Answered step by step

Verified Expert Solution

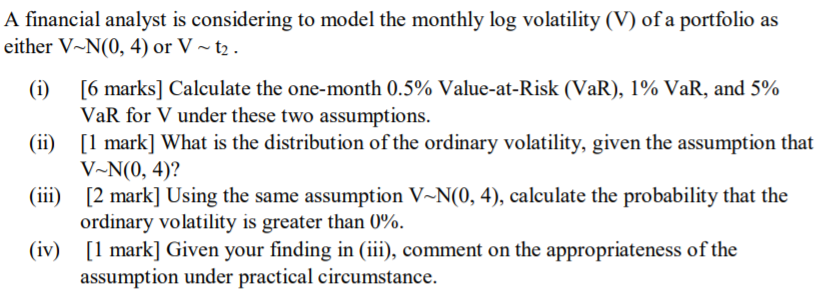

Question

1 Approved Answer

Please explain and show working A financial analyst is considering to model the monthly log volatility (V) of a portfolio as either V-N(0, 4) or

Please explain and show working

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Finance Markets Investments and Financial Management

Authors: Melicher Ronald, Norton Edgar

15th edition

9781118800720, 1118492676, 1118800729, 978-1118492673