Please guide me on this question

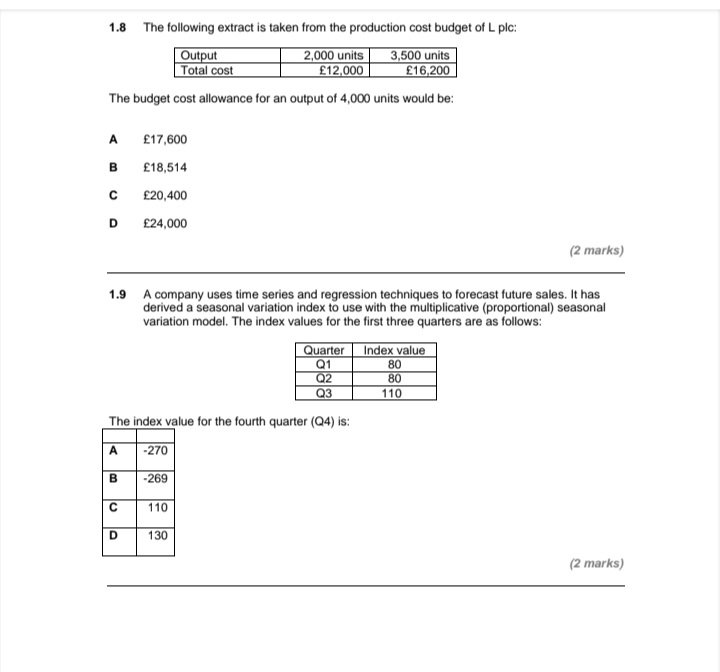

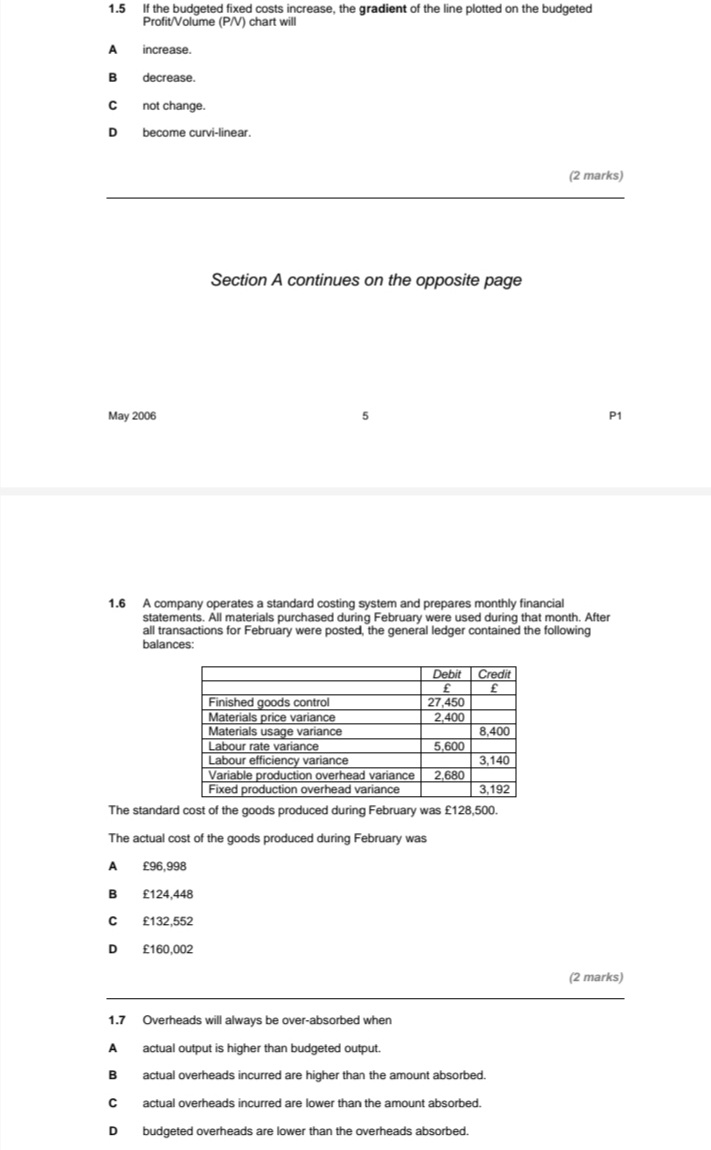

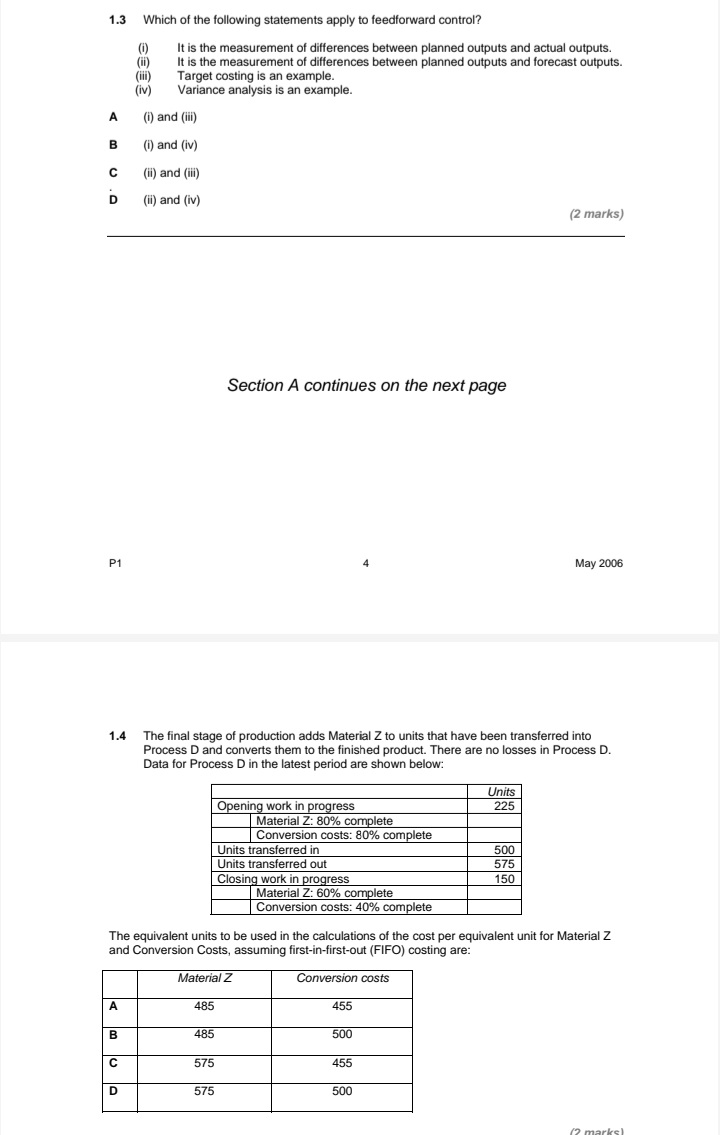

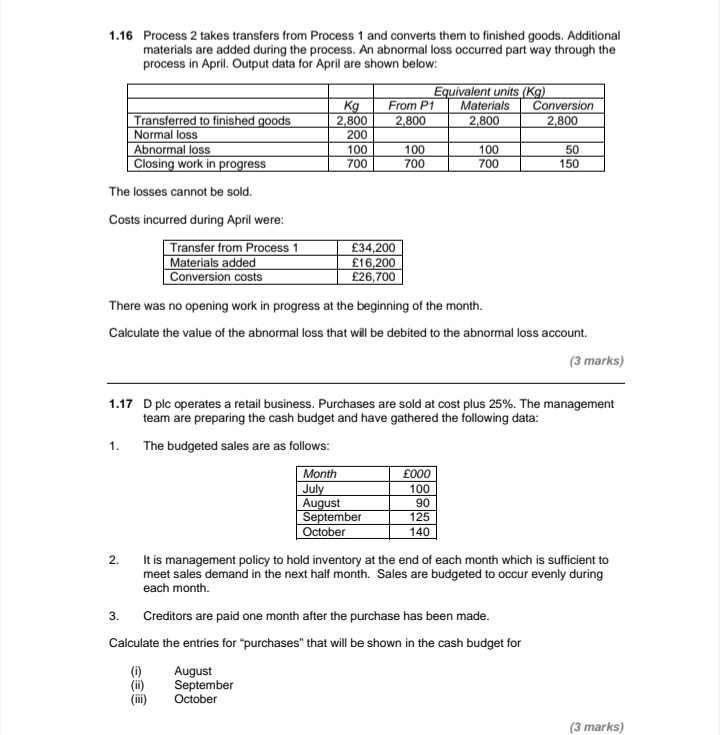

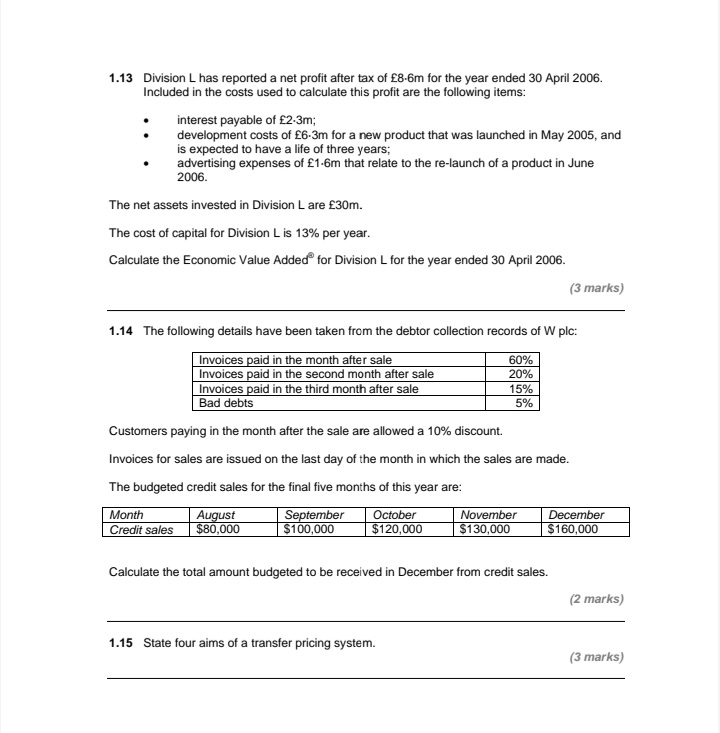

1.8 The following extract is taken from the production cost budget of L plc: Output 2,000 units 3,500 units Total cost E12,000 E16,200 The budget cost allowance for an output of 4,000 units would be: A E17,600 B E18,514 C E20,400 D E24,000 (2 marks) 1.9 A company uses time series and regression techniques to forecast future sales. It has derived a seasonal variation index to use with the multiplicative (proportional) seasonal variation model. The index values for the first three quarters are as follows: Quarter Index value Q1 80 Q2 80 Q3 110 The index value for the fourth quarter (Q4) is: A -270 B -269 C 110 130 (2 marks)1.5 If the budgeted fixed costs increase, the gradient of the line plotted on the budgeted Profit/Volume (P/V) chart will A increase. B decrease. C not change. D become curvi-linear. (2 marks) Section A continues on the opposite page May 2006 5 P1 1.6 A company operates a standard costing system and prepares monthly financial statements. All materials purchased during February were used during that month. After all transactions for February were posted, the general ledger contained the following balances: Debit Credit Finished goods control 27,450 Materials price variance 2,400 Materials usage variance 8,400 Labour rate variance 5.600 Labour efficiency variance 3,140 Variable production overhead variance | 2,680 Fixed production overhead variance 3,192 The standard cost of the goods produced during February was $128,500. The actual cost of the goods produced during February was A 196,998 B E124,448 C (132,552 D E160,002 (2 marks) 1.7 Overheads will always be over-absorbed when A actual output is higher than budgeted output. B actual overheads incurred are higher than the amount absorbed. C actual overheads incurred are lower than the amount absorbed. D budgeted overheads are lower than the overheads absorbed.1.3 Which of the following statements apply to feedforward control? It is the measurement of differences between planned outputs and actual outputs. It is the measurement of differences between planned outputs and forecast outputs. Target costing is an example. Variance analysis is an example. A (i) and (iii) B (1) and (iv) C (ii) and (iii) D (ii) and (iv) (2 marks) Section A continues on the next page P1 May 2006 1.4 The final stage of production adds Material Z to units that have been transferred into Process D and converts them to the finished product. There are no losses in Process D. Data for Process D in the latest period are shown below: Units Opening work in progress 225 Material Z: 80% complete Conversion costs: 80% complete Units transferred in 500 Units transferred out 575 Closing work in progress 150 Material Z: 60% complete Conversion costs: 40% complete The equivalent units to be used in the calculations of the cost per equivalent unit for Material Z and Conversion Costs, assuming first-in-first-out (FIFO) costing are: Material Z Conversion costs A 485 455 485 500 C 575 455 D 575 5001.16 Process 2 takes transfers from Process 1 and converts them to finished goods. Additional materials are added during the process. An abnormal loss occurred part way through the process in April. Output data for April are shown below: Equivalent units (Kg Kg From P1 Materials Conversion Transferred to finished goods 2,800 2,800 2,800 2,800 Normal loss 200 Abnormal loss 100 100 100 50 Closing work in progress 700 700 700 150 The losses cannot be sold. Costs incurred during April were: Transfer from Process 1 E34,200 Materials added E16,200 Conversion costs E26,700 There was no opening work in progress at the beginning of the month. Calculate the value of the abnormal loss that will be debited to the abnormal loss account. (3 marks) 1.17 D plc operates a retail business. Purchases are sold at cost plus 25%. The management team are preparing the cash budget and have gathered the following data: 1 . The budgeted sales are as follows: Month EO00 |July 100 August 90 September 125 October 140 2. It is management policy to hold inventory at the end of each month which is sufficient to meet sales demand in the next half month. Sales are budgeted to occur evenly during each month. 3. Creditors are paid one month after the purchase has been made. Calculate the entries for "purchases" that will be shown in the cash budget for August (ii) September October (3 marks)1.13 Division L has reported a net profit after tax of $8-6m for the year ended 30 April 2006. Included in the costs used to calculate this profit are the following items: interest payable of $2-3m; development costs of $6-3m for a new product that was launched in May 2005, and is expected to have a life of three years; advertising expenses of f1-6m that relate to the re-launch of a product in June 2006. The net assets invested in Division L are $30m. The cost of capital for Division L is 13% per year. Calculate the Economic Value Added" for Division L for the year ended 30 April 2006. (3 marks) 1.14 The following details have been taken from the debtor collection records of W plc: Invoices paid in the month after sale 60% Invoices paid in the second month after sale 20% Invoices paid in the third month after sale 15% Bad debts 5% Customers paying in the month after the sale are allowed a 10% discount. Invoices for sales are issued on the last day of the month in which the sales are made. The budgeted credit sales for the final five months of this year are: Month August September |October November December Credit sales $80,000 $100,000 $120,000 $130,000 $160,000 Calculate the total amount budgeted to be received in December from credit sales. (2 marks) 1.15 State four aims of a transfer pricing system