Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please fill in all the blanks. Can Simone and Rajiv afford this home using the monthly income loan criterion? Next week, your friends Simone and

Please fill in all the blanks.

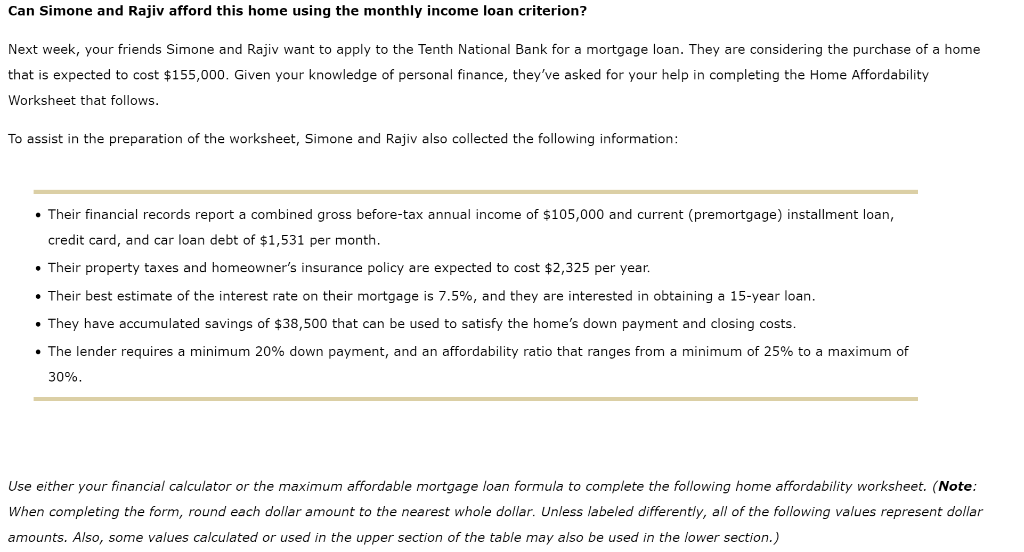

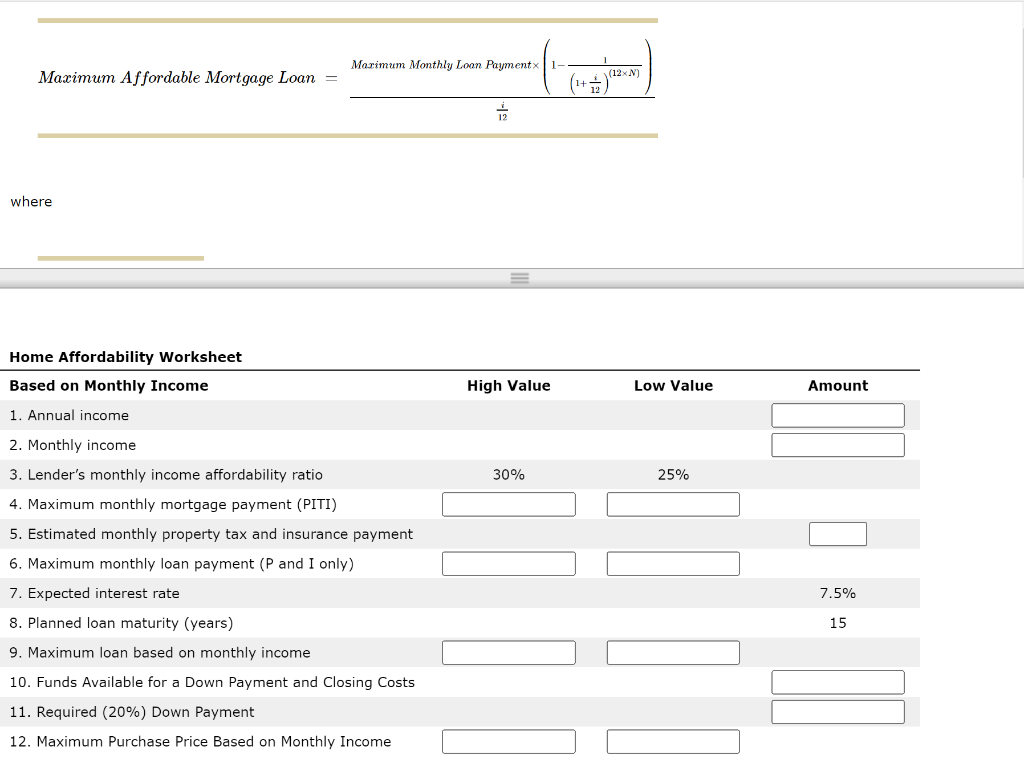

Can Simone and Rajiv afford this home using the monthly income loan criterion? Next week, your friends Simone and Rajiv want to apply to the Tenth National Bank for a mortgage loan. They are considering the purchase of a home that is expected to cost $155,000. Given your knowledge of personal finance, they've asked for your help in completing the Home Affordability Worksheet that follows. To assist in the preparation of the worksheet, Simone and Rajiv also collected the following information: Their financial records report a combined gross before-tax annual income of $105,000 and current (premortgage) installment loan, credit card, and car loan debt of $1,531 per month. Their property taxes and homeowner's insurance policy are expected to cost $2,325 per year. Their best estimate of the interest rate on their mortgage is 7.5%, and they are interested in obtaining a 15-year loan. They have accumulated savings of $38,500 that can be used to satisfy the home's down payment and closing costs. The lender requires a minimum 20% down payment, and an affordability ratio that ranges from a minimum of 25% to a maximum of 30%. Use either your financial calculator or the maximum affordable mortgage loan formula to complete the following home affordability worksheet. (Note: When completing the form, round each dollar amount to the nearest whole dollar. Unless labeled differently, all of the following values represent dollar amounts. Also, some values calculated or used in the upper section of the table may also be used in the lower section.) Marimum Monthly Loon Payment 1 - Maximum Affordable Mortgage Loan = (12) where Home Affordability Worksheet Based on Monthly Income High Value Low Value Amount 1. Annual income 30% 25% 2. Monthly income 3. Lender's monthly income affordability ratio 4. Maximum monthly mortgage payment (PITI) 5. Estimated monthly property tax and insurance payment 6. Maximum monthly loan payment (P and I only) 7. Expected interest rate 8. Planned loan maturity (years) 9. Maximum loan based on monthly income 10. Funds Available for a Down Payment and Closing Costs 7.5% 15 11. Required (20%) Down Payment 12. Maximum Purchase Price Based on Monthly IncomeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance In A Public World How Technology Social Media And Ads Affect Your Money Decisions

Authors: Bob DePasquale

1st Edition

1637306652, 978-1637306659