Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help me solve this problem At January 1, 2022, Crane Company reported the following property, plant, and equipment accounts: Accumulated depreciation-buildings Accumulated depreciation-equipment $63,550,000

Please help me solve this problem

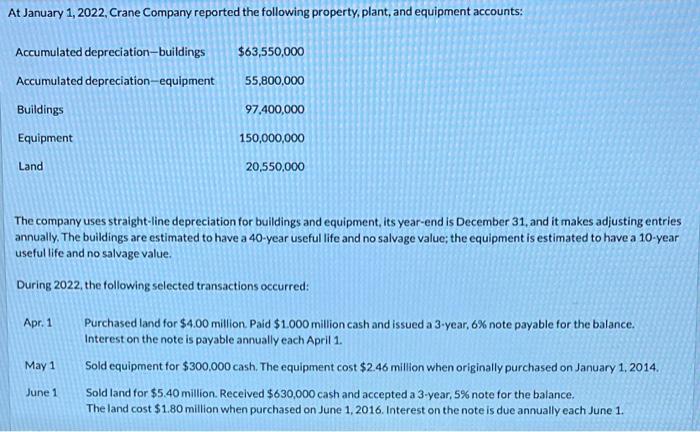

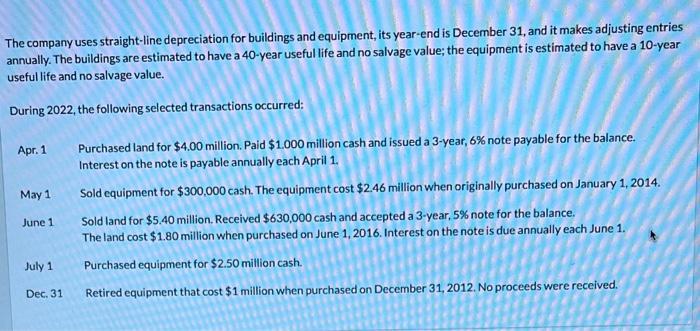

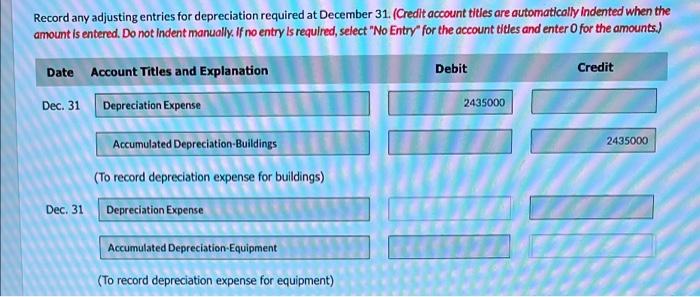

At January 1, 2022, Crane Company reported the following property, plant, and equipment accounts: Accumulated depreciation-buildings Accumulated depreciation-equipment $63,550,000 55,800,000 Buildings 97,400,000 Equipment 150,000,000 Land 20,550,000 The company uses straight-line depreciation for buildings and equipment, its year-end is December 31, and it makes adjusting entries annually. The buildings are estimated to have a 40-year useful life and no salvage value; the equipment is estimated to have a 10-year useful life and no salvage value. During 2022, the following selected transactions occurred: Apr. 1 May 1 Purchased land for $4.00 million Paid $1.000 million cash and issued a 3-year, 6% note payable for the balance. Interest on the note is payable annually each April 1. Sold equipment for $300,000 cash. The equipment cost $2.46 million when originally purchased on January 1, 2014 Sold land for $5.40 million. Received $630,000 cash and accepted a 3-year, 5% note for the balance. The land cost $1.80 million when purchased on June 1, 2016. Interest on the note is due annually each June 1. June 1 The company uses straight-line depreciation for buildings and equipment, its year-end is December 31, and it makes adjusting entries annually. The buildings are estimated to have a 40-year useful life and no salvage value; the equipment is estimated to have a 10-year useful life and no salvage value. During 2022, the following selected transactions occurred: Apr. 1 May 1 June 1 Purchased land for $4.00 million. Paid $1.000 million cash and issued a 3-year, 6% note payable for the balance. Interest on the note is payable annually each April 1. Sold equipment for $300,000 cash. The equipment cost $2.46 million when originally purchased on January 1, 2014. Sold land for $5.40 million. Received $630,000 cash and accepted a 3-year, 5% note for the balance. The land cost $1.80 million when purchased on June 1, 2016. Interest on the note is due annually each June 1. Purchased equipment for $2.50 million cash. Retired equipment that cost $1 million when purchased on December 31, 2012. No proceeds were received. July 1 Dec, 31 Record any adjusting entries for depreciation required at December 31. (Credit account titles are automatically Indented when the amount is entered. Do not Indent manually. If no entry is required, select "No Entry for the account titles and enter for the amounts.) Debit Credit Date Account Titles and Explanation Dec. 31 Depreciation Expense 2435000 2435000 Accumulated Depreciation Buildings (To record depreciation expense for buildings) Dec. 31 Depreciation Expense Accumulated Depreciation Equipment (To record depreciation expense for equipment) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Spiritual Audit Of Corporate America A Hard Look At Spirituality Religion And Values In The Workplace

Authors: Ian Mitroff, Elizabeth A. Denton

1st Edition

978-1118599617