Please help me fill EMPTY YELLOW CELLS ONLY thanks

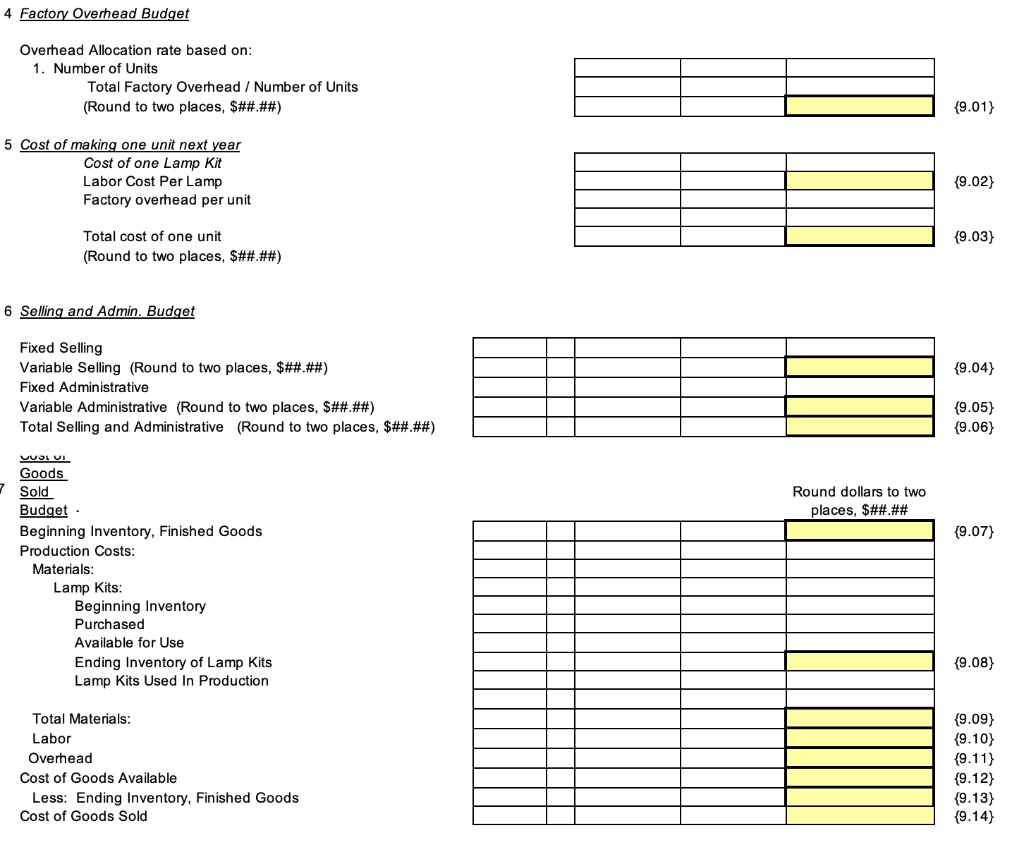

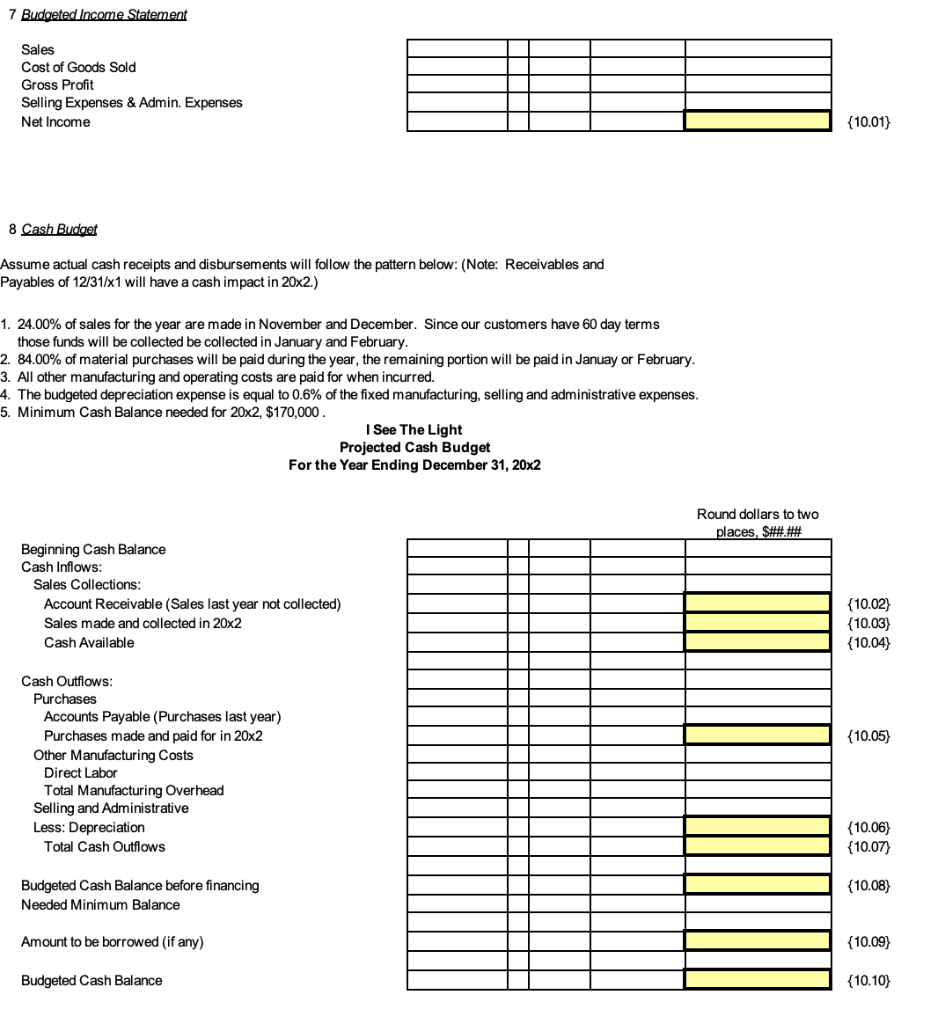

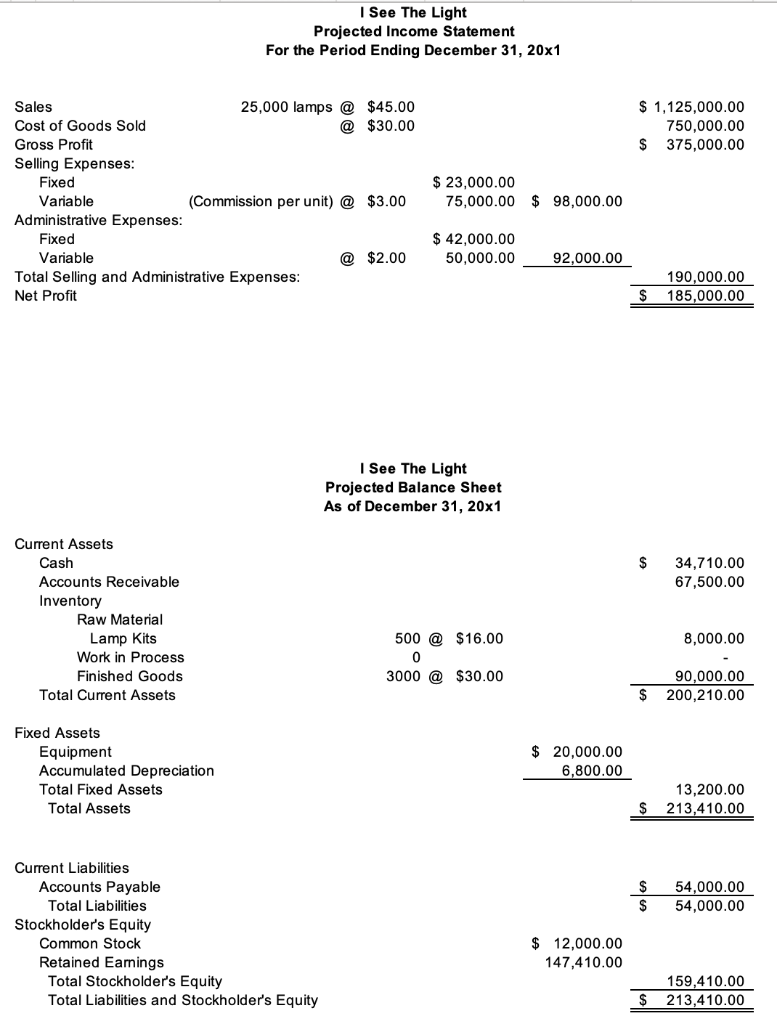

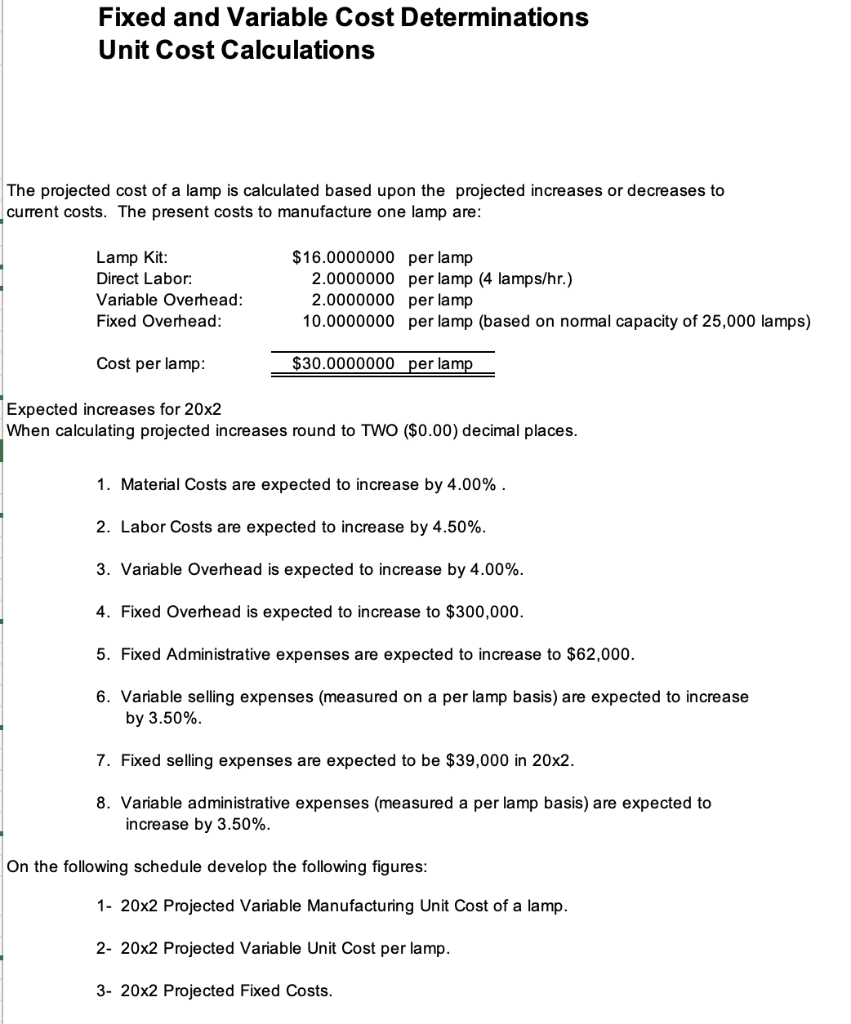

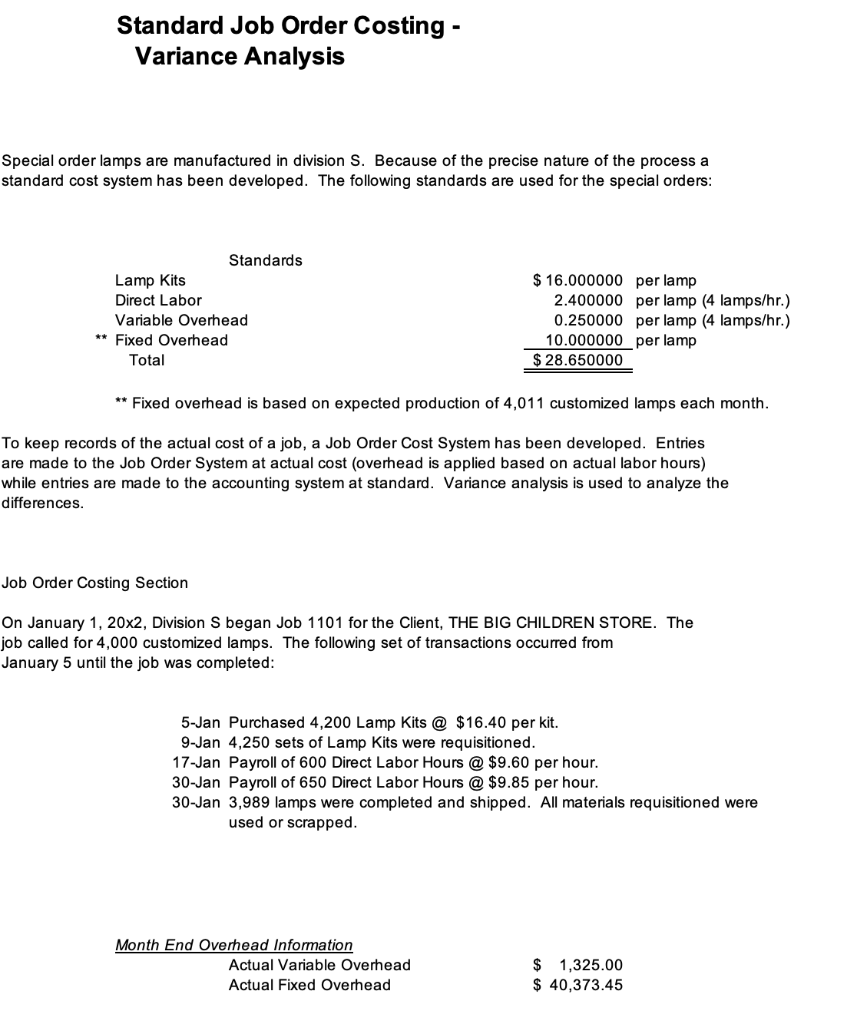

4 Factory Overhead Budget Overhead Allocation rate based on: 1. Number of Units Total Factory Overhead / Number of Units (Round to two places, $##.##) {9.01) 5 Cost of making one unit next year Cost of one Lamp Kit Labor Cost Per Lamp Factory overhead per unit {9.02) {9.03) Total cost of one unit (Round to two places, $##.##) 6 Selling and Admin. Budget {9.04) Fixed Selling Variable Selling (Round to two places, $##.##) Fixed Administrative Variable Administrative (Round to two places, $##.##) Total Selling and Administrative (Round to two places, $##.##) {9.05) {9.06) Round dollars to two places, $##.## {9.07) VOLVI Goods Sold Budget Beginning Inventory, Finished Goods Production Costs: Materials: Lamp Kits: Beginning Inventory Purchased Available for Use Ending Inventory of Lamp Kits Lamp Kits Used In Production {9.08) Total Materials: Labor Overhead Cost of Goods Available Less: Ending Inventory, Finished Goods Cost of Goods Sold {9.09) {9.10) {9.11) {9.12) {9.13) {9.14) 7 Budgeted Income Statement Sales Cost of Goods Sold Gross Profit Selling Expenses & Admin. Expenses Net Income {10.01) 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattern below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 24.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February. 2. 84.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February 3. All other manufacturing and operating costs are paid for when incurred. 4. The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. 5. Minimum Cash Balance needed for 20x2, $170,000. I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Round dollars to two places. S##.## Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) Sales made and collected in 20x2 Cash Available {10.02) {10.03) {10.04} {10.05) Cash Outflows: Purchases Accounts Payable (Purchases last year) Purchases made and paid for in 20x2 Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative Less: Depreciation Total Cash Outflows {10.06) {10.07) {10.08) Budgeted Cash Balance before financing Needed Minimum Balance Amount to be borrowed (if any) {10.09) Budgeted Cash Balance {10.10} I See The Light Projected Income Statement For the Period Ending December 31, 20x1 $ 1,125,000.00 750,000.00 $ 375,000.00 Sales 25,000 lamps @ $45.00 Cost of Goods Sold @ $30.00 Gross Profit Selling Expenses: Fixed Variable (Commission per unit) @ $3.00 Administrative Expenses: Fixed Variable @ $2.00 Total Selling and Administrative Expenses: Net Profit $ 23,000.00 75,000.00 $ 98,000.00 $ 42,000.00 50,000.00 92,000.00 190,000.00 185,000.00 $ I See The Light Projected Balance Sheet As of December 31, 20x1 $ 34,710.00 67,500.00 Current Assets Cash Accounts Receivable Inventory Raw Material Lamp Kits Work in Process Finished Goods Total Current Assets 8,000.00 500 @ $16.00 0 3000 @ $30.00 90,000.00 $ 200,210.00 Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets $ 20,000.00 6,800.00 13,200.00 213,410.00 $ $ $ 54,000.00 54,000.00 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity $ 12,000.00 147,410.00 159,410.00 213,410.00 $ Fixed and Variable Cost Determinations Unit Cost Calculations The projected cost of a lamp is calculated based upon the projected increases or decreases to current costs. The present costs to manufacture one lamp are: Lamp Kit: Direct Labor Variable Overhead: Fixed Overhead: $16.0000000 per lamp 2.0000000 per lamp (4 lamps/hr.) 2.0000000 per lamp 10.0000000 per lamp (based on normal capacity of 25,000 lamps) Cost per lamp: $30.0000000 per lamp Expected increases for 20x2 When calculating projected increases round to TWO ($0.00) decimal places. 1. Material Costs are expected to increase by 4.00% . 2. Labor Costs are expected to increase by 4.50%. 3. Variable Overhead is expected to increase by 4.00%. 4. Fixed Overhead is expected to increase to $300,000. 5. Fixed Administrative expenses are expected to increase to $62,000. 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 3.50%. 7. Fixed selling expenses are expected to be $39,000 in 20x2. 8. Variable administrative expenses (measured a per lamp basis) are expected to increase by 3.50%. On the following schedule develop the following figures: 1- 20x2 Projected Variable Manufacturing Unit Cost of a lamp. 2- 20x2 Projected Variable Unit Cost per lamp. 3- 20x2 Projected Fixed Costs. Standard Job Order Costing - Variance Analysis Special order lamps are manufactured in division S. Because of the precise nature of the process a standard cost system has been developed. The following standards are used for the special orders: Standards Lamp Kits Direct Labor Variable Overhead ** Fixed Overhead Total $ 16.000000 per lamp 2.400000 per lamp (4 lamps/hr.) 0.250000 per lamp (4 lamps/hr.) 10.000000 per lamp $ 28.650000 ** Fixed overhead is based on expected production of 4,011 customized lamps each month. To keep records of the actual cost of a job, a Job Order Cost System has been developed. Entries are made to the Order System at ual cost (overhead is applied sed on actual labor hours) while entries are made to the accounting system at standard. Variance analysis is used to analyze the differences. Job Order Costing Section On January 1, 20x2, Division S began Job 1101 for the Client, THE BIG CHILDREN STORE. The job called for 4,000 customized lamps. The following set of transactions occurred from January 5 until the job was completed: 5-Jan Purchased 4,200 Lamp Kits @ $16.40 per kit. 9-Jan 4,250 sets of Lamp Kits were requisitioned. 17-Jan Payroll of 600 Direct Labor Hours @ $9.60 per hour. 30-Jan Payroll of 650 Direct Labor Hours @ $9.85 per hour. 30-Jan 3,989 lamps were completed and shipped. All materials requisitioned were used or scrapped. Month End Overhead Information Actual Variable Overhead Actual Fixed Overhead $ 1,325.00 $ 40,373.45 4 Factory Overhead Budget Overhead Allocation rate based on: 1. Number of Units Total Factory Overhead / Number of Units (Round to two places, $##.##) {9.01) 5 Cost of making one unit next year Cost of one Lamp Kit Labor Cost Per Lamp Factory overhead per unit {9.02) {9.03) Total cost of one unit (Round to two places, $##.##) 6 Selling and Admin. Budget {9.04) Fixed Selling Variable Selling (Round to two places, $##.##) Fixed Administrative Variable Administrative (Round to two places, $##.##) Total Selling and Administrative (Round to two places, $##.##) {9.05) {9.06) Round dollars to two places, $##.## {9.07) VOLVI Goods Sold Budget Beginning Inventory, Finished Goods Production Costs: Materials: Lamp Kits: Beginning Inventory Purchased Available for Use Ending Inventory of Lamp Kits Lamp Kits Used In Production {9.08) Total Materials: Labor Overhead Cost of Goods Available Less: Ending Inventory, Finished Goods Cost of Goods Sold {9.09) {9.10) {9.11) {9.12) {9.13) {9.14) 7 Budgeted Income Statement Sales Cost of Goods Sold Gross Profit Selling Expenses & Admin. Expenses Net Income {10.01) 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattern below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 24.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February. 2. 84.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February 3. All other manufacturing and operating costs are paid for when incurred. 4. The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. 5. Minimum Cash Balance needed for 20x2, $170,000. I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Round dollars to two places. S##.## Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) Sales made and collected in 20x2 Cash Available {10.02) {10.03) {10.04} {10.05) Cash Outflows: Purchases Accounts Payable (Purchases last year) Purchases made and paid for in 20x2 Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative Less: Depreciation Total Cash Outflows {10.06) {10.07) {10.08) Budgeted Cash Balance before financing Needed Minimum Balance Amount to be borrowed (if any) {10.09) Budgeted Cash Balance {10.10} I See The Light Projected Income Statement For the Period Ending December 31, 20x1 $ 1,125,000.00 750,000.00 $ 375,000.00 Sales 25,000 lamps @ $45.00 Cost of Goods Sold @ $30.00 Gross Profit Selling Expenses: Fixed Variable (Commission per unit) @ $3.00 Administrative Expenses: Fixed Variable @ $2.00 Total Selling and Administrative Expenses: Net Profit $ 23,000.00 75,000.00 $ 98,000.00 $ 42,000.00 50,000.00 92,000.00 190,000.00 185,000.00 $ I See The Light Projected Balance Sheet As of December 31, 20x1 $ 34,710.00 67,500.00 Current Assets Cash Accounts Receivable Inventory Raw Material Lamp Kits Work in Process Finished Goods Total Current Assets 8,000.00 500 @ $16.00 0 3000 @ $30.00 90,000.00 $ 200,210.00 Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets $ 20,000.00 6,800.00 13,200.00 213,410.00 $ $ $ 54,000.00 54,000.00 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity $ 12,000.00 147,410.00 159,410.00 213,410.00 $ Fixed and Variable Cost Determinations Unit Cost Calculations The projected cost of a lamp is calculated based upon the projected increases or decreases to current costs. The present costs to manufacture one lamp are: Lamp Kit: Direct Labor Variable Overhead: Fixed Overhead: $16.0000000 per lamp 2.0000000 per lamp (4 lamps/hr.) 2.0000000 per lamp 10.0000000 per lamp (based on normal capacity of 25,000 lamps) Cost per lamp: $30.0000000 per lamp Expected increases for 20x2 When calculating projected increases round to TWO ($0.00) decimal places. 1. Material Costs are expected to increase by 4.00% . 2. Labor Costs are expected to increase by 4.50%. 3. Variable Overhead is expected to increase by 4.00%. 4. Fixed Overhead is expected to increase to $300,000. 5. Fixed Administrative expenses are expected to increase to $62,000. 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 3.50%. 7. Fixed selling expenses are expected to be $39,000 in 20x2. 8. Variable administrative expenses (measured a per lamp basis) are expected to increase by 3.50%. On the following schedule develop the following figures: 1- 20x2 Projected Variable Manufacturing Unit Cost of a lamp. 2- 20x2 Projected Variable Unit Cost per lamp. 3- 20x2 Projected Fixed Costs. Standard Job Order Costing - Variance Analysis Special order lamps are manufactured in division S. Because of the precise nature of the process a standard cost system has been developed. The following standards are used for the special orders: Standards Lamp Kits Direct Labor Variable Overhead ** Fixed Overhead Total $ 16.000000 per lamp 2.400000 per lamp (4 lamps/hr.) 0.250000 per lamp (4 lamps/hr.) 10.000000 per lamp $ 28.650000 ** Fixed overhead is based on expected production of 4,011 customized lamps each month. To keep records of the actual cost of a job, a Job Order Cost System has been developed. Entries are made to the Order System at ual cost (overhead is applied sed on actual labor hours) while entries are made to the accounting system at standard. Variance analysis is used to analyze the differences. Job Order Costing Section On January 1, 20x2, Division S began Job 1101 for the Client, THE BIG CHILDREN STORE. The job called for 4,000 customized lamps. The following set of transactions occurred from January 5 until the job was completed: 5-Jan Purchased 4,200 Lamp Kits @ $16.40 per kit. 9-Jan 4,250 sets of Lamp Kits were requisitioned. 17-Jan Payroll of 600 Direct Labor Hours @ $9.60 per hour. 30-Jan Payroll of 650 Direct Labor Hours @ $9.85 per hour. 30-Jan 3,989 lamps were completed and shipped. All materials requisitioned were used or scrapped. Month End Overhead Information Actual Variable Overhead Actual Fixed Overhead $ 1,325.00 $ 40,373.45