Answered step by step

Verified Expert Solution

Question

1 Approved Answer

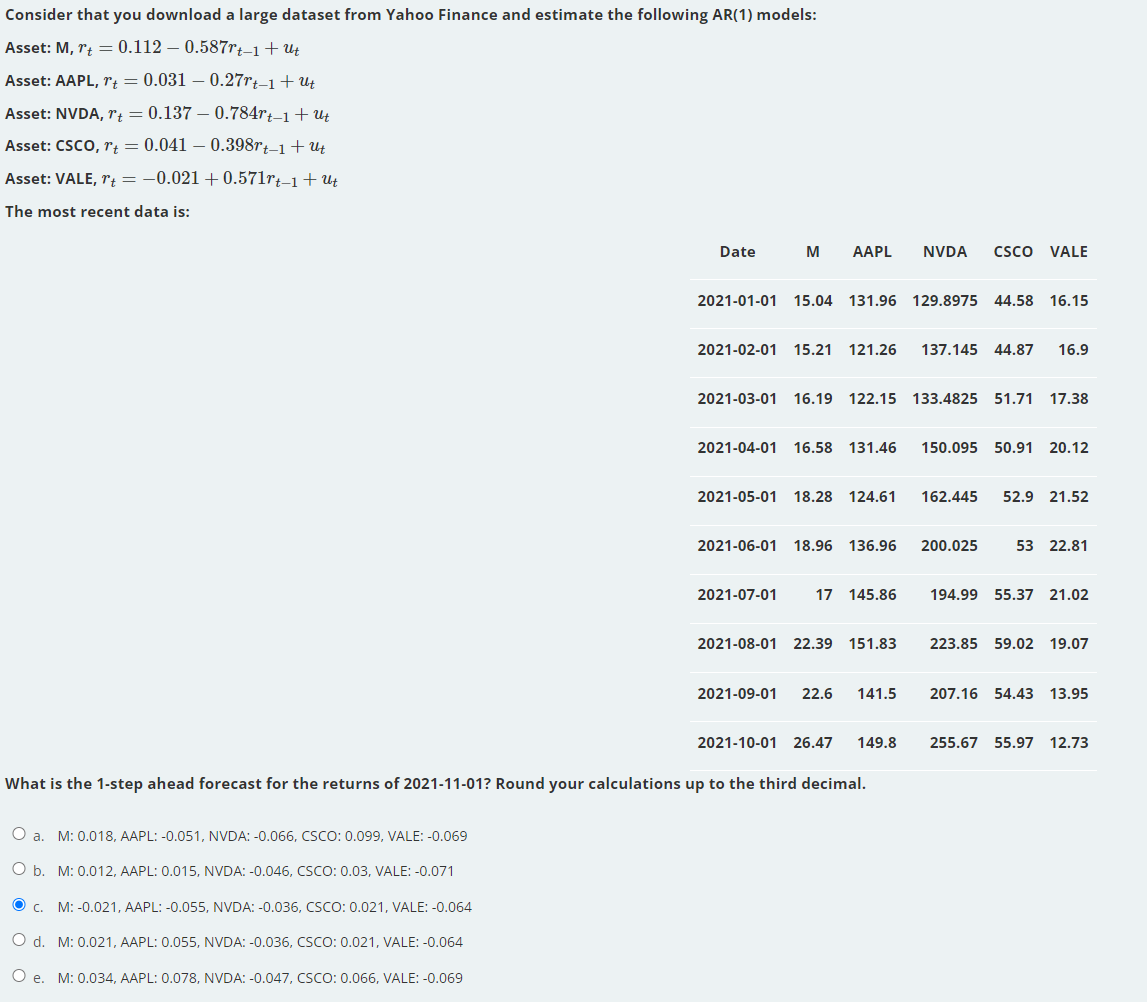

please help i am stuck. Consider that you download a large dataset from Yahoo Finance and estimate the following AR(1) models: Asset: M,rt=0.1120.587rt1+ut Asset: AAPL,

please help i am stuck.

Consider that you download a large dataset from Yahoo Finance and estimate the following AR(1) models: Asset: M,rt=0.1120.587rt1+ut Asset: AAPL, rt=0.0310.27rt1+ut Asset: NVDA, rt=0.1370.784rt1+ut Asset: CSCO, rt=0.0410.398rt1+ut Asset: VALE, rt=0.021+0.571rt1+ut The most recent data is: What is the 1-step ahead forecast for the returns of 2021-11-01? Round your calculations up to the third decin a. M: 0.018 , AAPL: -0.051, NVDA: -0.066, CSCO: 0.099 , VALE: -0.069 b. M: 0.012 , AAPL: 0.015 , NVDA: -0.046, CSCO: 0.03 , VALE: -0.071 c. M: -0.021 , AAPL: -0.055 , NVDA: -0.036, CSCO: 0.021 , VALE: -0.064 d. M: 0.021 , AAPL: 0.055 , NVDA: -0.036, CSCO: 0.021 , VALE: -0.064 e. M: 0.034 , AAPL: 0.078 , NVDA: -0.047 , CSCO: 0.066 , VALE: -0.069Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started