Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help answer these questions by making the correct adjustments 1. A company makes an error in 2015 that overstated its 2015 net income and

Please help answer these questions by making the correct adjustments

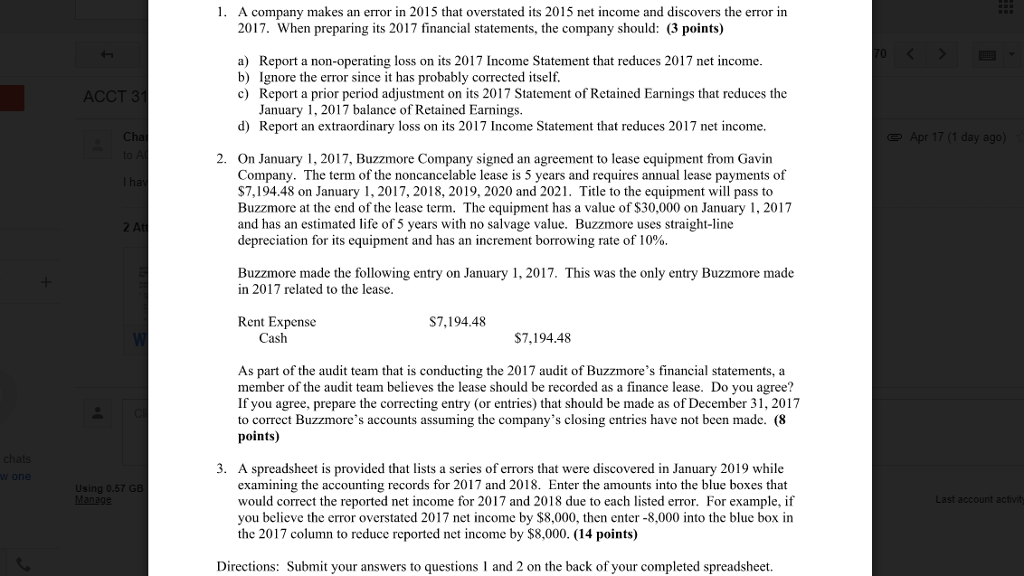

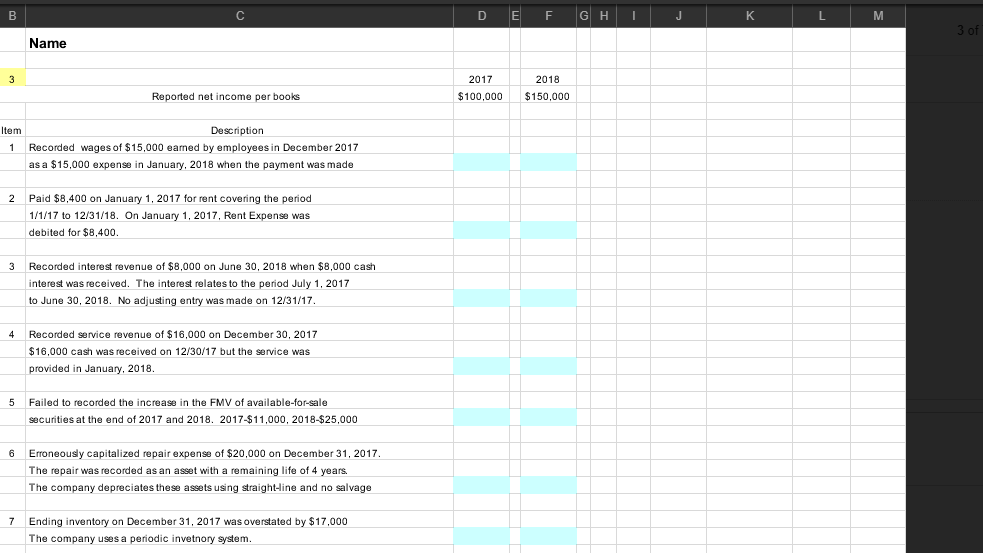

1. A company makes an error in 2015 that overstated its 2015 net income and discovers the error in 2017. When preparing its 2017 financial statements, the company should: (3 points) a) Report a non-operating loss on its 2017 Income Statement that reduces 2017 net income b) Ignore the error since it has probably corrected itself. c) Report a prior period adjustment on its 2017 Statement of Retained Earnings that reduces the January 1, 2017 balance of Retained Earnings. d) Report an extraordinary loss on its 2017 Income Statement that reduces 2017 net income. 2. On January 1, 2017, Buzzmore Company signed an agreement to lease equipment from Gavin The term of the noncancelable lease is 5 years and requires annual lease payments of Company S7,194.48 on January 1, 2017, 2018, 2019, 2020 and 2021. Title to the equipment will pass to Buzzmore at the end of the lease term. The equipment has a value of $30,000 on January 1, 2017 and has an estimated life of 5 years with no salvage value. Buzzmore uses straight-line depreciation for its equipment and has an increment borrowing rate of 10%. Buzzmore made the following entry on January 1, 2017. This was the only entry Buzzmore made in 2017 related to the lease Rent Expense $7,194.48 as S7,194.48 As part of the audit team that is conducting the 2017 audit of Buzzmore's financial statements, a member of the audit team believes the lease should be recorded as a finance lease. Do If you agree, prepare the correcting entry (or entries) that should be made as of December 31,2017 to correct Buzzmore's accounts assuming the company's closing entries have not been made. (8 points) you agree? 3. A spreadsheet is provided that lists a series of errors that were discovered in January 2019 while examining the accounting records for 2017 and 2018. Enter the amounts into the blue boxes that would correct the reported net income for 2017 and 2018 due to each listed error. For example, if you believe the error overstated 2017 net income by $8,000, then enter -8,000 into the blue box in the 2017 column to reduce reported net income by $8,000. (14 points) Directions: Submit your answers to questions 1 and 2 on the back of your completed spreadsheet

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Internal Auditing Continuing Professional Education CPE Edition

Authors: Robert M. Atkisson, Victor Z. Brink, Herbert N. Witt

1st Edition

0471818828, 978-0471818823