Answered step by step

Verified Expert Solution

Question

1 Approved Answer

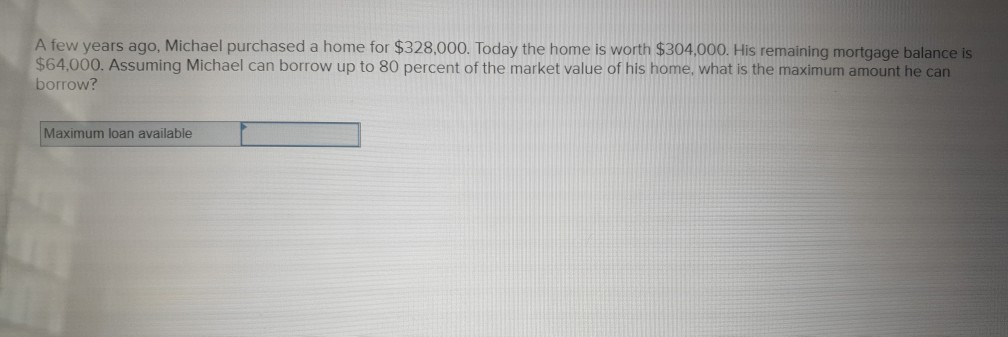

please help me. thank you. A few years ago, Michael purchased a home for $328,000. Today the home is worth $304,000. His remaining mortgage balance

please help me. thank you.

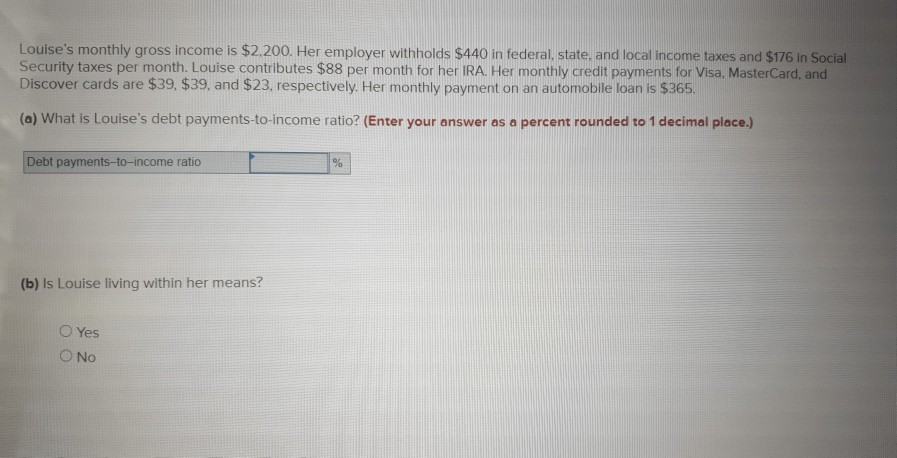

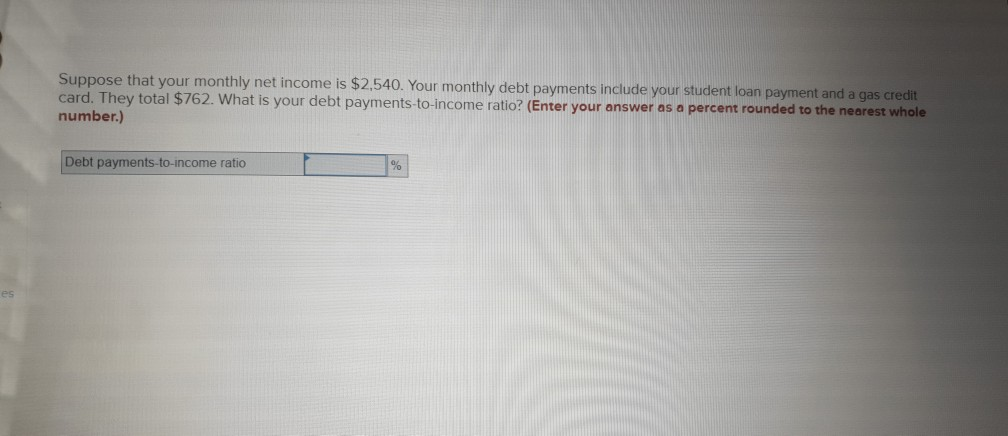

A few years ago, Michael purchased a home for $328,000. Today the home is worth $304,000. His remaining mortgage balance is $64,000. Assuming Michael can borrow up to 80 percent of the market value of his home, what is the maximum amount he can borrow? Maximum loan available Louise's monthly gross income is $2,200. Her employer withholds $440 in federal, state, and local income taxes and $176 in Social Security taxes per month. Louise contributes $88 per month for her IRA. Her monthly credit payments for Visa, MasterCard, and Discover cards are $39, $39. and $23, respectively. Her monthly payment on an automobile loan is $365. (a) What is Louise's debt payments-to-income ratio? (Enter your answer as a percent rounded to 1 decimal place.) Debt payments-to-income ratio % (b) Is Louise living within her means? Yes Suppose that your monthly net income is $2,540. Your monthly debt payments include your student loan payment and a gas credit card. They total $762. What is your debt payments-to-income ratio? (Enter your answer as a percent rounded to the nearest whole number.) Debt payments-to-income ratio %Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Audit Of The Case Study Method

Authors: Michael Masoner

1st Edition

027592761X, 978-0275927615