Answered step by step

Verified Expert Solution

Question

1 Approved Answer

(Please give step-by-step instructions and show what formula can be used to calculate it) P&G India. Procter and Gamble's affiliate in India, P&G India, procures

(Please give step-by-step instructions and show what formula can be used to calculate it)

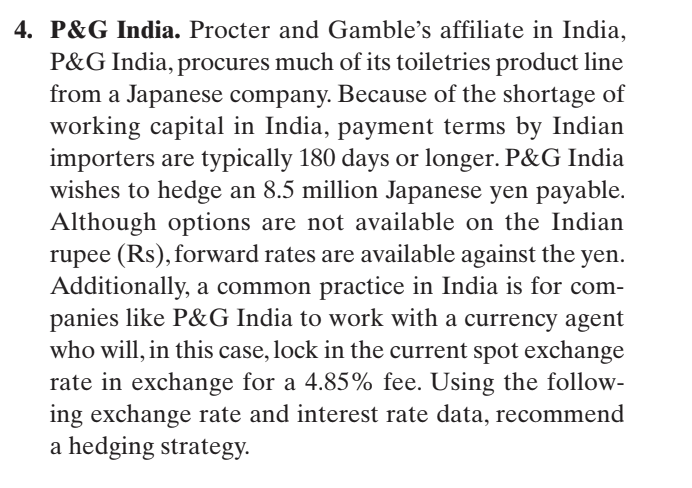

P\&G India. Procter and Gamble's affiliate in India, P&G India, procures much of its toiletries product line from a Japanese company. Because of the shortage of working capital in India, payment terms by Indian importers are typically 180 days or longer. P&G India wishes to hedge an 8.5 million Japanese yen payable. Although options are not available on the Indian rupee (Rs), forward rates are available against the yen. Additionally, a common practice in India is for companies like P&G India to work with a currency agent who will, in this case, lock in the current spot exchange rate in exchange for a 4.85% fee. Using the following exchange rate and interest rate data, recommend a hedging strategy. \begin{tabular}{lr} Spot rate: & 120.60/$ \\ 180-day forward rate & 2.400/Rps \\ Expected spot, 180 days & 2.6000 \\ 180-day Indian rupee investing rate & 8.000% \\ 180-day Japanese yen investing rate & 1.500% \\ Currency agents exchange rate & 4.850% \\ P\&G Indias cost of capital & 12.000% \end{tabular}Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Consumer Finance Research

Authors: Jing J. Xiao

1st Edition

1441926046, 978-1441926043