Please explain each step.

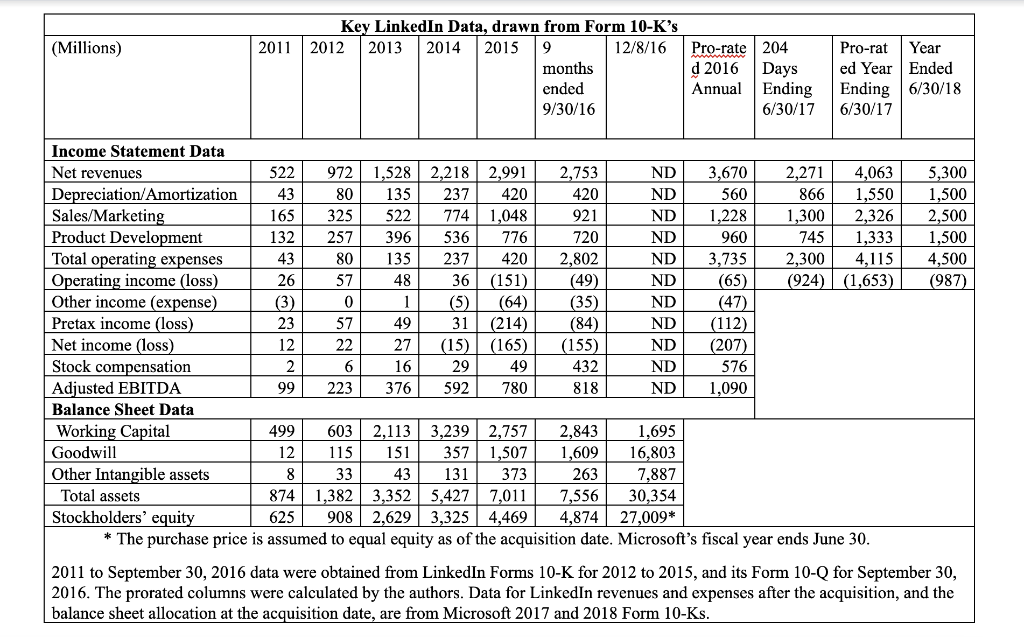

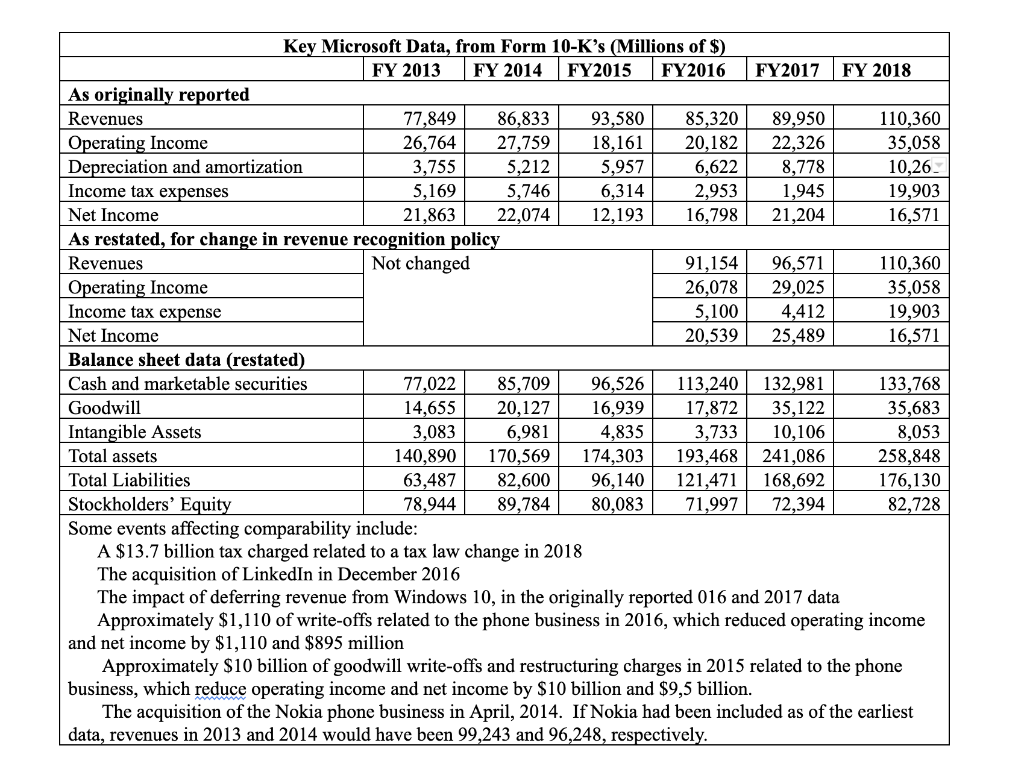

One objective of financial accounting is providing relevant information about the operating success or failure of companies. In this case, the measurement of LinkedIn's expenses was very different before and after it was acquired by Microsoft, due principally to differences in the amount of amortization of intangible assets.

- Discuss whether you believe the measurement of income was better before, or after, the acquisition date? Explain your answer.

- LinkedIn chose to disclose an alternative measure of its operations, "Adjusted EBITDA." This measure ignores depreciation, amortization, interest, income taxes, and stock compensation expense.

- Would this measure have been affected the same way as net income by the acquisition accounting done by Microsoft?

- Do you feel that ignoring amortization provides better information for investors than including amortization? Explain your answer.

(Millions) 2011 Key LinkedIn Data, drawn from Form 10-K's 2012 2013 2014 2015 9 12/8/16 months ended 9/30/16 Pro-rate 204 d 2016 Days Annual Ending 6/30/17 Pro-rat Year ed Year Ended Ending 6/30/18 6/30/17 E 1,228 Income Statement Data Net revenues 522 972 1,528 2,218 2,991 2,753 ND 3,670 2.271 4,063 5,300 Depreciation/Amortization 43 80 135 237 420 420 ND 560 866 1,550 1,500 Sales/Marketing 165 325 522 774 1,048 921 ND 1,300 2,326 2,500 Product Development 132 257 396 536 776 720 ND 960 745 1,333 1,500 Total operating expenses 43 80 135 237 420 2,802 ND 3,735 2,300 4,115 4,500 Operating income (loss) 26 57 48 36 (151) (49) ND (65) (924) (1,653) (987) Other income (expense) (3) 0 1 (5) (64) (35) ND (47) Pretax income (loss) 23 57 49 31 (214) (84) ND (112) Net income (loss) 12 22 27 (15) (165) (155) ND (207) Stock compensation 2 6 16 29 49 432 ND 576 Adjusted EBITDA 99 223 376 592 780 818 ND 1,090 Balance Sheet Data Working Capital 499 603 2,113 3,239 2,843 1,695 Goodwill 12 115 151 357 1,507 1,609 16,803 Other Intangible assets 8 33 43 131 373 263 7,887 Total assets 874 1,382 3,352 5,427 7,011 7,556 30,354 Stockholders' equity 908 2,629 3,325 4,469 4,874 27,009* * The purchase price is assumed to equal equity as of the acquisition date. Microsoft's fiscal year ends June 30. 2011 to September 30, 2016 data were obtained from LinkedIn Forms 10-K for 2012 to 2015, and its Form 10-Q for September 30, 2016. The prorated columns were calculated by the authors. Data for LinkedIn revenues and expenses after the acquisition, and the balance sheet allocation at the acquisition date, are from Microsoft 2017 and 2018 Form 10-Ks. 2,757 625 Key Microsoft Data, from Form 10-K's (Millions of $) FY 2013 FY 2014 FY2015 FY2016 FY2017 FY 2018 As originally reported Revenues 77,849 86,833 93,580 85,320 89,950 110,360 Operating Income 26,764 27,759 18,161 20,182 22,326 35,058 Depreciation and amortization 3,755 5,212 5,957 6,622 8,778 10,26 Income tax expenses 5,169 5,746 6,314 2,953 1,945 19,903 Net Income 21,863 22,074 12,193 16,798 21,204 16,571 As restated, for change in revenue recognition policy Revenues Not changed 91,154 96,571 110,360 Operating Income 26,078 29,025 35,058 Income tax expense 5,100 4,412 19,903 Net Income 20,539 25,489 16,571 Balance sheet data (restated) Cash and marketable securities 77,022 85,709 96,526 113,240 132,981 133,768 Goodwill 14,655 20,127 16,939 17,872 35,122 35,683 Intangible Assets 3,083 6,981 4,835 3,733 10,106 8,053 Total assets 140,890 170,569 174,303 193,468 241,086 258,848 Total Liabilities 63,487 82,600 96,140 121,471 168,692 176,130 Stockholders' Equity 78,944 89,784 80,083 71,997 72,394 82,728 Some events affecting comparability include: A $13.7 billion tax charged related to a tax law change in 2018 The acquisition of LinkedIn in December 2016 The impact of deferring revenue from Windows 10, in the originally reported 016 and 2017 data Approximately $1,110 of write-offs related to the phone business in 2016, which reduced operating income and net income by $1,110 and $895 million Approximately $10 billion of goodwill write-offs and restructuring charges in 2015 related to the phone business, which reduce operating income and net income by $10 billion and $9,5 billion. The acquisition of the Nokia phone business in April, 2014. If Nokia had been included as of the earliest data, revenues in 2013 and 2014 would have been 99,243 and 96,248, respectively