please help me answer q4 using the data in q3.thx

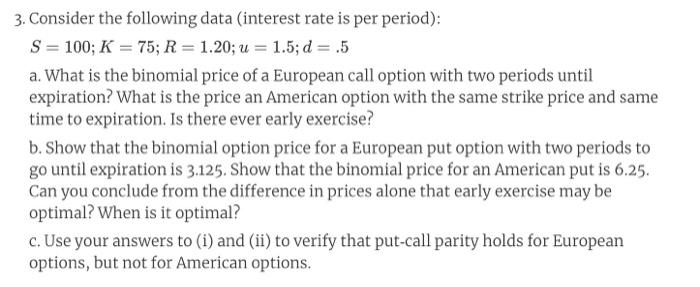

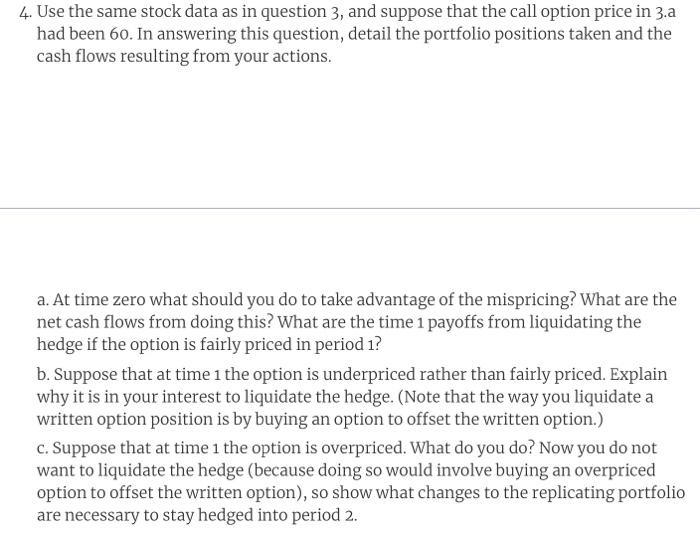

4. Use the same stock data as in question 3, and suppose that the call option price in 3.a had been 60. In answering this question, detail the portfolio positions taken and the cash flows resulting from your actions. a. At time zero what should you do to take advantage of the mispricing? What are the net cash flows from doing this? What are the time 1 payoffs from liquidating the hedge if the option is fairly priced in period 1? b. Suppose that at time 1 the option is underpriced rather than fairly priced. Explain why it is in your interest to liquidate the hedge. (Note that the way you liquidate a written option position is by buying an option to offset the written option.) c. Suppose that at time 1 the option is overpriced. What do you do? Now you do not want to liquidate the hedge (because doing so would involve buying an overpriced option to offset the written option), so show what changes to the replicating portfolio are necessary to stay hedged into period 2. 3. Consider the following data interest rate is per period): S = 100; K = 75; R=1.20; u = 1.5; d = .5 a. What is the binomial price of a European call option with two periods until expiration? What is the price an American option with the same strike price and same time to expiration. Is there ever early exercise? b. Show that the binomial option price for a European put option with two periods to go until expiration is 3.125. Show that the binomial price for an American put is 6.25. Can you conclude from the difference in prices alone that early exercise may be optimal? When is it optimal? c. Use your answers to (i) and (ii) to verify that put-call parity holds for European options, but not for American options. 4. Use the same stock data as in question 3, and suppose that the call option price in 3.a had been 60. In answering this question, detail the portfolio positions taken and the cash flows resulting from your actions. a. At time zero what should you do to take advantage of the mispricing? What are the net cash flows from doing this? What are the time 1 payoffs from liquidating the hedge if the option is fairly priced in period 1? b. Suppose that at time 1 the option is underpriced rather than fairly priced. Explain why it is in your interest to liquidate the hedge. (Note that the way you liquidate a written option position is by buying an option to offset the written option.) c. Suppose that at time 1 the option is overpriced. What do you do? Now you do not want to liquidate the hedge (because doing so would involve buying an overpriced option to offset the written option), so show what changes to the replicating portfolio are necessary to stay hedged into period 2. 3. Consider the following data interest rate is per period): S = 100; K = 75; R=1.20; u = 1.5; d = .5 a. What is the binomial price of a European call option with two periods until expiration? What is the price an American option with the same strike price and same time to expiration. Is there ever early exercise? b. Show that the binomial option price for a European put option with two periods to go until expiration is 3.125. Show that the binomial price for an American put is 6.25. Can you conclude from the difference in prices alone that early exercise may be optimal? When is it optimal? c. Use your answers to (i) and (ii) to verify that put-call parity holds for European options, but not for American options