Please, help me.

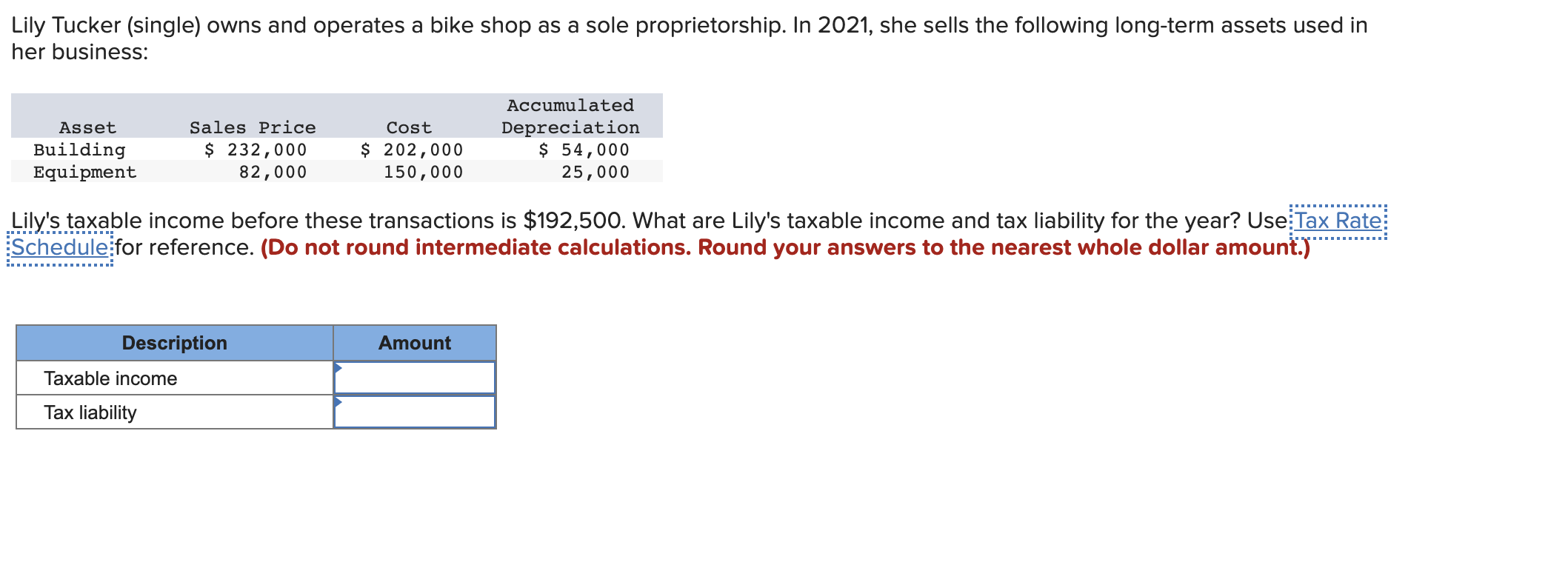

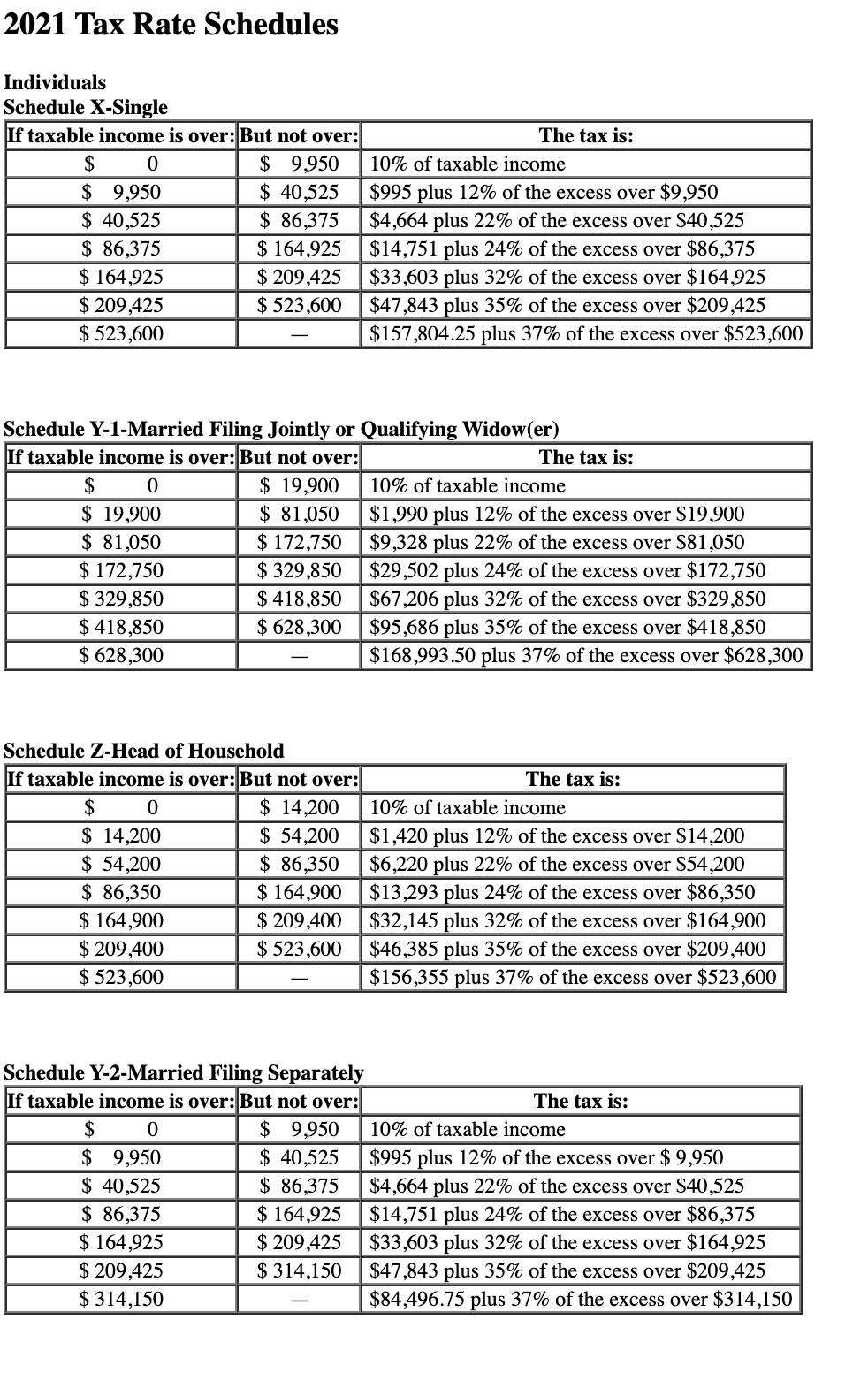

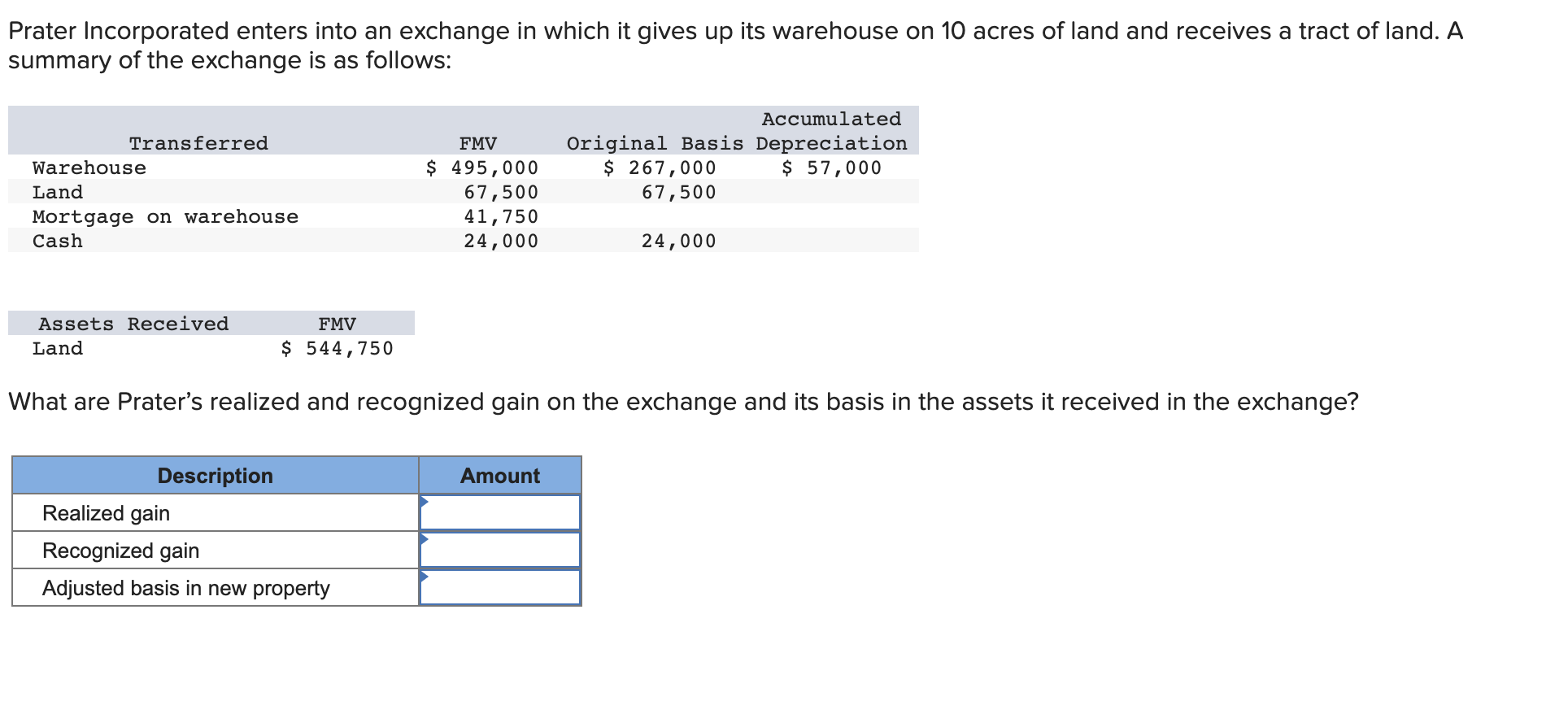

Lily Tucker (single) owns and operates a bike shop as a sole proprietorship. In 2021, she sells the following long-term assets used in her business: Asset Building Equipment Sales Price $ 232,000 82,000 Cost $ 202,000 150,000 Accumulated Depreciation $ 54,000 25,000 Lily's taxable income before these transactions is $192,500. What are Lily's taxable income and tax liability for the year? Use Tax Rate Schedule for reference. (Do not round intermediate calculations. Round your answers to the nearest whole dollar amount.) Description An Taxable income Tax liability 2021 Tax Rate Schedules Individuals Schedule X-Single If taxable income is over: But not over: $ 0 $ 9,950 $ 9,950 $ 40,525 $ 40,525 $ 86,375 $ 86,375 $ 164,925 $ 164,925 $ 209,425 $ 209,425 $ 523,600 $ 523,600 The tax is: 10% of taxable income $995 plus 12% of the excess over $9,950 $4,664 plus 22% of the excess over $40,525 $14,751 plus 24% of the excess over $86,375 $33,603 plus 32% of the excess over $164,925 $47,843 plus 35% of the excess over $209,425 $157,804.25 plus 37% of the excess over $523,600 Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over:But not over: The tax is: $ 0 $ 19,900 10% of taxable income $ 19,900 $ 81,050 $1,990 plus 12% of the excess over $19,900 $ 81,050 $ 172,750 $9,328 plus 22% of the excess over $81,050 $ 172,750 $ 329,850 $29,502 plus 24% of the excess over $172,750 $ 329,850 $ 418,850 $67,206 plus 32% of the excess over $329,850 $ 418,850 $ 628,300 $95,686 plus 35% of the excess over $418,850 $ 628,300 $168,993.50 plus 37% of the excess over $628,300 Schedule Z-Head of Household If taxable income is over: But not over: $ 0 $ 14,200 $ 14,200 $ 54,200 $ 54,200 $ 86,350 $ 86,350 $ 164,900 $ 164,900 $ 209,400 $ 209,400 $ 523,600 $ 523,600 The tax is: 10% of taxable income $1,420 plus 12% of the excess over $14,200 $6,220 plus 22% of the excess over $54,200 $13,293 plus 24% of the excess over $86,350 $32,145 plus 32% of the excess over $164,900 $46,385 plus 35% of the excess over $209,400 $156,355 plus 37% of the excess over $523,600 Schedule Y-2-Married Filing Separately If taxable income is over: But not over: The tax is: $ 0 $ 9,950 10% of taxable income $ 9,950 $ 40,525 $995 plus 12% of the excess over $ 9,950 $ 40,525 $ 86,375 $4,664 plus 22% of the excess over $40,525 $ 86,375 $ 164,925 $14,751 plus 24% of the excess over $86,375 $ 164,925 $ 209,425 $33,603 plus 32% of the excess over $164,925 $ 209,425 $ 314,150 $47,843 plus 35% of the excess over $209,425 $ 314,150 $84,496.75 plus 37% of the excess over $314,150 Prater Incorporated enters into an exchange in which it gives up its warehouse on 10 acres of land and receives a tract of land. A summary of the exchange is as follows: Transferred Warehouse Land Mortgage on warehouse Cash FMV $ 495,000 67,500 41,750 24,000 Accumulated Original Basis Depreciation $ 267,000 $ 57,000 67,500 24,000 Assets Received Land FMV $ 544,750 What are Prater's realized and recognized gain on the exchange and its basis in the assets it received in the exchange? Amount Description Realized gain Recognized gain Adjusted basis in new property