Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please explain your answer not just results 0 Again, assume that there are two investors, one being rational and the other one being overconfident. Both

Please explain your answer not just results

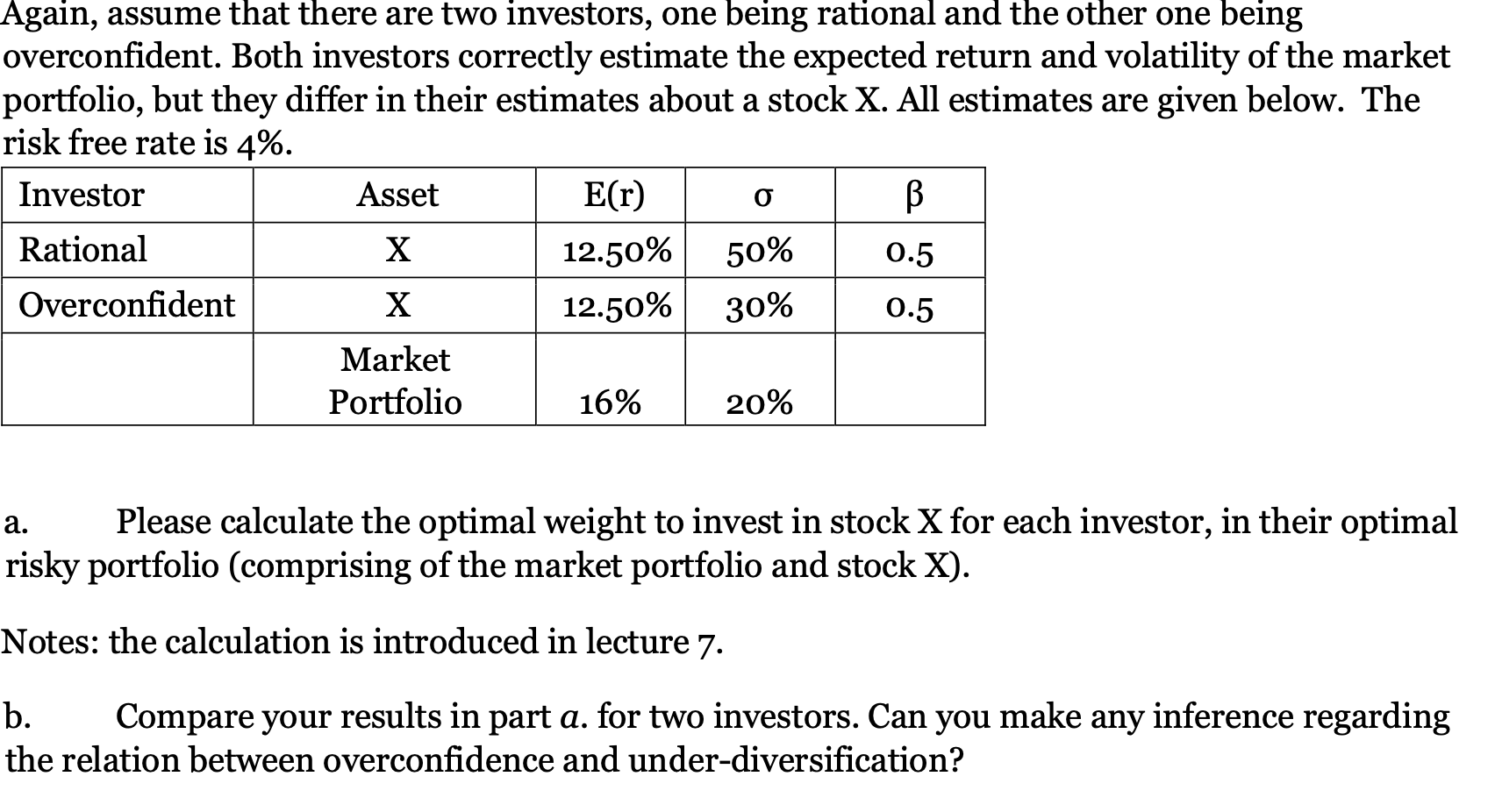

0 Again, assume that there are two investors, one being rational and the other one being overconfident. Both investors correctly estimate the expected return and volatility of the market portfolio, but they differ in their estimates about a stock X. All estimates are given below. The risk free rate is 4%. Investor Asset E(r) B Rational X 12.50% Overconfident X 12.50% 30% 0.5 Market Portfolio 16% 20% 50% 0.5 a. Please calculate the optimal weight to invest in stock X for each investor, in their optimal risky portfolio (comprising of the market portfolio and stock X). Notes: the calculation is introduced in lecture 7. b. Compare your results in part a. for two investors. Can you make any inference regarding the relation between overconfidence and under-diversification? 0 Again, assume that there are two investors, one being rational and the other one being overconfident. Both investors correctly estimate the expected return and volatility of the market portfolio, but they differ in their estimates about a stock X. All estimates are given below. The risk free rate is 4%. Investor Asset E(r) B Rational X 12.50% Overconfident X 12.50% 30% 0.5 Market Portfolio 16% 20% 50% 0.5 a. Please calculate the optimal weight to invest in stock X for each investor, in their optimal risky portfolio (comprising of the market portfolio and stock X). Notes: the calculation is introduced in lecture 7. b. Compare your results in part a. for two investors. Can you make any inference regarding the relation between overconfidence and under-diversificationStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started