Answered step by step

Verified Expert Solution

Question

1 Approved Answer

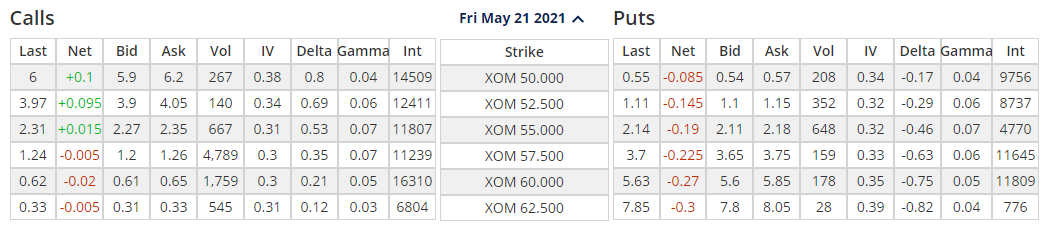

Please explain with full working out how the values were obtained Now take the current price of the Exxon (XOM) May ATM monthly expiry option.

Please explain with full working out how the values were obtained

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Basic Finance An Introduction to Financial Institutions Investments and Management

Authors: Herbert B. Mayo

10th edition

1111820635, 978-1111820633