Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help? 26 FKP Sdn Bhd is considering expanding its range of industrial machinery products by manufacturing machine tables and machine bases. Each product requires

Please help?

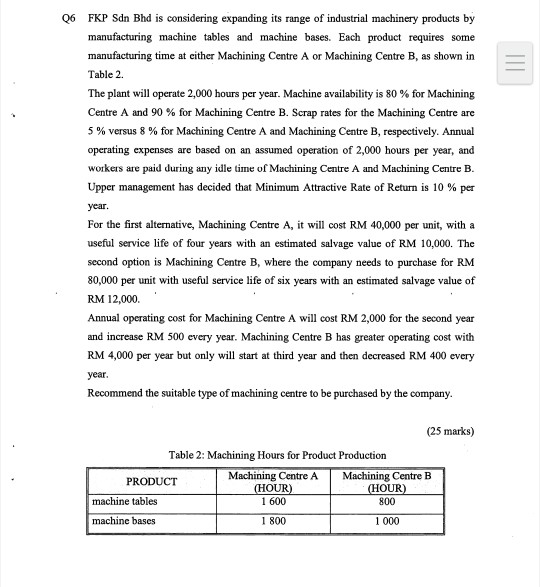

26 FKP Sdn Bhd is considering expanding its range of industrial machinery products by manufacturing machine tables and machine bases. Each product requires some manufacturing time at either Machining Centre A or Machining Centre B, as shown in Table 2. The plant will operate 2,000 hours per year. Machine availability is 80 % for Machining Centre A and 90 % for Machining Centre B. Scrap rates for the Machining Centre are 5 % versus 8 % for Machining Centre A and Machining Centre B, respectively. Annual operating expenses are based on an assumed operation of 2,000 hours per year, and workers are paid during any idle time of Machining Centre A and Machining Centre B. Upper management has decided that Minimum Attractive Rate of Return is 10 % per year. For the first alternative, Machining Centre A, it will cost RM 40,000 per unit, with a useful service life of four years with an estimated salvage value of RM 10,000. The second option is Machining Centre B, where the company needs to purchase for RM 80,000 per unit with useful service life of six years with an estimated salvage value of RM 12,000. Annual operating cost for Machining Centre A will cost RM 2,000 for the second year and increase RM 500 every year. Machining Centre B has greater operating cost with RM 4,000 per year but only will start at third year and then decreased RM 400 every year. Recommend the suitable type of machining centre to be purchased by the company. (25 marks) Table 2: Machining Hours for Product Production Machining Centre A PRODUCT Machining Centre B (HOUR) (HOUR) machine tables 1 600 800 machine bases 1 800 1 000 26 FKP Sdn Bhd is considering expanding its range of industrial machinery products by manufacturing machine tables and machine bases. Each product requires some manufacturing time at either Machining Centre A or Machining Centre B, as shown in Table 2. The plant will operate 2,000 hours per year. Machine availability is 80 % for Machining Centre A and 90 % for Machining Centre B. Scrap rates for the Machining Centre are 5 % versus 8 % for Machining Centre A and Machining Centre B, respectively. Annual operating expenses are based on an assumed operation of 2,000 hours per year, and workers are paid during any idle time of Machining Centre A and Machining Centre B. Upper management has decided that Minimum Attractive Rate of Return is 10 % per year. For the first alternative, Machining Centre A, it will cost RM 40,000 per unit, with a useful service life of four years with an estimated salvage value of RM 10,000. The second option is Machining Centre B, where the company needs to purchase for RM 80,000 per unit with useful service life of six years with an estimated salvage value of RM 12,000. Annual operating cost for Machining Centre A will cost RM 2,000 for the second year and increase RM 500 every year. Machining Centre B has greater operating cost with RM 4,000 per year but only will start at third year and then decreased RM 400 every year. Recommend the suitable type of machining centre to be purchased by the company. (25 marks) Table 2: Machining Hours for Product Production Machining Centre A PRODUCT Machining Centre B (HOUR) (HOUR) machine tables 1 600 800 machine bases 1 800 1 000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Information And Cyber Security Governance

Authors: Robert E Davis

1st Edition

1000416089, 9781000416084