Please do the blank following sheet

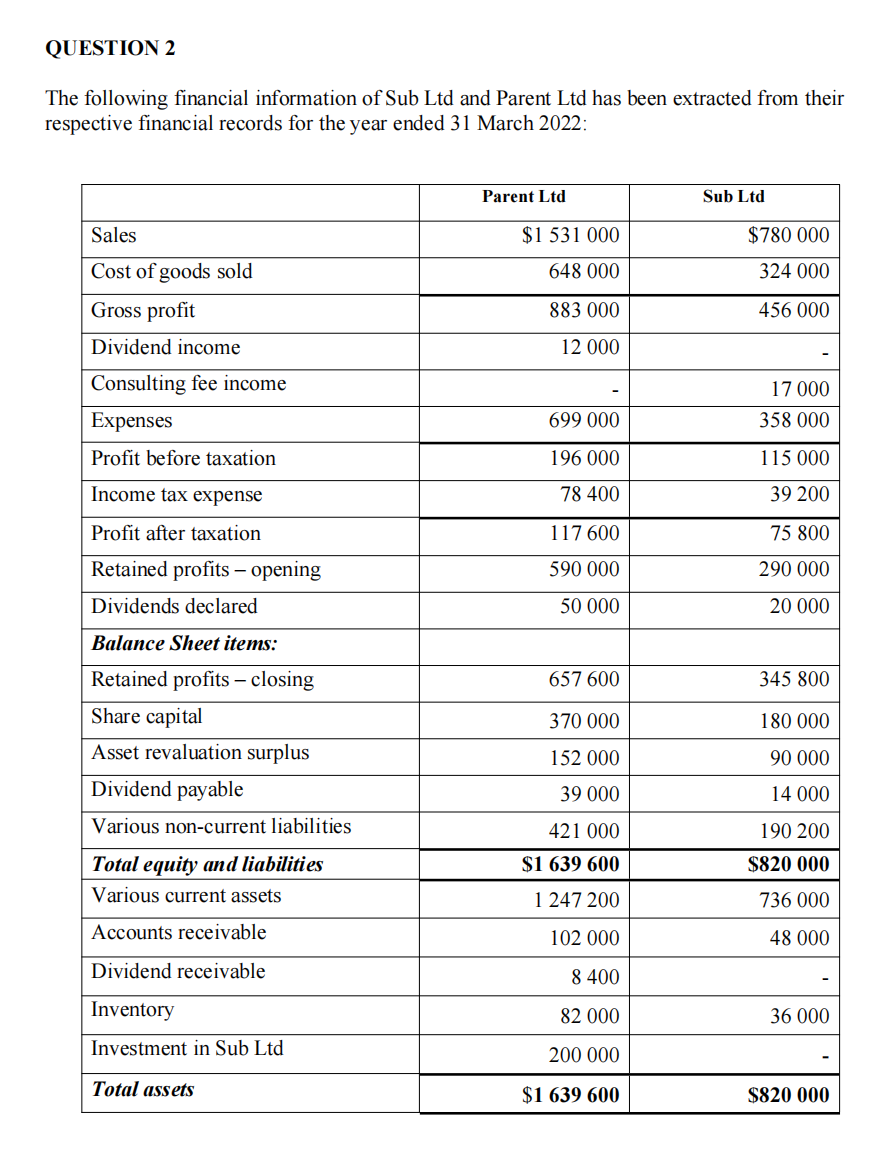

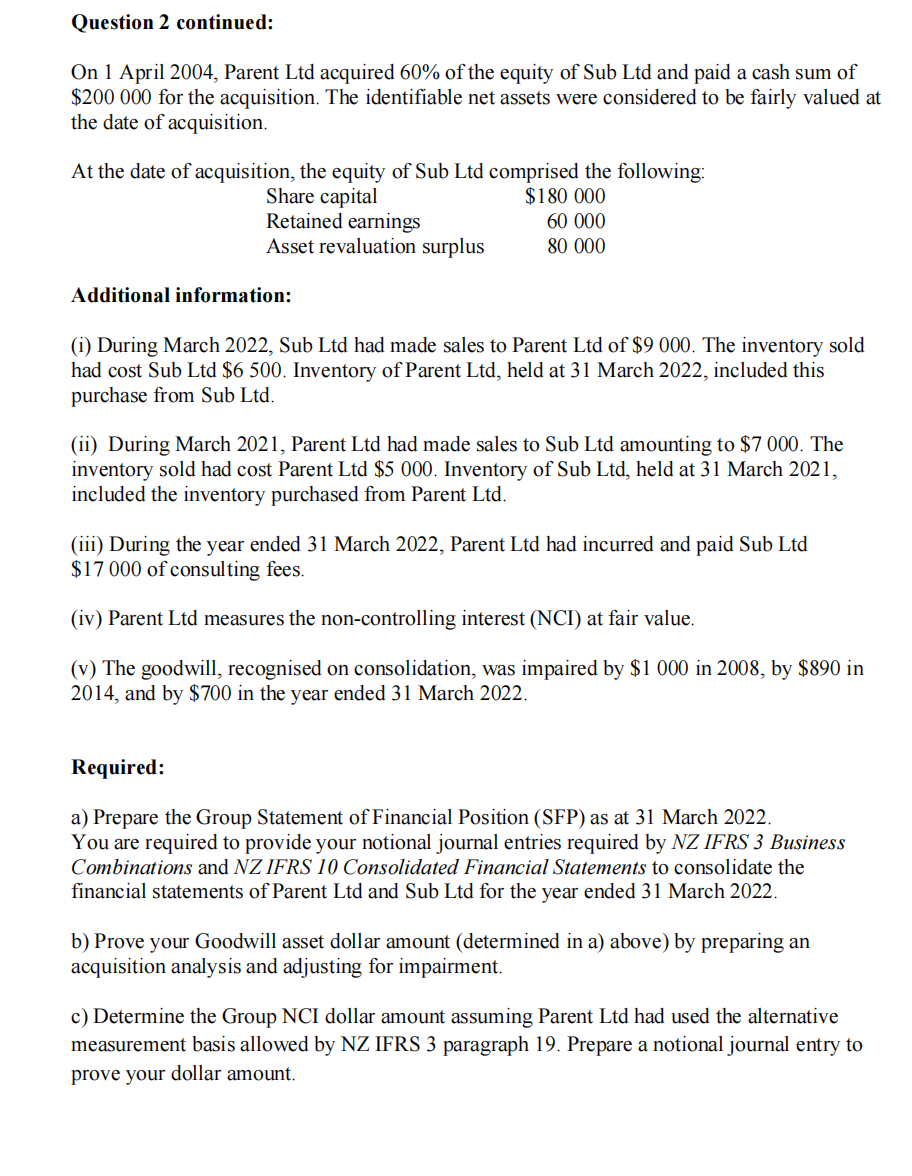

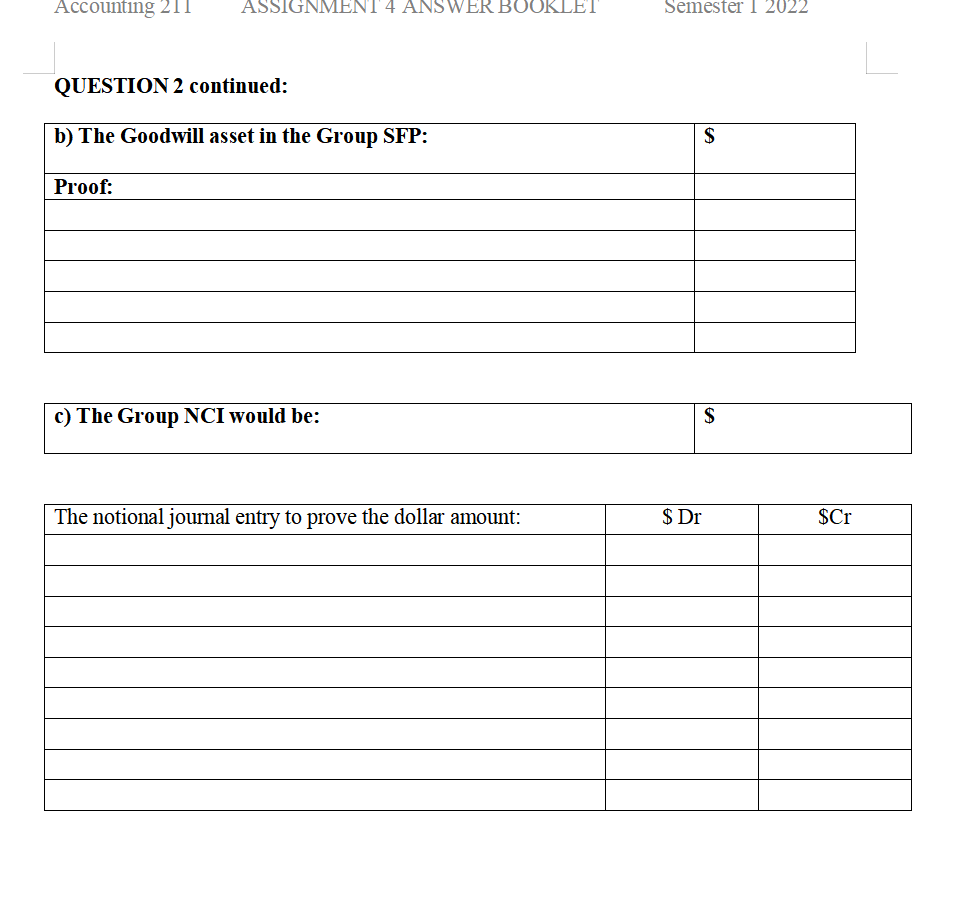

QUESTION 2 The following financial information of Sub Ltd and Parent Ltd has been extracted from their respective financial records for the year ended 31 March 2022: Parent Ltd Sub Ltd Sales $780 000 324 000 Cost of goods sold Gross profit 456 000 Dividend income Consulting fee income 17 000 Expenses 358 000 Profit before taxation 115 000 Income tax expense 39 200 Profit after taxation 75 800 Retained profits - opening 290 000 Dividends declared 20 000 Balance Sheet items: Retained profits - closing 345 800 Share capital 180 000 Asset revaluation surplus 90 000 Dividend payable 14 000 Various non-current liabilities 190 200 Total equity and liabilities $820 000 Various current assets 736 000 Accounts receivable 48 000 Dividend receivable Inventory 36 000 Investment in Sub Ltd Total assets $820 000 $1 531 000 648 000 883 000 12 000 699 000 196 000 78 400 117 600 590 000 50 000 657 600 370 000 152 000 39 000 421 000 $1 639 600 1 247 200 102 000 8 400 82 000 200 000 $1 639 600 Question 2 continued: On 1 April 2004, Parent Ltd acquired 60% of the equity of Sub Ltd and paid a cash sum of $200 000 for the acquisition. The identifiable net assets were considered to be fairly valued at the date of acquisition. At the date of acquisition, the equity of Sub Ltd comprised the following: Share capital $180 000 Retained earnings 60 000 80 000 Asset revaluation surplus Additional information: (i) During March 2022, Sub Ltd had made sales to Parent Ltd of $9 000. The inventory sold had cost Sub Ltd $6 500. Inventory of Parent Ltd, held at 31 March 2022, included this purchase from Sub Ltd. (ii) During March 2021, Parent Ltd had made sales to Sub Ltd amounting to $7 000. The inventory sold had cost Parent Ltd $5 000. Inventory of Sub Ltd, held at 31 March 2021, included the inventory purchased from Parent Ltd. (iii) During the year ended 31 March 2022, Parent Ltd had incurred and paid Sub Ltd $17 000 of consulting fees. (iv) Parent Ltd measures the non-controlling interest (NCI) at fair value. (v) The goodwill, recognised on consolidation, was impaired by $1 000 in 2008, by $890 in 2014, and by $700 in the year ended 31 March 2022. Required: a) Prepare the Group Statement of Financial Position (SFP) as at 31 March 2022. You are required to provide your notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements to consolidate the financial statements of Parent Ltd and Sub Ltd for the year ended 31 March 2022. b) Prove your Goodwill asset dollar amount (determined in a) above) by preparing an acquisition analysis and adjusting for impairment. c) Determine the Group NCI dollar amount assuming Parent Ltd had used the alternative measurement basis allowed by NZ IFRS 3 paragraph 19. Prepare a notional journal entry to prove your dollar amount. Accounting 211 QUESTION 2 continued: b) The Goodwill asset in the Group SFP: Proof: c) The Group NCI would be: The notional journal entry to prove the dollar amount: ASSIGNMENT 4 ANSWER BOOKLET Semester I 2022 $ $ $ Dr $Cr