please help! also provide explanations to calculations!

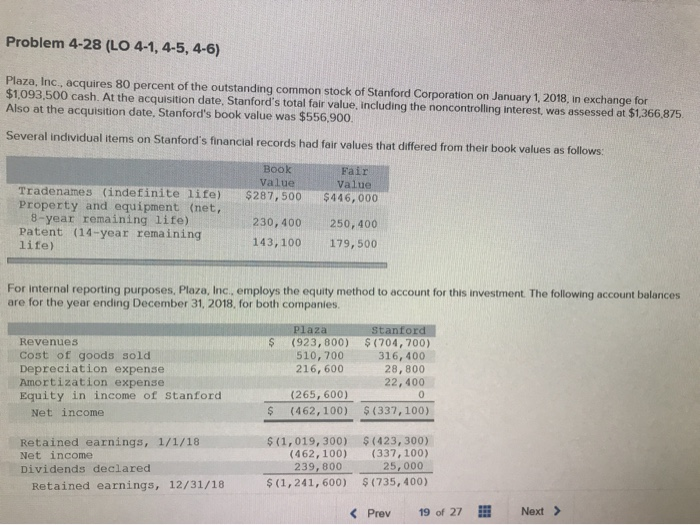

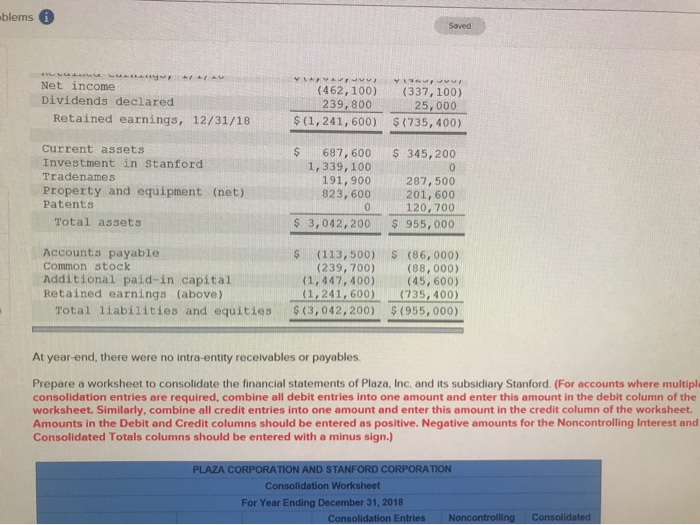

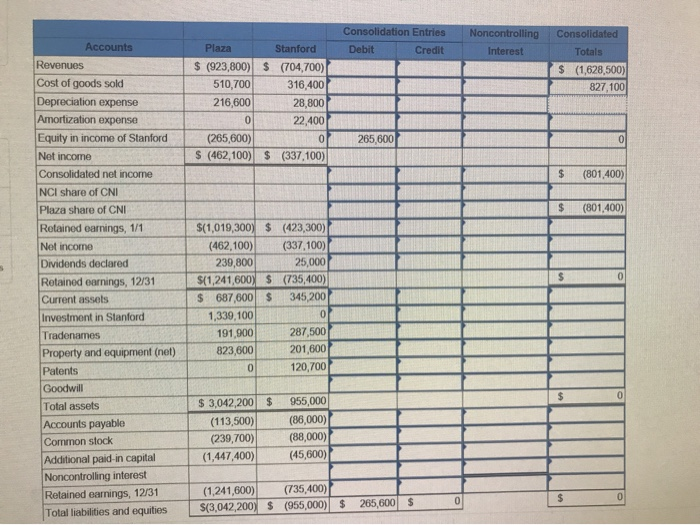

Problem 4-28 (LO 4-1, 4-5, 4-6) Plaza, Inc., acquires 80 percent of the outstanding common stock of Stanford Corporation on January 1, 2018. in exchange for $1,093,500 cash. At the acquisition date, Stanford's total fair value, including the noncontrolling Interest, was assessed at $1,366,875. Also at the acquisition date, Stanford's book value was $556,900. Several individual items on Stanford's financial records had fair values that differed from their book values as follows: Book Value $287,500 Fair Value $446,000 Tradenames (indefinite life) Property and equipment (net, 8-year remaining life) Patent (14-year remaining life) 230,400 143,100 250,400 179,500 For internal reporting purposes, Plaza, Inc, employs the equity method to account for this investment. The following account balances are for the year ending December 31, 2018, for both companies $ Plaza (923, 800) 510,700 216, 600 Stanford S (704, 700) 316, 400 28,800 22,400 Revenues Cost of goods sold Depreciation expense Amortization expense Equity in income of Stanford Net income 0 (265, 600) (462, 100) $ S (337, 100) Retained earnings, 1/1/18 Net income Dividends declared Retained earnings, 12/31/18 $(1,019,300) (462,100) 239,800 $(1,241, 600) S (423, 300) (337, 100) 25,000 $(735, 400) oblems * Saved Net income Dividends declared Retained earnings, 12/31/18 A ) Y (462, 100) 239,800 $(1,241, 600) (337, 100) 25,000 $(735,400) $ 345,200 Current assets Investment in Stanford Tradenames Property and equipment (net) Patents Total assets 687, 600 1, 339, 100 191,900 823, 600 0 $ 3,042,200 287,500 201, 600 120, 700 $ 955,000 Accounts payable Common stock Additional paid-in capital Retained earnings (above) Total liabilities and equities $ (113,500) (239, 700) (1,447, 400) (1,241, 600) $ (3,042,200) $ (86,000) (88,000) (45,600) (735, 400) $(955,000) At year-end, there were no intra-entity receivables or payables Prepare a worksheet to consolidate the financial statements of Plaza, Inc. and its subsidiary Stanford. (For accounts where multiple consolidation entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet. Amounts in the Debit and Credit columns should be entered as positive. Negative amounts for the Noncontrolling Interest and Consolidated Totals columns should be entered with a minus sign.) PLAZA CORPORATION AND STANFORD CORPORATION Consolidation Worksheet For Year Ending December 31, 2018 Consolidation Entries Noncontrolling Consolidated Consolidation Entries Debit Credit Noncontrolling Interest Plaza $ (923,800) 510,700 216,600 Stanford $ (704,700) 316.400 28,800 22,400 Consolidated Totals $ (1,628,500) 827,100 265,600 (265,600) $ (462,100) $ (337,100) (801,400) (801,400) Accounts Revenues Cost of goods sold Depreciation expense Amortization expense Equity in income of Stanford Net income Consolidated net income NCI share of CNI Plaza share of CNI Retained earnings, 1/1 Net income Dividends declared Retained earnings, 12/31 Current assets Investment in Stanford Tradenames Property and equipment (net) Patents Goodwill Total assets Accounts payable Common stock Additional paid-in capital Noncontrolling interest Retained earnings, 12/31 Total liabilities and equities $(1,019,300) $ (423,300) (462,100) (337,100) 239,800 25,000 $(1,241,600) S (735,400) 687,000 $ 345,200 1,339,100 191,900 287,500 823,600 201,600 120,700 $ 955,000 $ 3,042,200 (113,500) (239,700) (1,447,400) (86,000) (88,000) (45,600)| (1,241,600) S(3,042,200) $ (735,400) (955,000) $ 265,600 $