Answered step by step

Verified Expert Solution

Question

1 Approved Answer

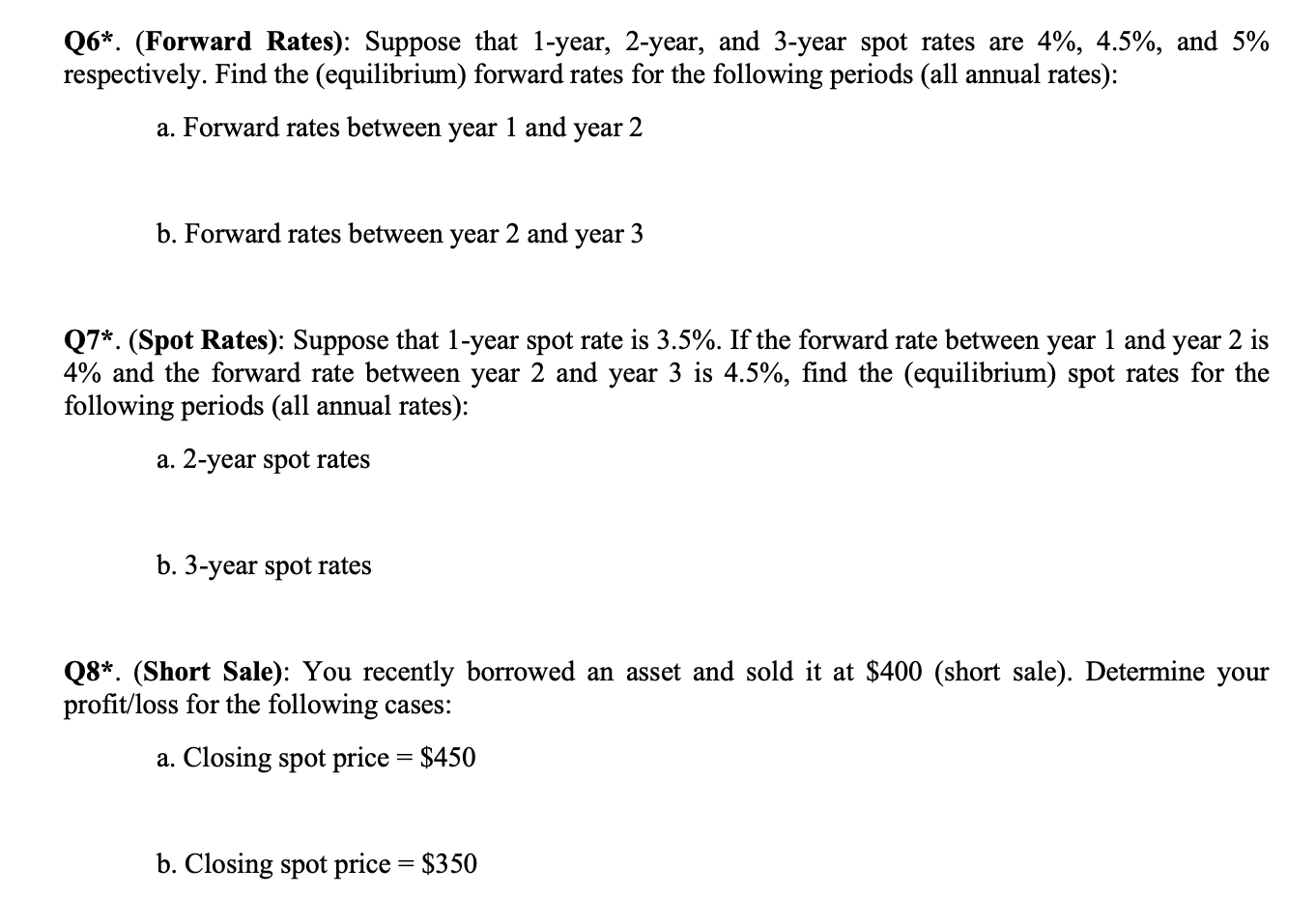

PLEASE HELP ME ANSWER THESE QUESTIONS. THANK YOU VERY MUCH!! Q6*. (Forward Rates): Suppose that 1-year, 2-year, and 3-year spot rates are 4%, 4.5%, and

PLEASE HELP ME ANSWER THESE QUESTIONS. THANK YOU VERY MUCH!!

Q6*. (Forward Rates): Suppose that 1-year, 2-year, and 3-year spot rates are 4%, 4.5%, and 5% respectively. Find the (equilibrium) forward rates for the following periods (all annual rates): a. Forward rates between year 1 and year 2 b. Forward rates between year 2 and year 3 Q7*. (Spot Rates): Suppose that 1-year spot rate is 3.5%. If the forward rate between year 1 and year 2 is 4% and the forward rate between year 2 and year 3 is 4.5%, find the (equilibrium) spot rates for the following periods (all annual rates): a. 2-year spot rates b. 3-year spot rates Q8*. (Short Sale): You recently borrowed an asset and sold it at $400 (short sale). Determine your profit/loss for the following cases: a. Closing spot price = $450 b. Closing spot price = $350Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Treatise On The Law Pertaining To Corporate Finance

Authors: William A. Reid

1st Edition

111793568X, 9781117935683