Answered step by step

Verified Expert Solution

Question

1 Approved Answer

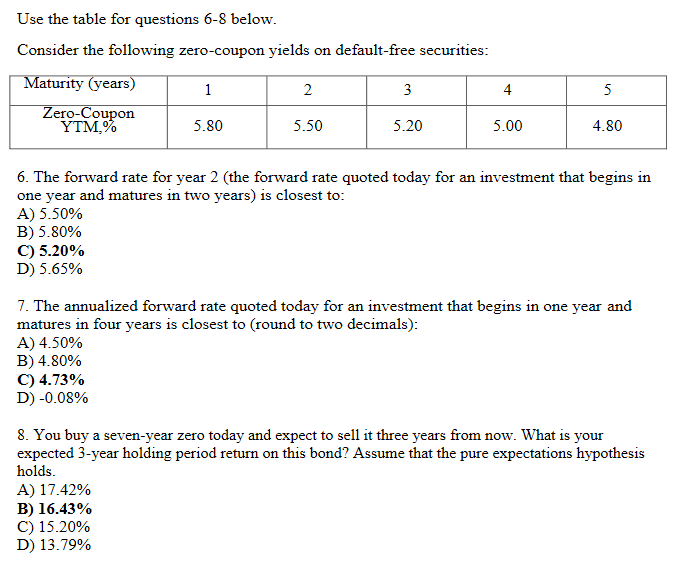

Please give a proper explanation. Thanks Use the table for questions 6-8 below. Consider the following zero-coupon yields on default-free securities: Maturity (years) 1 2

Please give a proper explanation. Thanks

Use the table for questions 6-8 below. Consider the following zero-coupon yields on default-free securities: Maturity (years) 1 2 3 4 Zero-Coupon YTM,% 5.80 5.50 5.20 5.00 5 4.80 6. The forward rate for year 2 (the forward rate quoted today for an investment that begins in one year and matures in two years) is closest to: A) 5.50% B) 5.80% C) 5.20% D) 5.65% 7. The annualized forward rate quoted today for an investment that begins in one year and matures in four years is closest to (round to two decimals): A) 4.50% B) 4.80% C) 4.73% D) -0.08% 8. You buy a seven-year zero today and expect to sell it three years from now. What is your expected 3-year holding period return on this bond? Assume that the pure expectations hypothesis holds. A) 17.42% B) 16.43% C) 15.20% D) 13.79%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introductory Econometrics For Finance

Authors: Chris Brooks

2nd Edition

052169468X, 9780521694681