Answered step by step

Verified Expert Solution

Question

1 Approved Answer

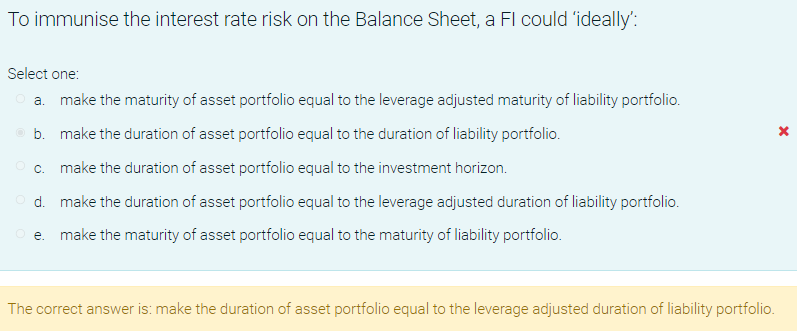

Please explain the correct answer and why B is incorrect. To immunise the interest rate risk on the Balance Sheet, a FI could ideally': X

Please explain the correct answer and why B is incorrect.

To immunise the interest rate risk on the Balance Sheet, a FI could ideally': X X Select one: a. make the maturity of asset portfolio equal to the leverage adjusted maturity of liability portfolio. b. make the duration of asset portfolio equal to the duration of liability portfolio. c. make the duration of asset portfolio equal to the investment horizon. d. make the duration of asset portfolio equal to the leverage adjusted duration of liability portfolio. e. make the maturity of asset portfolio equal to the maturity of liability portfolio. The correct answer is: make the duration of asset portfolio equal to the leverage adjusted duration of liability portfolioStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Moolah Or Bummer A Humorous Look At Finance And Investing

Authors: Sharon Schwab

1st Edition

0595344313, 9780595344314