Answered step by step

Verified Expert Solution

Question

1 Approved Answer

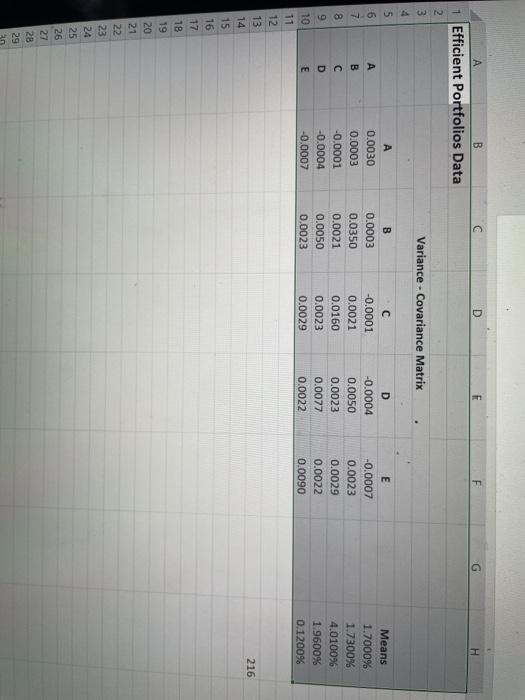

PLEASE HELP 3. You are given the following information: Use the Variance - Covariance matrix in the Excel file: Efficient Portfolios Data Construct a model

PLEASE HELP

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance That Works For You How To Build Wealth Design Your Future And Make Money While You Sleep

Authors: Matthew Kent

1st Edition

1983092851, 9781983092855