Please help me address the following Question: Based on the 2014 statement of profit and loss data (Exhibits 1 and 2), do you agree with

Please help me address the following Question:

Based on the 2014 statement of profit and loss data (Exhibits 1 and 2), do you agree with Hayes' decision to keep product 103?

a) Should Mayflower lower as of January 1, 2006, its price of product 101? To what price?

b) Why did Mayflower improve profitability during the period January 1 to June 30, 2015? How useful was the data in Exhibit 4 for this analysis?

c) Why is it essential that Mayflower has an effective cost system? What is your overall appraisal of the company's cost system and its use in management reports? List the strengths and weaknesses of this system and its related reports for the purposes management uses the system's output. What recommendations, if any, would you make to Hayes regarding its cost accounting system and related reports?

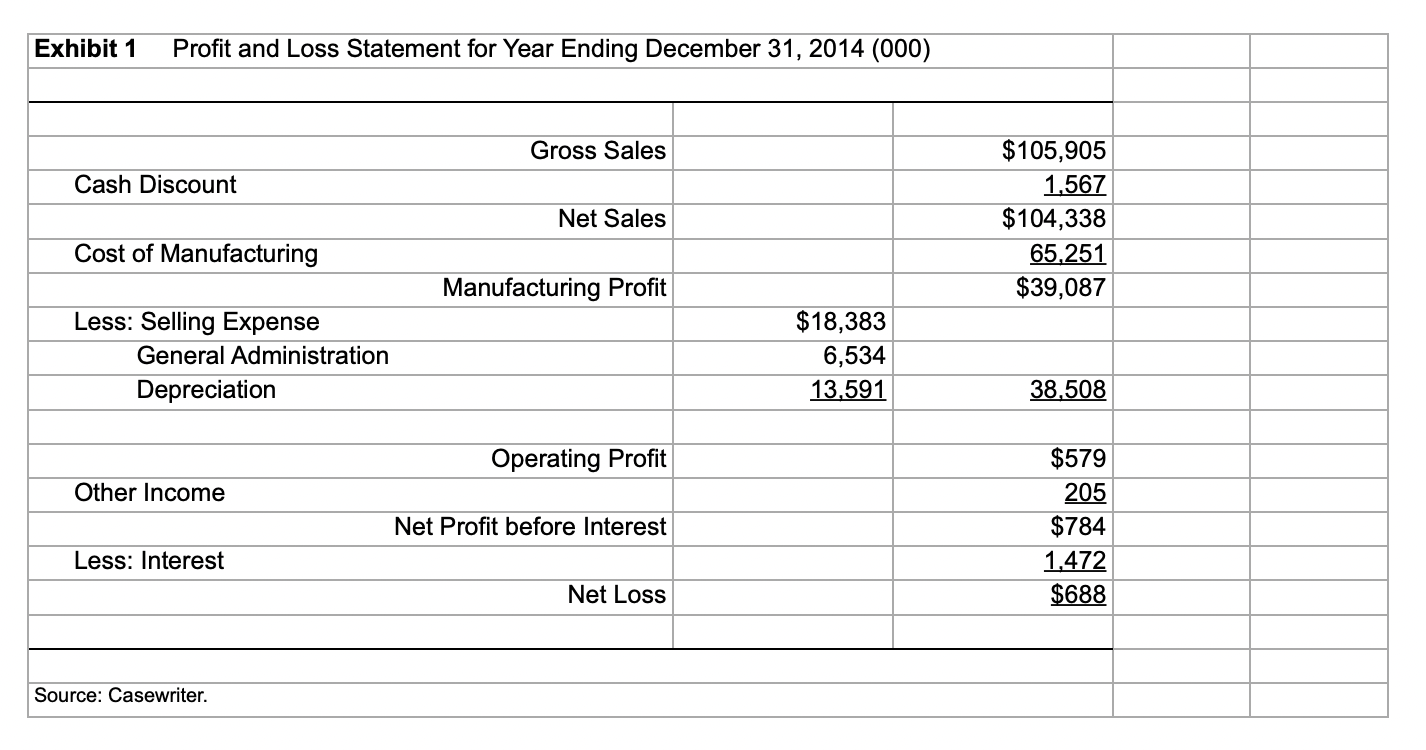

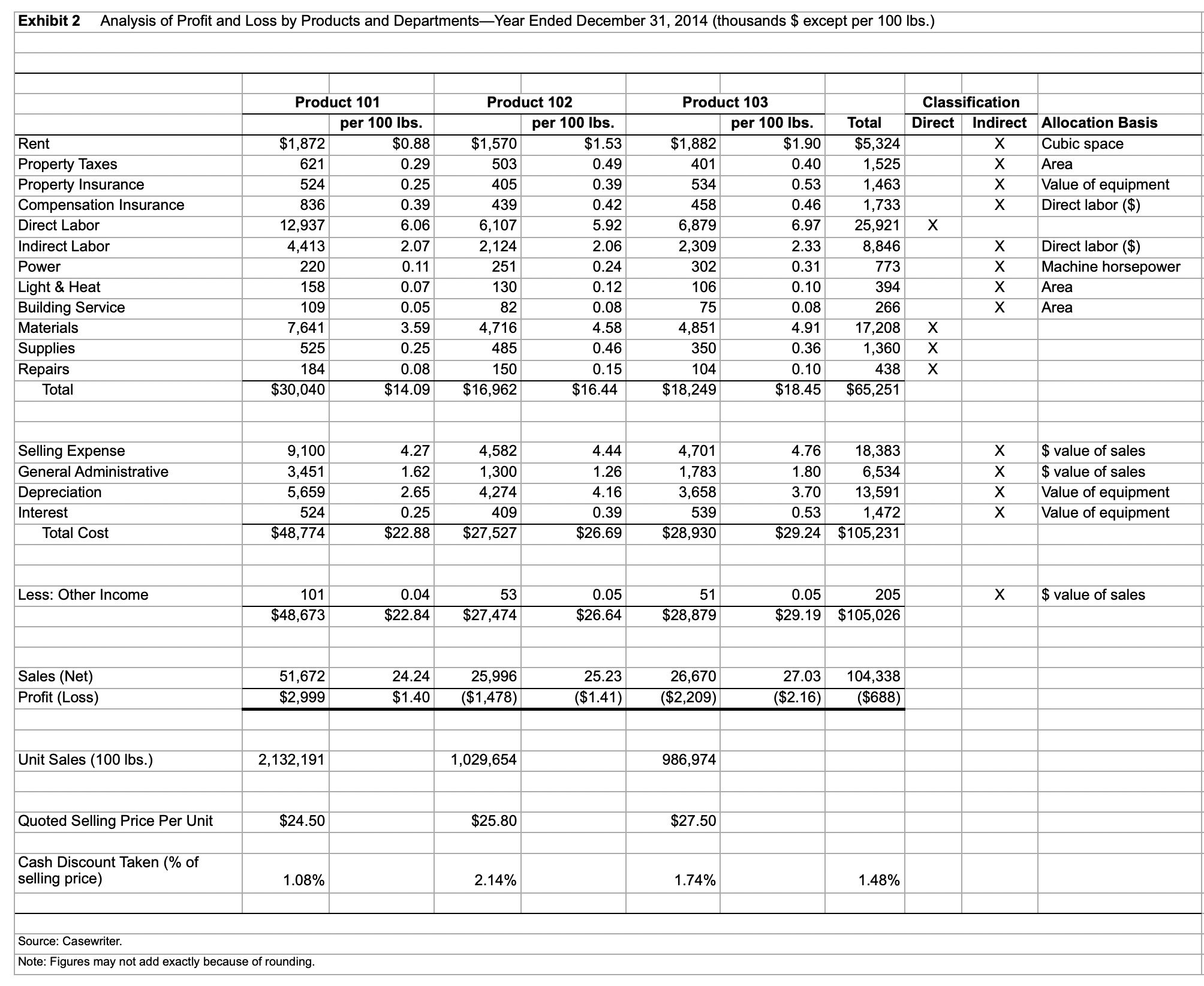

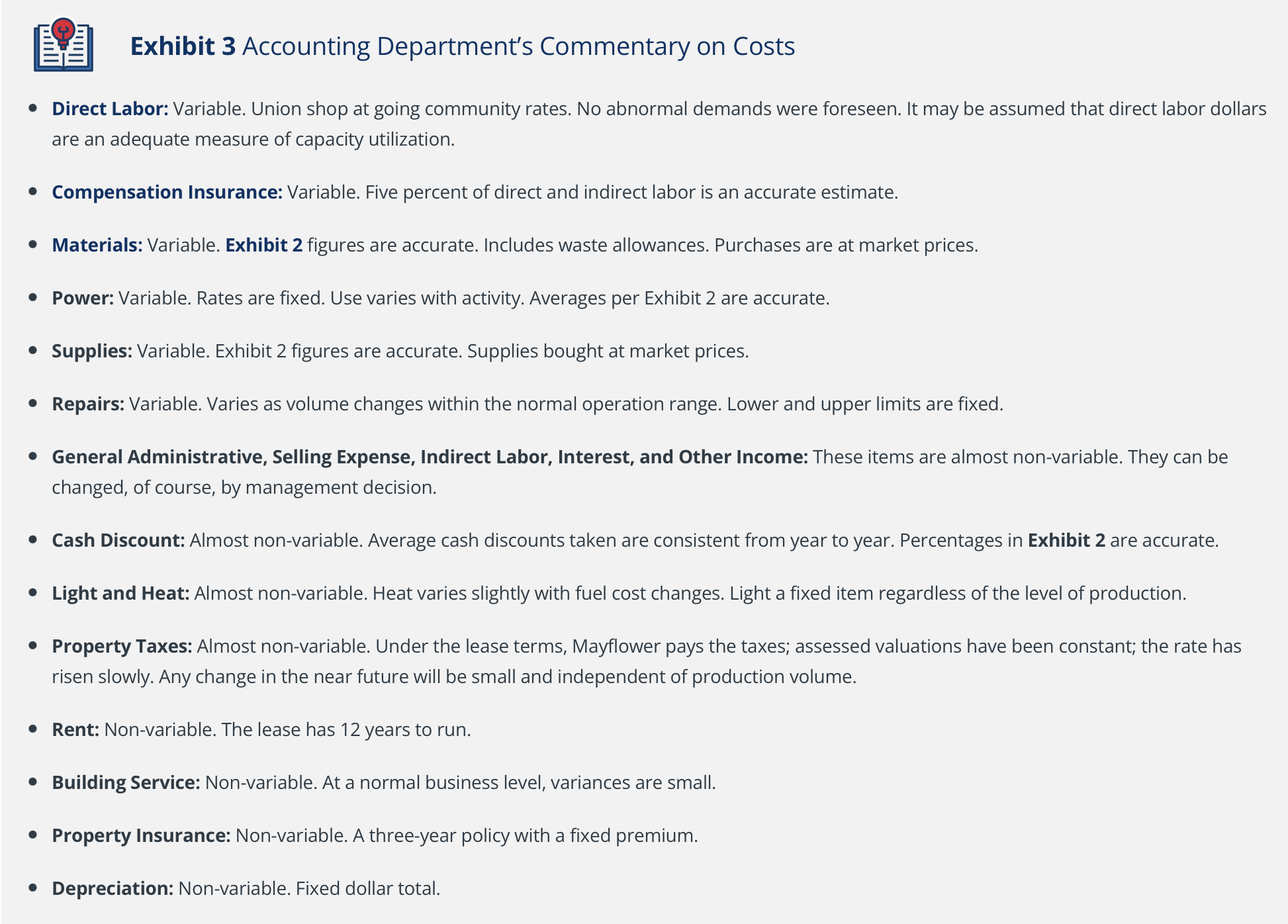

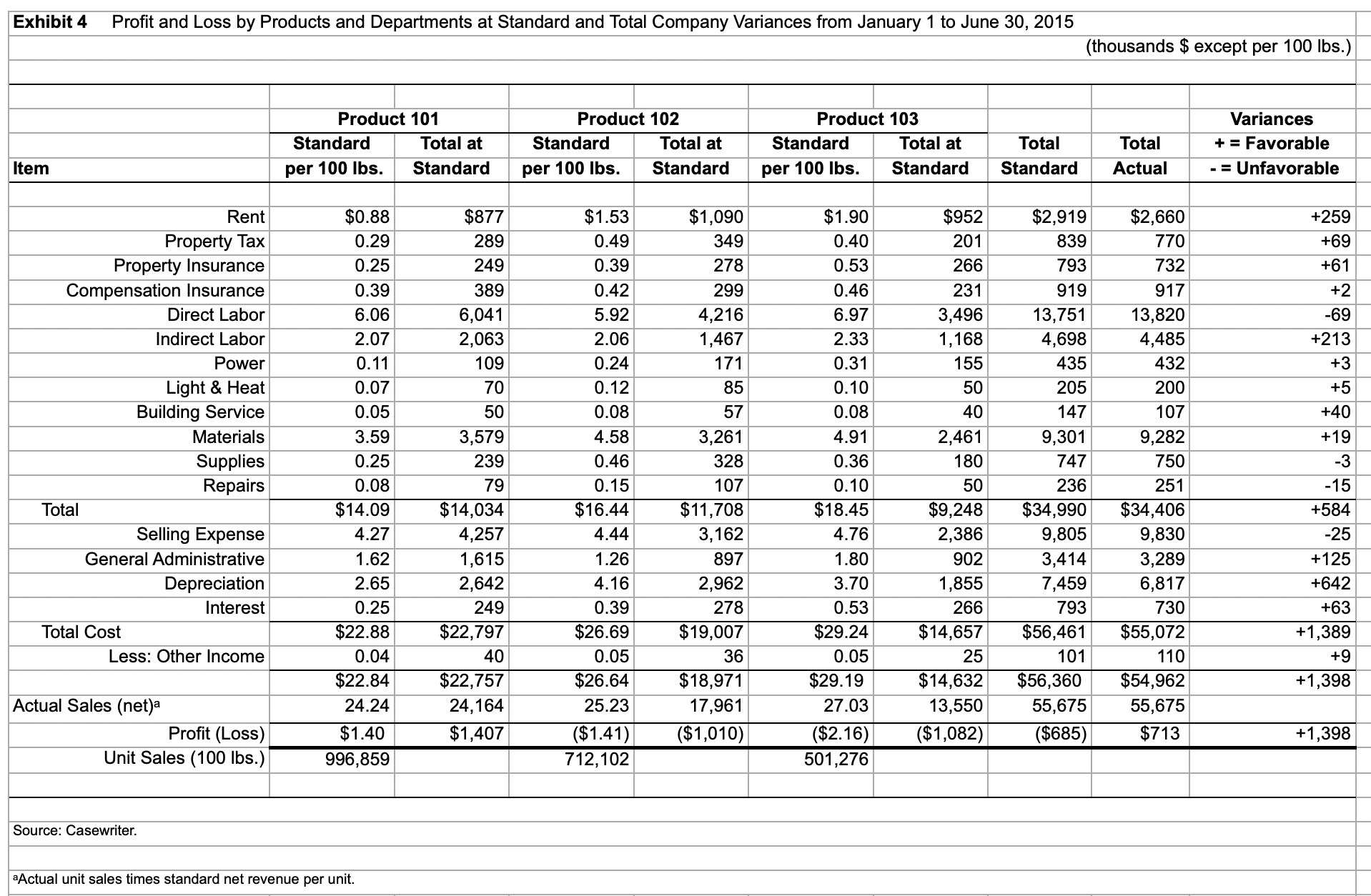

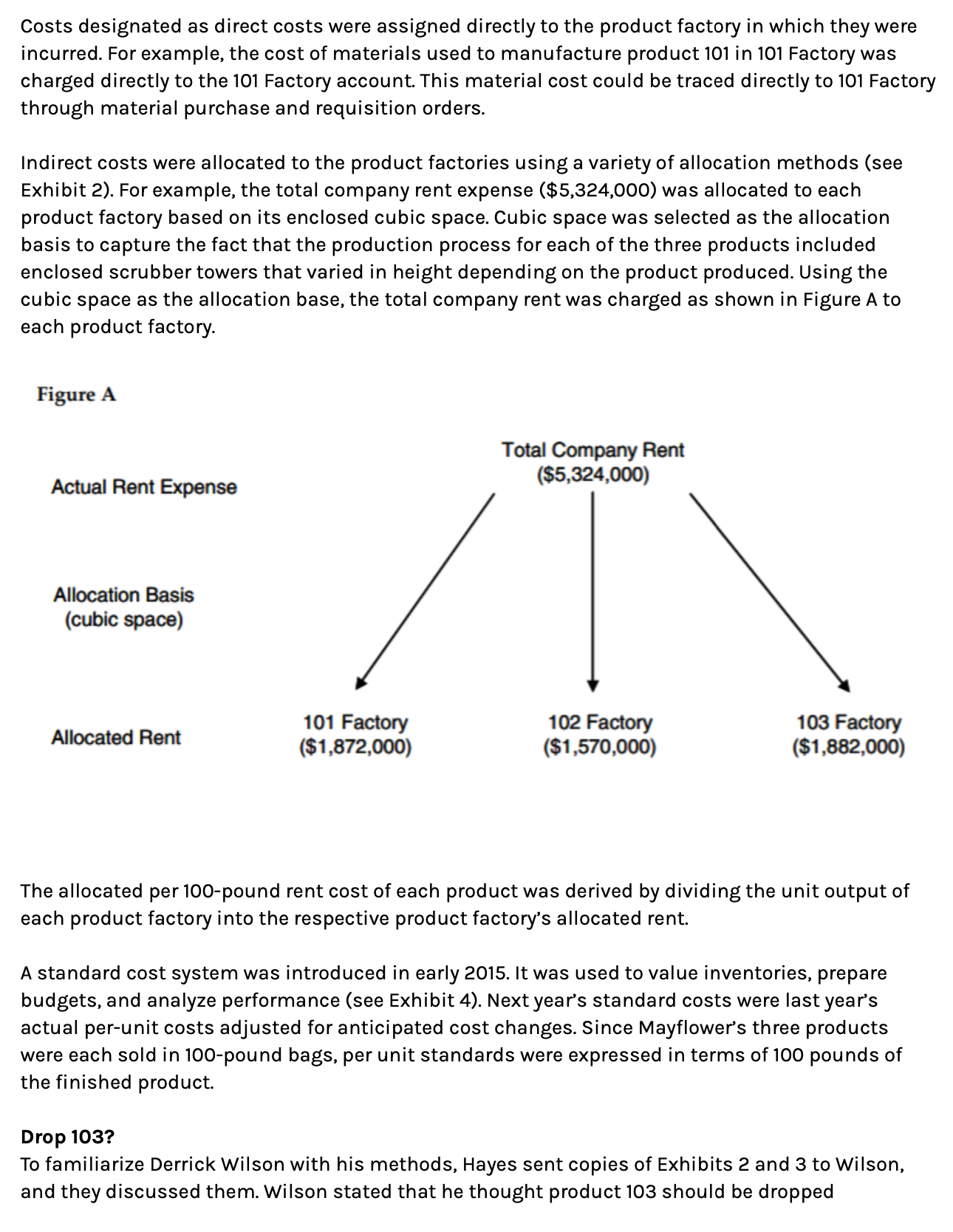

Exhibit 1 Profit and Loss Statement for Year Ending December 31, 2014 (000) Gross Sales $105,905 Cash Discount Net Sales $104,338 Cost of Manufacturing 65 251 Manufacturing Prot $39,087 Less: Selling Expense $18,383 General Administration 6,534 Depreciation 13 591 38 508 Operating Prot $579 Other Income Net Profit before Interest $784 Less: Interest L Net Loss M Source: Case-writer. Exhibit 2 Analysis of Prot and Loss by Products and DepartmentsYear Ended December 31, 2014 (thousands $ except per 100 lbs.) Product 101 Product 102 Product 103 Classification per 100 lbs. per 100 lbs. per 100 lbs. Total Direct Indirect Allocation Basis Rent $1.872 $0.88 $1,570 $1.53 $1,882 $1.90 $5,324 X Cubic space Property Taxes 621 0.29 503 0.49 401 0.40 1,525 X Area Property Insurance 524 0.25 405 0.39 534 0.53 1,463 X Value of equipment Compensation Insurance 836 0.39 439 0.42 458 0.46 1,733 X Direct labor ($) Direct Labor 12,937 6.06 6,107 5.92 6,879 6.97 25,921 X Indirect Labor 4,413 2.07 2,124 2.06 2,309 2.33 8,846 X Direct labor ($) Power 220 0.11 251 0.24 302 0.31 773 X Machine horsepower Light & Heat 158 0.07 130 0.12 106 0.10 394 X Area Building Service 109 0.05 82 0.08 75 0.08 266 X Area Materials 7,641 3.59 4,716 4.58 4,851 4.91 17,208 X Supplies 525 0.25 485 0.46 350 0.36 1,360 X Repairs 184 0.08 150 0.15 104 0.10 438 X Total $30,040 $14.09 $16,962 $16.44 $18,249 $18.45 $65,251 Selling Expense 9,100 4.27 4,582 4.44 4,701 4.76 18,383 X $ value of sales General Administrative 3,451 1.62 1,300 1.26 1,783 1.80 6,534 X 35 value of sales Depreciation 5,659 2.65 4,274 4.16 3,658 3.70 13,591 X Value of equipment Interest 524 0.25 409 0.39 539 0.53 1,472 X Value of equipment Total Cost $48,774 $22.88 $27,527 $26.69 $28,930 $29.24 $105,231 Less: Other Income 101 0.04 53 0.05 51 0.05 205 X $ value of sales $48,673 $22.84 $27,474 $26.64 $28,879 $29.19 $105,026 Sales (Net) 51,672 24.24 25,996 25.23 26,670 27.03 104,338 Profit (Loss) $2,999 $1.40 ($1,478) ($1.41) ($2,209) ($2.16) ($688) Unit Sales (100 lbs.) 2,132,191 1,029,654 986,974 Quoted Selling Price Per Unit $24.50 $25.80 $27.50 Cash Discount Taken (% of selling price) 1.08% 2.14% 1.74% 1.48% Source: Casewriter. Note: Figures may not add exactly because of rounding. Exhibit 3 Accounting Department's Commentary on Costs 0 Direct Labor: Variable. Union shop at going community rates. No abnormal demands were foreseen. It may be assumed that direct labor dollars are an adequate measure of capacity utilization. 0 Compensation Insurance: Variable. Five percent of direct and indirect labor is an accurate estimate. 0 Materials: Variable. Exhibit 2 figures are accurate. Includes waste allowances. Purchases are at market prices. 0 Power: Variable. Rates are fixed. Use varies with activity. Averages per Exhibit 2 are accurate. 0 Supplies: Variable. Exhibit 2 gures are accurate. Supplies bought at market prices. 0 Repairs: Variable. Varies as volume changes within the normal operation range. Lower and upper limits are fixed. 0 General Administrative, Selling Expense, Indirect Labor, Interest, and Other Income: These items are almost non-variable. They can be changed, of course, by management decision. 0 Cash Discount: Almost non-variable. Average cash discounts taken are consistent from yearto year. Percentages in Exhibit 2 are accurate. 0 Light and Heat: Almost non-variable. Heat varies slightly with fuel cost changes. Light a fixed item regardless ofthe level of production. 0 Property Taxes: Almost non-variable. Under the lease terms, Mayower pays the taxes; assessed valuations have been constant; the rate has risen slowly. Any change in the near future will be small and independent of production volume. 0 Rent: Non-variable. The lease has 12 years to run. 0 Building Service: Non-variable. At a normal business level, variances are small. 0 Property Insurance: Non-variable. Athree-year policy with a xed premium. 0 Depreciation: Non-variable. Fixed dollar total. Exhibit 4 Profit and Loss by Products and Departments at Standard and Total Company Variances from January 1 to June 30, 2015 (thousands $ except per 100 lbs.) Product 101 Product 102 Product 103 Variances Standard Total at Standard Total at Standard Total at Total Total + = Favorable Item per 100 lbs. Standard per 100 lbs. Standard per 100 lbs. Standard Standard Actual - = Unfavorable Rent $0.88 $877 $1.53 $1,090 $1.90 $952 $2,919 $2,660 +259 Property Tax 0.29 289 0.49 349 0.40 201 839 770 +69 Property Insurance 0.25 249 0.39 278 0.53 266 793 732 +61 Compensation Insurance 0.39 389 0.42 299 0.46 231 919 917 +2 Direct Labor 6.06 6,041 5.92 4,216 6.97 3,496 13,751 13,820 -69 Indirect Labor 2.07 2,063 2.06 1,467 2.33 1,168 4,698 4,485 +213 Power 0.11 109 0.24 171 0.31 155 435 432 +3 Light 8: Heat 0.07 70 0.12 85 0.10 50 205 200 +5 Building Service 0.05 50 0.08 57 0.08 40 147 107 +40 Materials 3.59 3,579 4.58 3,261 4.91 2,461 9,301 9,282 +19 Supplies 0.25 239 0.46 328 0.36 180 747 750 -3 Repairs 0.08 79 0.15 107 0.10 50 236 251 -15 Total $14.09 $14,034 $16.44 $11,708 $18.45 $9,248 $34,990 $34,406 +584 Selling Expense 4.27 4,257 4.44 3,162 4.76 2,386 9,805 9,830 -25 General Administrative 1.62 1,615 1.26 897 1.80 902 3,414 3,289 +125 Depreciation 2.65 2,642 4.16 2,962 3.70 1,855 7,459 6,817 +642 Interest 0.25 249 0.39 278 0.53 266 793 730 +63 Total Cost $22.88 $22,797 $26.69 $19,007 $29.24 $14,657 $56,461 $55,072 +1,389 Less: Other Income 0.04 40 0.05 36 0.05 25 101 110 +9 $22.84 $22,757 $26.64 $18,971 $29.19 $14,632 $56,360 $54,962 +1,398 Actual Sales (net)a 24.24 24,164 25.23 17,961 27.03 13,550 55,675 55,675 Profit (Loss) $1.40 $1,407 ($1.41) ($1,010) ($2.16) ($1,082) ($685) $713 +1 ,398 Unit Sales (100 WNW Source: Casewriter. aActual unit sales times standard net revenue per unit. Mayflower Manufacturing Company In February 2015, Eugene Hayes was appointed general manager of the Mayower Manufacturing Company by Derrick Wilson, president. Hayes, 56, had wide executive experience in manufacturing products like those of Mayflower. The appointment of Hayes resulted from management problems arising from the death of EdgarWilson, founder and, until his death in early 2014, president of Mayflower. Derrick Wilson had only four years' experience with the company, and in early 2015 was 34 years old. His father had hoped to train him over a 10-year period, but his untimely death had cut this seasoning period short. The younger Wilson became president when his father died and had exercised full control until he hired Hayes. New Management Derrick Wilson knew that during 2014 he had made several poor decisions and noted that the morale of the organization had suffered, apparently through lack of confidence in him. When he received the income statement for 2014 (see Exhibit 1) showing a net loss of $688,000 during a good business year, he knew he needed help. He attracted Hayes from a competitor by offering a stock option incentive in addition to salary, knowing that Hayes wanted to acquire a financial competence for his retirement.The two men came to a clear understanding that Hayes, as general manager, had full authority to execute any changes he desired. In addition, Hayes would explain the reasons for his decisions to Wilson and thereby train him for successful leadership upon Hayes' retirement. Upon taking office in February 2015, Hayes decided against immediate major changes. Rather, he chose to analyze 2014 operations and to wait to see results for the first half of 2015. He instructed the accounting department to provide detailed expenses and earnings statements byproducts and departments for 2014 (see Exhibit 2). In addition, he requested an explanation of the nature of the company's costs including their expected future behavior (see Exhibit 3). Company and Industry The Mayflower Manufacturing Company made only three industrial products: 101,102, and 103.They were sold by the company's sales force for use in the processes of other manufacturers. All of the sales force, on a salary basis, sold the three products but in varying proportions. Mayflower sold throughout New England and was one of eight companies with similar products. Several of its competitors were larger and manufactured a larger variety of products than did Mayflower. The dominant company was the Samra Company,which operated a branch plant in the company's market area. Customarily, the Samra Company announced prices annually, and the other producers followed suit. Price cutting was rare, and the only variance from quoted selling prices took the form of cash discounts. In the past, attempts at price cutting had followed a consistent pattern: all competitors met the price reduction, and the industry as a whole sold about the same quantity but at lower prices.This continued until the Samra Company,with its strong financial position, again stabilized the situation following a general recognition of the failure of price cutting. Furthermore, because sales were to industrial buyers and because the products of different manufacturers were very similar, Hayes was convinced Mayflower could not individually raise prices without suffering substantial volume declines. During 2014, Mayflower's share of industry sales was 12% for type 101, 8% for 102, and 10% for 103. The industrywide quoted selling prices were $24.50, $25.80, and $27.50 per 100 pounds of product, respectively. Manufacturing Strategy Mayflower's manufacturing strategy was based on the \"dedicated factory\" concept. That is, each of the three products was produced in its own factory within the total factory complex. The three product factories were referred to as 101 Factory, 102 Factory, and 103 Factory. Each of these product factories was horizontally integrated beginning with receiving and extending through raw material storage, productionprocess facilities, finishedproduct inventory, and shipping. In addition, each product factory had a dedicated direct labor force, which for accounting purposes included hourly workers, shift managers, and other manufacturing-related personnel assigned to each product factory. Indirect labor\"floated" between product factories as needed. Typically, the Mayflower manufacturing facilities operated below capacity. Cost System The Mayflower Manufacturing Company maintained a simple cost system. It was used for strategic planning, productline decisions, identifying manufacturing processimprovement opportunities, profitability analysis, performance evaluation, cost control, and inventory valuation purposes. Management's goal was to assign all of the company's costs to each of the three products in a way that would lead to the most useful product costs for the cost system's various managerial purposes. The cost system identified two categories of costs. The first category consisted of costs, such as material costs, that could be tied directly to the manufacture of specific products. All other costs were placed in the second category and referred to as indirect costs (see Exhibit 2). The cost system accumulated direct and indirect costs at the productfactory level before determining the individual product costs on a per-unit basis. Since each ofthe three products was sold in 100pound bags, per unit costs were expressed in terms of 100 pounds of the finished product. The perunit cost was calculated by dividing the unit output into the respective product factory's total cost. Total cost was the sum of the product factory's direct costs plus allocated indirect costs less an allocated otherincome amount. Allocated indirect costs included the company's interest cost related to bank loans. Costs designated as direct costs were assigned directly to the product factory in which they were incurred. For example, the cost of materials used to manufacture product 101 in 101 Factory was charged directly to the 101 Factory account. This material cost could be traced directly to 101 Factory through material purchase and requisition orders. Indirect costs were allocated to the product factories using a variety of allocation methods (see Exhibit 2). For example, the total company rent expense ($5,324,000) was allocated to each product factory based on its enclosed cubic space. Cubic space was selected as the allocation basis to capture the fact that the production process for each of the three products included enclosed scrubber towers that varied in height depending on the product produced. Using the cubic space as the allocation base,the total company rent was charged as shown in Figure A to each prod uct factory. Figure A Total Company Rent Actual Rent Expense (55'324'000) Allocation Basis (cubic space) 101 Factory 102 Factory 103 Factory The allocated per 100-pound rent cost of each product was derived by dividing the unit output of each product factory into the respective product factory's allocated rent. A standard cost system was introduced in early 2015. It was used to value inventories, prepare budgets, and analyze performance (see Exhibit 4). Next year's standard costs were last year's actual per-u nit costs adjusted for anticipated cost changes. Since Mayflower's three products were each sold in 100-pound bags, per unit standards were expressed in terms of 100 pounds of the finished product. Drop103'? To familiarize Derrick Wilson with his methods, Hayes sent copies of Exhibits 2 and 3 to Wilson, and they discussed them.Wi|son stated that he thought product 103 should be dropped immediately, as it would be impossible to lower expenses on product 103 as much as $2.16 per100 pounds. In addition, he stressed the need for economies on product 102. Hayes relied on the authority arrangement Wilson had agreed to earlier and continued production ofthe three products. Midyear Results In the first week ofJuly 2015, Hayes received from the accounting department the six months' statement of cumulative standard costs including variances of total company actual costs from standard (see Exhibit 4). It showed that the first half of 2015 had been a successful period. In order to expedite the availability of interimperiod results, Mayflower did not determine actual product-line revenues, costs, and profits. Rather, product-line data was prepared using standard per unit data and actual unit sales. Reduce 101 Price? During the latter half of 2015, the sales of the entire industry weakened. Even though Mayflower retained its share of the market, its profit for the last six months was expected to be small. In November 2015, the Samra Company announced a price reduction as ofJanuary 1, 2006, on product 101 from $24.50 to $22.50 per100 pounds.This created a pricing problem for all its competitors. Hayes forecast that if Mayflower held to the $24.50 price during the first six months of 2006, the company's unit sales would be 750,000. He felt that if it dropped its price to $22.50, the six months' unit volume would be 1 million. Hayes knew that competing managements anticipated a further decline in activity. He thought a general decline in prices of all products was quite probable. The accounting department reported that the standard costs in use would probably apply during 2006, with two exceptions: materials and supplies would be about 5% below the 2015 standard. Hayes and Wilson discussed the pricing problem. Wilson observed that even with the anticipated decline in material and supply costs, a sales price of $22.50 would be below cost.Wi|son, therefore, wanted the $24.50 price to be continued, since he felt the company could not be profitable while selling a key product below cost. Case Adapted from Harvard University Press

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance