Answered step by step

Verified Expert Solution

Question

1 Approved Answer

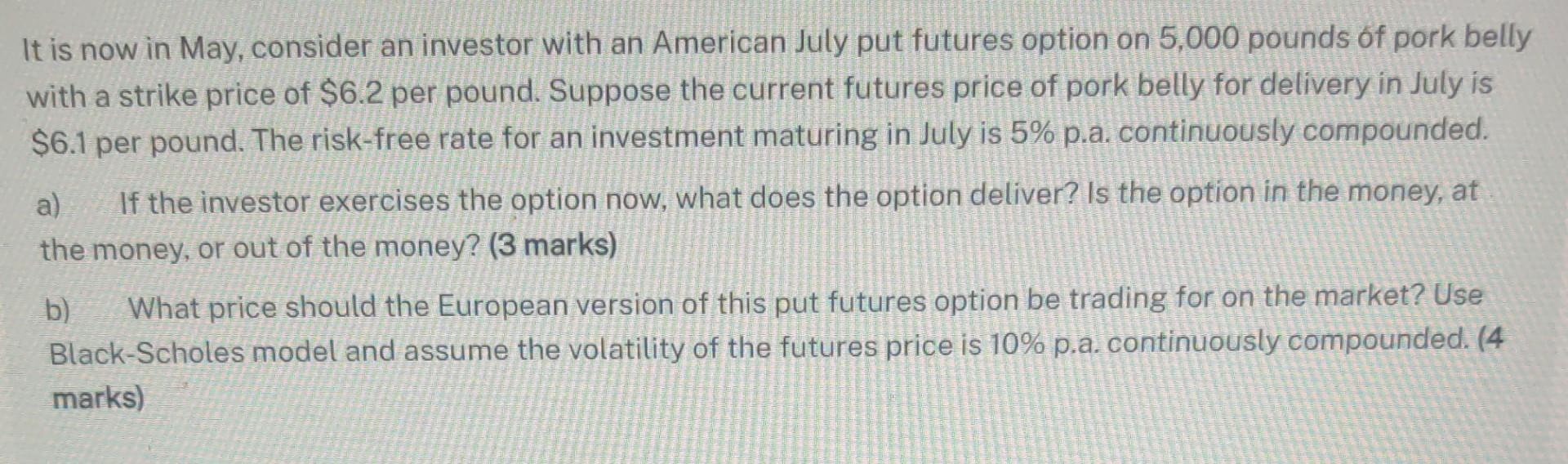

please ensure neat handwriting. Solution needed urgently It is now in May, consider an investor with an American July put futures option on 5,000 pounds

please ensure neat handwriting. Solution needed urgently

It is now in May, consider an investor with an American July put futures option on 5,000 pounds of pork belly with a strike price of $6.2 per pound. Suppose the current futures price of pork belly for delivery in July is $6.1 per pound. The risk-free rate for an investment maturing in July is 5% p.a. continuously compounded. a) If the investor exercises the option now, what does the option deliver? Is the option in the money, at the money, or out of the money? (3 marks) b) What price should the European version of this put futures option be trading for on the market? Use Black-Scholes model and assume the volatility of the futures price is 10% p.a. continuously compounded. (4 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of The Political Economy Of Financial Crises

Authors: Martin H. Wolfson, Gerald A. Epstein

1st Edition

0199757232, 978-0199757237