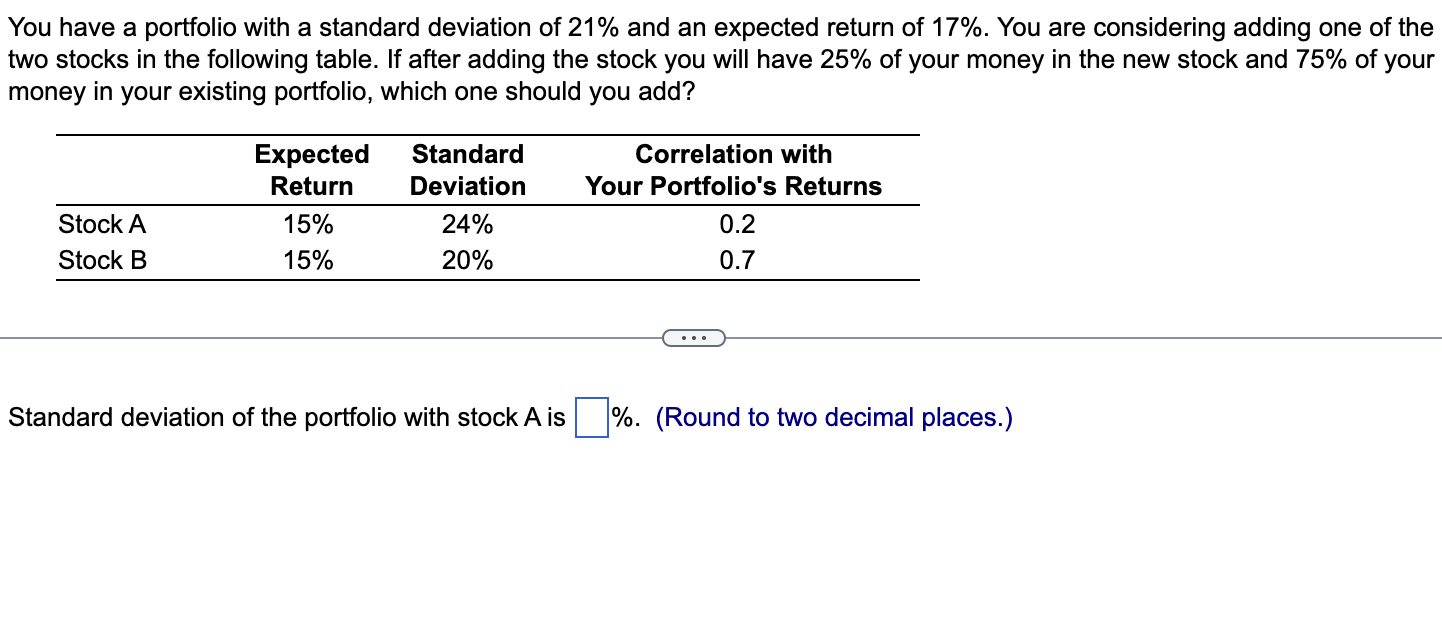

Please do parts A and Part B, I put an example in for reference You have a portfolio with a standard deviation of 21% and

Please do parts A and Part B, I put an example in for reference

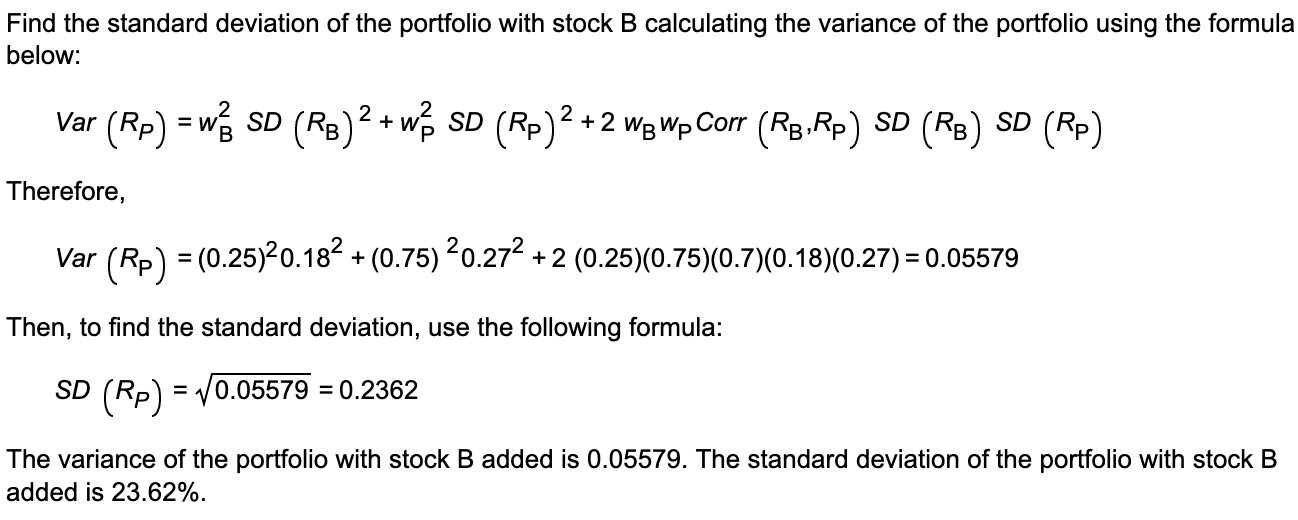

You have a portfolio with a standard deviation of 21% and an expected return of 17%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add? Standard deviation of the portfolio with stock A is \%. (Round to two decimal places.) Find the standard deviation of the portfolio with stock B calculating the variance of the portfolio using the formula below: Var(RP)=wB2SD(RB)2+wP2SD(RP)2+2wBwPCorr(RB,RP)SD(RB)SD(RP) Therefore, Var(RP)=(0.25)20.182+(0.75)20.272+2(0.25)(0.75)(0.7)(0.18)(0.27)=0.05579 Then, to find the standard deviation, use the following formula: SD(RP)=0.05579=0.2362 The variance of the portfolio with stock B added is 0.05579. The standard deviation of the portfolio with stock B added is 23.62%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Urban Public Finance

Authors: D. Wildasin

1st Edition

0415851882, 978-0415851886